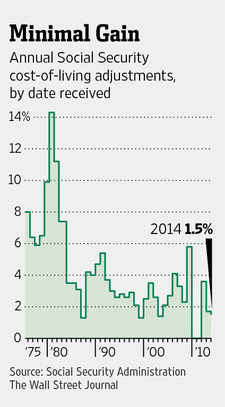

Social Security Benefits To Increase 1.5% in 2014

The federal government announced Wednesday that the social security benefits for almost 63 million retirees and disabled people will increase by 1.5% next year.

The federal government announced Wednesday that the social security benefits for almost 63 million retirees and disabled people will increase by 1.5% next year.

This will be one of the smallest annual increases since automatic cost-of-living adjustments (COLA) began in 1975. The sluggish U.S economic recovery has kept inflation in check and limited businesses’ ability to raise prices of goods and services.

The COLA is calculated by comparing consumer prices in July, August and September each year to prices in the same three months from the previous year. If prices go up over the course of the year, benefits go up, starting with payments delivered in January.

The benefit increase for 2014 comes after a 1.7% gain for 2013. Besides 2010 and 2011, when there were no increases, next year’s rise will be the smallest since 2003, when benefits went up by 1.4%.

Social Security pays retired workers an average of $1,272 a month. A 1.5% raise comes to about $19.