“In general, I think it most likely that in the coming year, (a) the lethality of the virus continues to wane, (b) the world economy continues to reopen, (c) corporate earnings continue to advance, (d) the Federal Reserve begins draining excess liquidity from the banking system with some resultant increase in interest rates, (e) inflation subsides somewhat, and (f) barring some other exogenous variable – which we can never really do – equity values continue to advance, though at something less (and probably a lot less) than the blazing pace at which they’ve been soaring since the market trough of March 2020…Please don’t mistake this for a forecast. [If it’s wrong] my recommendations to you will be unaffected, since our investment policy is driven entirely by the plan we’ve made, and not at all by current events (emphasis added).”

Exogenous means the variable or the event is coming from outside.

Russia/Ukraine is the exogenous variable du jour. The investment policy of goal-focused, plan-driven, long-term stock investors, like you and I, should be unaffected by it.

That concludes this memo’s core message; everything else is commentary.

Under the heading of commentary:

(1) The Russia/Ukraine event has nothing to do with “democracy.” It has to do with energy, which is the lifeblood of the Russian kleptocracy. Russia supplies 40% of Europe’s heating fuel, in the form of natural gas. One of the two aging pipelines through which the gas is transmitted runs through Ukraine, which had lately evinced a growing yearning for increased ties to the West. Putin could never allow this. (See Lukas Alpert’s essay on MarketWatch.)

(2) At around 4,100, the S&P 500 has experienced a drawdown about equal to its average since 1980.

(3) At the risk of making a political statement: A great deal of good can come out of all this, if and to the extent that it leads both the United States and Europe to a significant reappraisal of their respective energy policies, to the detriment of Putin’s Russia.

My thoughts and heart are with the people of Ukraine and our US military personnel deployed in Eastern Europe.

How much inflation can the country afford before we’re in trouble?

Let’s discuss.

First, let’s get on the same page about some basics.

If you’ve noticed the price of a thing increasing over time (say, your favorite candy bar, postage stamps, or the cost of college tuition), that’s inflation in action.

Retirement planners and investment managers like us keep a keen eye on inflation because the whole point of investing our clients’ money is to keep up with or outpace the rising cost of living.

Economists use the broad increase (or decrease) in prices of goods and services across the country as a measure of economic health.

When inflation is stable and predictable, it’s a sign of a basically healthy, growing economy.

But, high inflation can quickly eat away at the purchasing power of your dollars, indicating that the economy might be overheated.

Deflation, or a decline in prices, can be a warning sign of a shrinking economy.

Recent data highlighted a surprise spike in inflation, indicating that prices increased faster than economists expected last month.1

Could this be a worrisome sign that the economy is overheated? Could $50 burgers be in our future?

Maybe.

On the other hand, could it be a temporary blip caused by the economy emerging from the pandemic-driven slowdown, complicated by supply chain issues?

Very possible.

Are the headlines catastrophizing?

They always are.

Let’s look at the data.

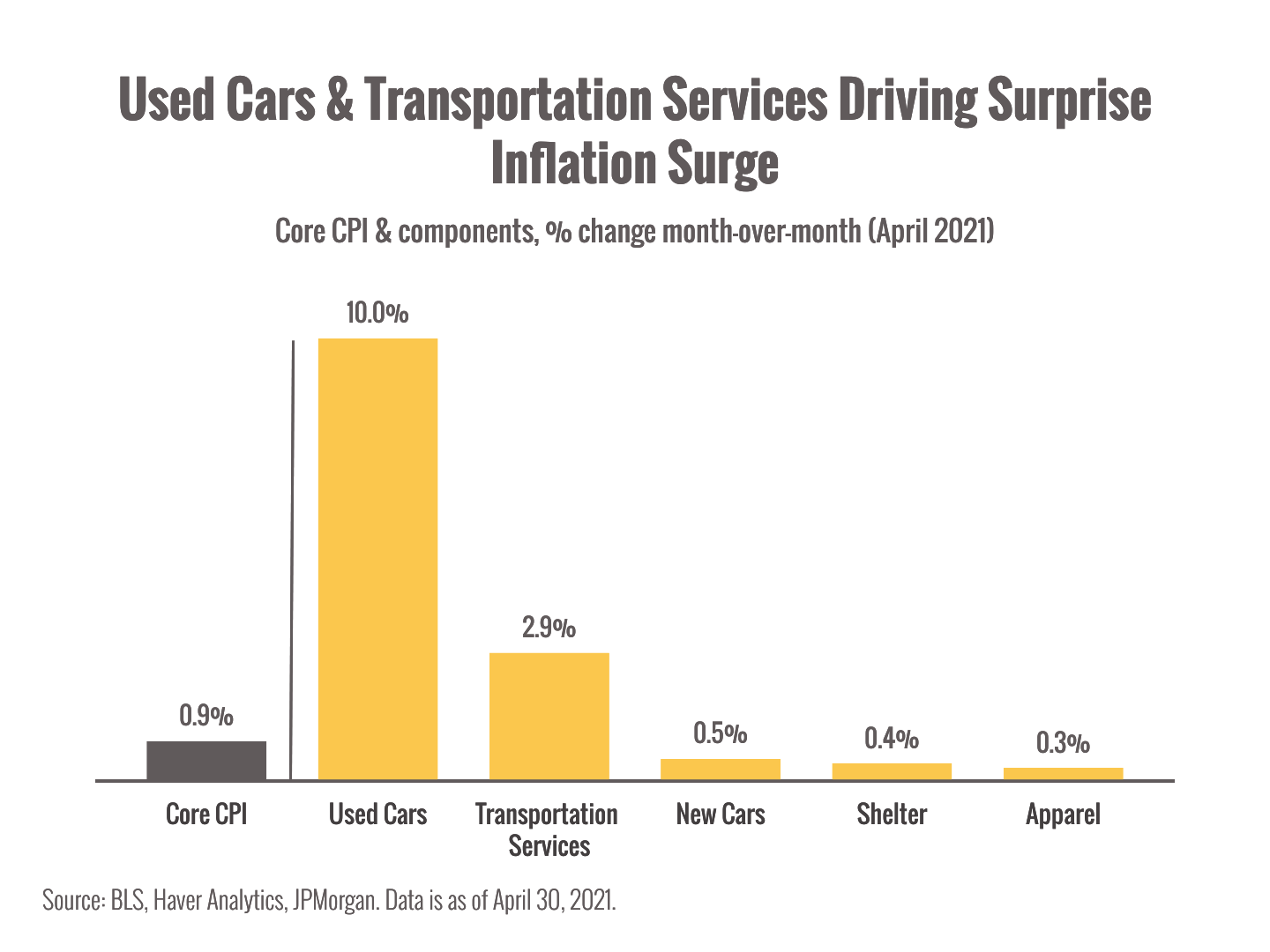

The Consumer Price Index (CPI), one of the major indexes economists use to track inflation, showed a surprising spike in April, igniting fears of runaway inflation.

Core CPI (which excludes the highly volatile categories of energy and food) showed a 0.9% increase in April month-over-month and 3.0% year-over-year. That’s much higher than the expected 0.3% and 2.3%, respectively.1

However, digging a bit deeper, we see that just two categories of goods (used cars and transportation services) accounted for the vast majority of the surge.2

That suggests things like flights and train travel suddenly became more expensive after a year of rock-bottom prices.

Is that runaway inflation or the normalization of prices as the world reopens?

We can’t tell from a single data point, but it’s not unusual to see prices increase in sectors that experienced a severe slowdown last year.

And the jump in used car prices? Well, many folks are turning to the second-hand market right now, in part because new cars are caught up in global supply chain bottlenecks for things like semiconductors and raw materials.3

Inflation is something to keep an eye on, especially in a year when so many of the usual variables have been thrown into flux. An ongoing surge in prices could hurt our wallets as our dollars buy less over time.

However, a single monthly spike following a very weird period for the economy is not cause for alarm yet; we should prepare ourselves for more odd numbers coming out of different parts of the economy in the weeks and months to come.

Shortages of everything from ketchup to gasoline could lead to price increases and fluctuations as supply chains attempt to disentangle from pandemic disruptions.4

Should we expect markets to react to inflation? How should we deal with it?

A negative market reaction in the short term is not surprising after weeks of strong performance. We should expect volatility ahead as we (and the economy) adjust to a post-pandemic world.

But remember, the stock market is a powerful hedge against inflation over the long term. During the last 90+ years, stocks have gained 9.8% per year while inflation has averaged 3% per year.

The engines of this elegant defense are the earnings and dividends of the great companies that we own which grow at healthy clips above inflation.

Plus value stocks, which play a key role in our NorthStar Globally Diversified Portfolio, tend to perform better than growth stocks when inflation surges.

Whether it’s high or low inflation, never lose sight of this enduring truth:

All lastingly successful investing is goal-focused and planning-driven.

All failed investing is market-focused and current events-driven.

Successful investors act continuously on her or his lifetime plan.

Failed investors react continually to economic (inflation!) and market developments.

Until next time,

Chris

Chris Mullis, Ph.D.,CDFA® Founding Partner & Financial Planner

This is probably our most important share of 2021.

Tell us how well you appreciate this video and we’ll tell you how successful an investor you’ll be.

When an American’s portfolio suddenly declines 14% from a previous peak, he will never calmly announce, “I’m experiencing a perfectly ordinary, unsurprising, and above all temporary correction — indeed, merely the average intra-year correction of the last 65 years — and it will have no lasting effect on my long-term return.”

Instead, he screams, “I’ve lost 14% of my money, and there’s no end in sight!” as CNBC trumpets the apocalypse du moment.

Watch this video and be able to make that exceptionally calm and financially productive proclamation…”I’m experiencing a perfectly ordinary, unsurprising, and temporary…”

Here’s a quick guide to the market frenzy you’re seeing in the headlines.

But before we dive in, please don’t lose sight of this essential fact: all this mayhem means very little to the majority of investors. If you’re properly diversified, your 401(k) is fine and your IRA is still doing its thing.

Our clients know that their NorthStar portfolios are firewalled from craziness like this thanks to this critically important truth: We will never own enough of any one idea to make a killing in it. We will never own enough of any one idea to get killed by it.

In fact, it is our considered opinion that owning individual stocks, shorting stocks, and hedge funds are all a form of the Sirens’ song (more on that in the last section below).

Now let’s look at how we got here, and what the impact is for average investors.

Long email ahead. (Buckle up, it’s a little complicated.)

What is GameStop and why does everyone care?

GameStop is a brick-and-mortar video game chain that hit hard times in the pandemic. Like many distressed companies, it was targeted by short sellers betting that the stock’s price would go down.1

Basically, short sellers do the opposite of most investors. They try to make money when a stock’s price falls. They borrow shares from their brokerage for a fee, immediately sell them, and plan to buy them back later at a lower price when the price falls. Shorting is a strategy used by certain types of hedge funds.

What’s a short squeeze?

Shorting stocks is risky since any positive news or interest in a company can drive the stock’s price up. When short sellers bet wrong and a stock’s price rises, they can be forced to buy shares at higher prices to cover their losses (or pony up more collateral).

A squeeze happens when short sellers scramble to buy shares to cover their positions when the stock price is rising. The more investors who buy and hold those shares, the harder it is for short sellers to find shares to buy (exposing them to potentially huge losses).

With me so far?

Where does Reddit come in?

After it became clear that short sellers were betting on GameStop’s demise, the popular company became the focus of amateur traders on the popular WallStreetBets forum on Reddit, a popular community of chatrooms and forums.

By banding together and coordinating buying activity, these small-time traders boosted the stock’s price far above what the company’s financial fundamentals support, putting pressure on the hedge funds betting the other way.2

The stock went viral.

Why?

Social media chatter + free trading apps like Robinhood + bull market + new investors with time on their hands = FRENZY

Is it illegal? That’s a stretch. These armchair traders are egging each other into speculative bets, but we don’t think it rises to the level of illegal market manipulation. However, regulators might feel differently.

Is it bad for markets? The battle between gleeful amateurs pushing prices up and hedge funds scrambling to force prices down has led to some of the highest volume trading days on record and cost short sellers billions.3

Is this David vs. Goliath?

We don’t think the GameStop bubble is just about greed or boredom or euphoria. We see a powerful narrative at play.

We think a lot of these small traders are angry at the perception that All-Powerful Wall Street is pulling strings and using their connections to hurt mom-and-pop investors. They see this as an opportunity to stick it to the big-money pros by using their own strategies against them.

It’s new school vs. old school. Rebels vs. the Empire. Bueller vs. Principal Rooney. Reddit vs. CNBC.

So, should I be investing in GameStop?

No! GameStop’s stock is massively inflated and trading has been halted multiple times because of its meteoric rise.4 At this point, it looks like folks are piling in just to say they were there.

When the bubble bursts, it’ll be a rush to sell and many GameStop holders will end up losing most of their investment.

(It might already be happening by the time you read this.)

We’ve seen frenzies like this many times before. Tulip mania in the 1630s, the Nifty Fifty in the 1970s, the dot-coms in the 1990s, Bitcoin’s multiple bubbles over the last decade, etc. We’ll see more in the future.

Why are people angry at Robinhood?

Amidst the buying frenzy, Robinhood and other popular brokerage platforms suddenly restricted trading on several red-hot stocks, including GameStop.5

Protests erupted from investors, many market pros (not the short sellers, obviously), lawmakers and more.

Did Robinhood halt trading to appease big investors at the expense of small investors? Did they do it to protect markets from manipulation and liquidity problems?

What are the implications of this frenzy?

There’s no predicting the future, obviously, but we think a few things are likely. Most bubbles end naturally when the euphoria turns to panic, folks start selling, and the price crashes.

However, it’s also possible that regulators will step in if they think there’s risk to markets (or they see too many investors getting hurt).

We think this ride’s going to end in tears for many folks caught up in it. But I’m not sure who will be crying hardest.

Finally, The Sirens

Remember the story from The Odyssey, where Ulysses and his crew have to sail past the island of the Sirens?

The Sirens, you’ll recall, sing a song so seductively sweet that no sailors can resist it: they must steer toward the song, only to be dashed upon the rocks surrounding the island.

Ulysses, being the conniver he is, looks to have it both ways: he wants somehow to hear the song while not getting shipwrecked. So he stuffs all his crewmen’s ears with wax, and has himself lashed to his ship’s mast — ordering his mates on pain of death not to obey him if he orders them to change course.

Individual stocks (GameStop!), shorting, and hedge funds are all part of the Sirens’ song, and they are singing it to you and to millions of other investors, who are perhaps losing touch with how fatal it will be to their long-term plans if the “miracle” implodes.

In this analogy, we are the one true friend who accepts the responsibility of lashing you inextricably to the mast. And diversification is the rope.

The twists and turns so far make it seem like 2020 is dragging into a second season.

As Americans, we’re shocked and worried, and we’re wondering how political disagreements turned into excuses for violence.

As a financial professionals, we know that the politics, protests, and rioting in DC are just one factor affecting markets.

We honestly don’t know what will happen over the next few weeks, but we can help you understand how it affects you as an investor.

Why did markets surge the day the Capitol was attacked?

While the world watched the violence in DC with horror, markets quietly rallied to new records the same day.1

That’s weird, right?

Well, not really.

We think it boils down to a few things.

Computers and algorithms are dispassionate, executing trades regardless of the larger world.

Markets don’t always react to short-term ugliness. Instead, they reflect expectations about economic and business growth plus a healthy dose of investor psychology.

With elections officially at an end, political uncertainty has dissipated.

Overall, we think investors are looking past the immediate future and hoping that vaccines, increased economic stimulus, and economic growth paint a positive picture of the future.

The Democrats control the White House and Congress. What does that mean for investors?

If you’re like a lot of people, you might think that your party in power is good for markets and your party out of power is bad.

That makes for a stressful experience every four years, right?

Fortunately, that’s not the case at all. Markets are pretty rational with respect to politics and policy.

While businesses and investors generally dislike increased taxes and corporate regulation, the Democrats hold such slim majorities in the House and Senate that it limits their ability to pass many big policy changes.

Also, the Democrats’ immediate agenda is very likely to be focused on fighting the pandemic and passing more stimulus aid, both of which should support stock prices.

Does that mean markets will continue to rally?

No guarantees, unfortunately. With all the frothy market activity and rosy expectations about the future, bad news could knock stocks down a peg or two.

A correction is definitely possible, and some strategists think certain sectors are in a bubble.

Bottom line, expect more volatility.

Well, what comes next?

We wish we could tell you.

We’re hoping that the vicious, divisive politics will come to an end after the inauguration, and the politicians can get back to work getting us through the pandemic.

We’re optimistic that the light at the end of the tunnel is getting closer and we can start going back to normal.

We’re proud of what scientists and medical professionals have been able to accomplish in such a short amount of time.

We’re grateful for the folks around us.

We’e hopeful about the future.

How about you?

What’s your take? We’re interested to hear your thoughts.

Warmly,

The NorthStar Team

P.S. Tax laws are likely to change under the Biden presidency. We don’t know exactly when they’ll happen or what they’ll look like, but we’ll be in touch when we know more.

Once in a very great while, there comes a year in the economy and the markets that may serve as a tutorial — in effect, a master class in the principles of successful long-term, goal-focused investing. Two thousand twenty was just such a year.

On December 31, 2019, the Standard & Poor’s 500 Stock index closed at 3,230.78. This past New Year’s Eve, it closed at 3,756.07, some 16.3% higher. With reinvested dividends, the total return of the S&P 500 was about 18.4%.

From these bare facts, you might infer that the equity market had, in 2020, quite a good year. As indeed it did. What should be so phenomenally instructive to the long-term investor is how it got there.

From a new all-time high on February 19th, the market reacted to the onset of the greatest public health crisis in a century by going down roughly a third in five weeks. The Federal Reserve and Congress responded with massive intervention, the economy learned to work around the lockdowns — and the result was that the S&P 500 regained its February high by mid-August.

The lifetime lesson here: At their most dramatic turning points, the economy can’t be forecast, and the market cannot be timed. Instead, having a long-term plan and sticking to it — acting as opposed to reacting, which is our clients’ and our firm’s investment policy in a nutshell — once again demonstrated its enduring value.

(Two corollary lessons are worth noting in this regard. (1) The velocity and trajectory of the equity market recovery essentially mirrored the violence of the February/March decline. (2) The market went into new high ground in midsummer, even as the pandemic and its economic devastations were still raging. Both outcomes were consistent with historical norms. “Waiting for the pullback” once a market recovery gets under way, and/or waiting for the economic picture to clear before investing, turned out to be formulas for significant underperformance, as is most often the case.)

The American economy — and its leading companies — continued to demonstrate its fundamental resilience through the balance of the year, such that all three major stock indexes made multiple new highs. Even cash dividends appear on track to exceed those paid in 2019, which was the previous record year.

Meanwhile, at least two vaccines were developed and approved in record time, and were going into distribution as the year ended. There seems to be good hope that the most vulnerable segments of the population could get the vaccines by spring, and that everyone who wants to be vaccinated can do so by the end of the year, if not sooner.

The second great lifetime lesson of this hugely educational year had to do with the presidential election cycle. To say that it was the most hyper-partisan in living memory wouldn’t adequately express it: adherents to both candidates were genuinely convinced that the other would, if elected/reelected, precipitate the end of American democracy.

In the event, everyone who exited the market in anticipation of the election got thoroughly (and almost immediately) skunked. The enduring historical lesson: never get your politics mixed up with your investment policy.

Still, as we look ahead to 2021, there remains far more than enough uncertainty to go around. Is it possible that the economic recovery — and that of corporate earnings — have been largely discounted in soaring stock prices, particularly those of the largest growth companies? If so, might the coming year be a lackluster or even a somewhat declining year for the equity market, even as earnings surge?

Yes, of course it’s possible. Now, how do you and we — as long-term, goal-focused investors — make investment policy out of that possibility? Our answer: we don’t, because one can’t. Our strategy, as 2021 dawns, is entirely driven by the same steadfast principles as it was a year ago — and will be a year from now.

We have been assured by the Federal Reserve that it is prepared to hold interest rates near current levels until such time as the economy is functioning at something close to full capacity — perhaps as long as two or three more years.

For investors like us, this makes it difficult to see how we can pursue our long-term goals with fixed income investments. Equities, with their potential for long-term growth of capital — and especially their long-term growth of dividends — seem to us the more rational approach. We therefore tune out “volatility.” We act; we do not react. This was the most effective approach to the vicissitudes of 2020. We believe it always will be.

As always, we’re here to talk any and all of these issues through with you.

We wish you a happy, healthy, prosperous and fulfilling 2021.

The coronavirus is still very much with us, as is much of the economic dislocation occasioned by the resulting lockdowns. Granted, we are evidently closing in rapidly on a vaccine—indeed, a number of vaccines. But it may be quite some time yet before most of us will get access to a vaccine, and frustration may abound. Moreover, in the coming weeks we will have to go through a hyperpartisan presidential election, with a variety of voting issues we’ve never had to deal with before.

So before we’re further engulfed by these multiple unknowns, we want to take a moment to review what we as investors should have learned — or relearned — since the onset of the great market panic that began in February/March. And that ended when the S&P 500 Index regained its pre-crisis highs in mid-August.

The lessons, it seems to me, are:

No amount of study — of economic commentary and market forecasting — ever prepares us for really dramatic events, which always seem to come at us out of deep left field. Thus, trying to make investment strategy out of “expert” prognostication — much less financial journalism — always sets investors up to fail. Instead, having a long-term plan, and working that plan through all the fears (and fads) of an investing lifetime, tends to keep us on the straight and narrow, and helps us to avoid sudden emotional decisions.

The equity market went down 34% in 33 days. None of us have ever seen that precipitous a decline before — but with respect to its depth, it was just about average. That is, the S&P Index has declined by about a third on an average of every five years or so since the end of WWII. But in those 75 years, the S&P Index has gone from about 15 to where it is now. The lesson is that, at least historically, the declines haven’t lasted, and long-term progress has always reasserted itself.

Almost as suddenly as the market crashed, it completely recovered, surmounting its February 19 all-time high on August 18. Note that the news concerning the virus and the economy continued to be dreadful, even as the market came all the way back. We think there are actually two great lessons here. (1) The speed and trajectory of a major market recovery very often mirror the violence and depth of the preceding decline. (2) The equity market most often resumes its advance, and may even go into new high ground, considerably before the economic picture clears. If we wait to invest before we see unambiguously favorable economic trends, history tells us that we may have missed a very significant part of the market advance.

The overarching lesson of this year’s swift decline and rapid recovery is, of course, that the market can’t be timed — that the long-term, goal-focused equity investor is best advised to just ride it out.

These are the investment policies our clients have been following all along, and if anything, our experience this year has validated this approach even further.

A word now — really just a repetition of what we’ve said to you before — about the election. Simply stated: it’s unwise in the extreme to exit the quality equity investments you’ve been accumulating for your most cherished lifetime financial goals because of the uncertainties surrounding the election.

Aside from the self-inflicted wound of incurring capital gains taxes, your chances of getting out and then back in advantageously are historically very poor, nor can we possibly be helpful to you in attempting to do so. As we have done all year — and as we do every election year — we urge you to just stay the course.

As always, we’re here to talk any and all of these issues through with you.

Thank you, as always, for your support and your engagement. It is a privilege to know you.

Everyone wants to know how to earn the most money with their investments. We all want that, right? Well, the answer is so simple you can scribble it on a cocktail napkin. We made a short video to share that sketch with you and to give you the answer. But be warned! There’s a paradoxical catch — “simple” doesn’t necessary mean “easy.”

Transcript:

Everyone wants to know how to earn the most money with their investments. We all want that, right? Well, the answer — The Investment Answer — is so simple you can scribble it on a cocktail napkin. That’s exactly what my friend and New York Times columnist Carl Richards has done for us in this sketch.

These are the factors that drive portfolio returns in the real world. The big circle on the left are the heavy hitters in rank order of importance. While the tiny circle in the bottom right reflects what doesn’t work.

By far the most influence is wielded by your behavior as an investor. That’s #1 by a wide margin. Do you take the long view with your investments? Do you understand that short-term volatility is normal? And, do you appreciate that pullbacks are temporary and the uptrend is permanent? The second biggest driver of returns is the percentage of stocks in your portfolio. And then what kind of stocks? Small companies have outperformed large companies over the long haul. And, value companies — those priced at a discount relative to their intrinsic value — outperform growth companies over the long term.

What’s not part of the investment answer? What’s is not a path to investing success? Marketing timing, stock picking, CNBC, and your brother-in-law’s advice.

Our team of PhDs at NorthStar Capital Advisors created this data-driven and time-tested approach for carefully managing our clients’ money. It’s formed by observation, by academic research, and by our real-world experience of successful investing over the past 14+ years.

But knowing the answer doesn’t necessarily translate to the success that we all seek. Think about our health. We all know how to live a healthy life, right? Nutrition and exercise. There’s the answer — The Health Answer — But do we faithfully practice these day in and day out, year after year?

To quote Warren Buffet, one of the greatest investors of all time, “Investing is simple, but not easy.” There’s the crucial paradox. “Investing is simple, but not easy.”

We practice the principles of long-term investing that have most reliably yielded favorable long-term results. Those principles are: planning; a rational optimism based on experience, and finally — patience and discipline. If you have any questions about “the investment answer” or that paradox of simple but not easy? We would love to hear from you.

As always, thank you for watching, we appreciate the opportunity to support your financial success, and please be well.

Need some distractions from your day? Scroll down to the bottom of this article. There’s a baby jaguar.

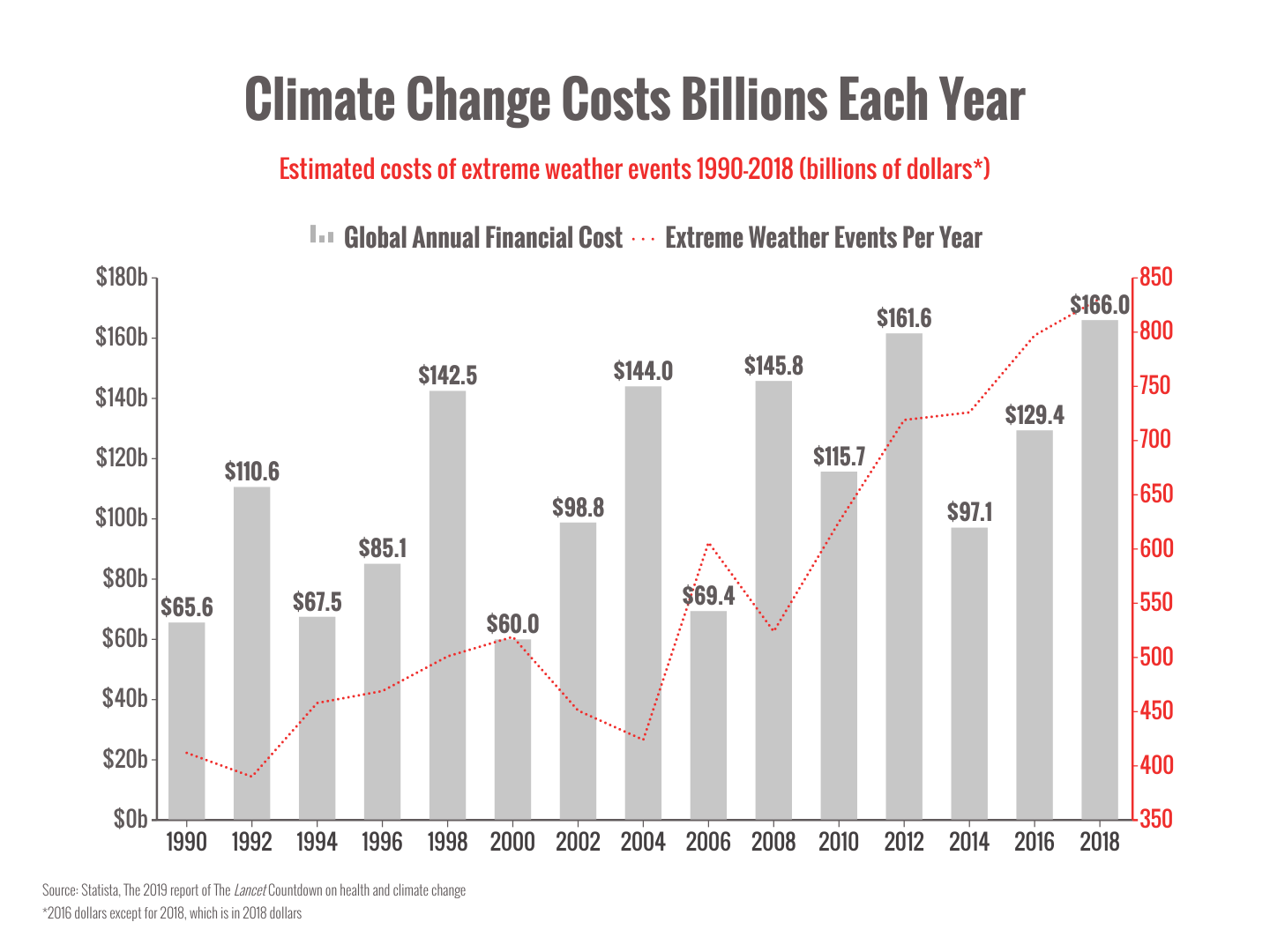

But first, let’s talk about climate change.

The wildfires, hurricanes, and floods we’ve seen in 2020 (on top of an already-awful global pandemic) make this an important conversation to have.

Think climate change isn’t an issue? Well, the market consensus is moving in the other direction.

Insurers, government entities, and large investors are treating climate change as a major systemic risk to financial markets.1

Why? Because many companies and sectors are at risk from the costly heatwaves, wildfires, droughts, floods, and hurricanes that come with a warming planet.2

Do scientists agree on climate change? Yes, the vast majority of actively publishing climate scientists – 97 percent – concur that humans are causing global warming and climate change.

Most of the leading science organizations around the world have issued public statements expressing this, including international and U.S. science academies.3

So, what does climate change mean for investors?

Investors worry that climate risk could cause the prospects of certain companies to drop dramatically and ricochet throughout the financial system (much like what happened during the 2008 financial crisis).

But, unlike a global issue such as the coronavirus, the effects will play out differently around the country and the world.

Flood- or wildfire-prone areas could experience disruptions in business or find it difficult to insure homes and structures against damage.

Agriculture could be damaged by droughts and heat stress.

Already-warm areas could become too hot for comfortable habitation.

But, if the world goes all-in on sustainability too suddenly, there’s also a danger that the “transition risk” caused by new regulations or widespread shifts in energy use could also hurt markets or certain sectors of the economy.4

Well, what’s the good news?

There’s always hope. Many of the worst effects of climate change will play out over years and decades, not weeks and months.

There’s time for people, businesses, and governments to adapt. And humans are infinitely adaptable.

And there’s hope that the worst-case scenarios about a hotter world might not come to pass.5

I believe that optimism and pessimism can (and often should) co-exist.

I’m pessimistic about the climate path we’re on.

I’m optimistic that we will make the changes needed to get on the right path and steer away from the worst effects of climate change.

As a financial planner and wealth manager, I’m also staying on top of the growing body of risk models and research to help my clients chart a path through an increasingly uncertain world.

Ok, enough about climate change. Here are the distractions I promised.

What do you think? Are you worried about climate change?

What do you think we should do about it?

Warmly,

Chris

Chris Mullis, Ph.D.,CDFA® Founding Partner Financial Planning. Wealth Management. Since 2006AskNorthStar.com (704) 350-5028

P.S. Markets have been volatile this month. It’s to be expected with so much uncertainty swirling about. We’ll reach out if I have anything critical to share.