You Are Your #1 Threat

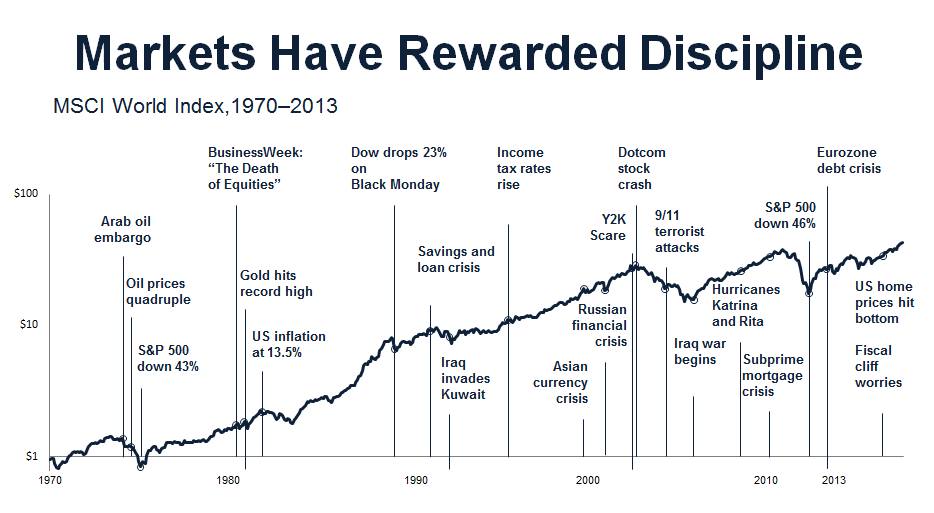

The chart above from Dimensional Fund Advisors is an excellent demonstration of the resilience of the market. Each event marked on the timeline was accompanied by thousands of articles and TV reports discussing at great length how bad things were going to get and what you supposedly needed to do. Despite all that noise, the market just keeps powering up over the long term.

The chart above from Dimensional Fund Advisors is an excellent demonstration of the resilience of the market. Each event marked on the timeline was accompanied by thousands of articles and TV reports discussing at great length how bad things were going to get and what you supposedly needed to do. Despite all that noise, the market just keeps powering up over the long term.

Individual investors (that’s you!) constitute the number one threat to their own portfolio. How’s that? In the face of market stress and volatility, they usual reaction is some combination of the following :

- Fleeing into the arms of a charlatan who purports to having predicted it

- Buying into Black Swan funds and protective products that cap all future upside and cost a fortune

- Obsessing over hedges after the fact

- Selling out with big (permanent) losses and sitting in cash

- Freezing 401(k) contributions or having retirement cash allocated to money market funds

- Excessive trading

- Planting a flag and being unwilling to publicly change our minds in the face of new evidence

- Throwing money at bizarre alternatives like coins, bars, bricks and bullion which have no proven ability to fund a retirement

- Conflating political views with investment expectations

According to adivsor Josh Brown, “every one of these things is extremely detrimental to our financial health. In some cases, the damage could be irreversible. Nothing kills the long-term returns of a portfolio like throwing away the playbook in the heat of a market crisis.”

Source: TRB

Simple, Bedrock Rules on Personal Finance

Financial columnist Brett Arends’ final piece for the Wall Street Journal is absolutely foundational!

Financial columnist Brett Arends’ final piece for the Wall Street Journal is absolutely foundational!

Ignore economic and financial forecasts. Their purpose is to keep forecasters employed. Most professional economists were blindsided in 2008 by the biggest financial collapse in 70 years—and by the stock market’s recovery.

Ignore “expert” stock picks. The stocks that Wall Street experts like most generally fare no better than those they like least—or stocks picked at random.

Keep it simple. Complicated financial strategies and investments are mostly designed to enrich managers and salesmen.

Buy individual stocks only as a gamble. Never buy fashionable investments.

Put most of your long-term portfolio into equities. While equities are volatile, they generally produce the best long-term returns—typically about 4% to 5% a year above inflation. But remember to hang on when they plummet.

Invest globally, not just in the U.S. Foreign stock markets, in the aggregate, are no riskier than U.S. markets and offer terrific diversification.

Buy Treasurys, too: In addition to stocks, own some long-term Treasury bonds and some Treasury inflation-protected securities. These are likely to hold their value, or even go up, when stocks crash.

Save early, save often. Time and patience are the investor’s best friends.

Use those free shelters. Contribute as much as possible to your company’s 401(k) plan or equivalent (such as 403(b) or 457), and at least enough to get the company match. If you can, contribute to individual retirement accounts for yourself, and a nonworking spouse, as well.

Plan for a long life. A third of your adult life could come after you’re 65. Try to pay off your mortgage, and save at least 10 times your annual salary, by the time you retire. Delay taking Social Security for as long as you can up to the age of 70, to maximize each monthly check.

Beware of buying your employer’s stock. Your job there is probably financial exposure enough.

Protect your nest egg. Don’t drain your retirement savings to pay for your child’s college education. Likewise, don’t empty your 401(k) or IRAs to start a business. You will be taxed and penalized on the withdrawals even if you lose the money.

Teach your children about money. Teach them early and often. No one else will, and they will have to make their own way.

Don’t Drop the Ball…on your New Year’s financial resolutions

It’s early February and “crunch time” for those of us trying to keep our New Year’s resolutions.

It’s early February and “crunch time” for those of us trying to keep our New Year’s resolutions.

If you made a financial resolution to ring in 2015 then you’re not alone! 31% of Americans set financial objectives this year. There are powerful reasons to make and keep such resolutions:

- For those who made a resolution in 2014, 74% say they succeeded in getting at least halfway to their goal

- 51% of people who made a financial resolution at the start of 2014 feel that they are now in a better financial situation

- 42% of those surveyed say sticking to financial resolution is easier than sticking to other popular resolutions

- For those who made a resolution for 2014, 29% say there were completely successful in reaching their goal

- 64% say being encouraged by the progress made is the #1 motivator to stick with financial resolutions

Mandi Woodruff posted the interesting chart below on the leading New Year’s financial resolutions for the past few years. Encouragingly, “develop a plan to reach longer-term goals” is a popular choice, increasing to 14 percent. This is a more than twofold increase since 2011, when it was at a single-digit low of 6 percent.

Need help keeping and tracking your resolutions? Contact us!

Don’t Drop the Ball on Your 2015 Financial Resolutions

Recent Posts

-

Are Financial Advisors Worth It? (DIY vs. Hiring a Pro) August 6,2026

Are Financial Advisors Worth It? (DIY vs. Hiring a Pro) August 6,2026 -

-

Four Things That Can Sabotage Retirement July 9,2026

Four Things That Can Sabotage Retirement July 9,2026 -

Is 2032 the End of Social Security? June 25,2026

Is 2032 the End of Social Security? June 25,2026 -