How much inflation can the country afford before we’re in trouble?

Let’s discuss.

First, let’s get on the same page about some basics.

If you’ve noticed the price of a thing increasing over time (say, your favorite candy bar, postage stamps, or the cost of college tuition), that’s inflation in action.

Retirement planners and investment managers like us keep a keen eye on inflation because the whole point of investing our clients’ money is to keep up with or outpace the rising cost of living.

Economists use the broad increase (or decrease) in prices of goods and services across the country as a measure of economic health.

When inflation is stable and predictable, it’s a sign of a basically healthy, growing economy.

But, high inflation can quickly eat away at the purchasing power of your dollars, indicating that the economy might be overheated.

Deflation, or a decline in prices, can be a warning sign of a shrinking economy.

Recent data highlighted a surprise spike in inflation, indicating that prices increased faster than economists expected last month.1

Could this be a worrisome sign that the economy is overheated? Could $50 burgers be in our future?

Maybe.

On the other hand, could it be a temporary blip caused by the economy emerging from the pandemic-driven slowdown, complicated by supply chain issues?

Very possible.

Are the headlines catastrophizing?

They always are.

Let’s look at the data.

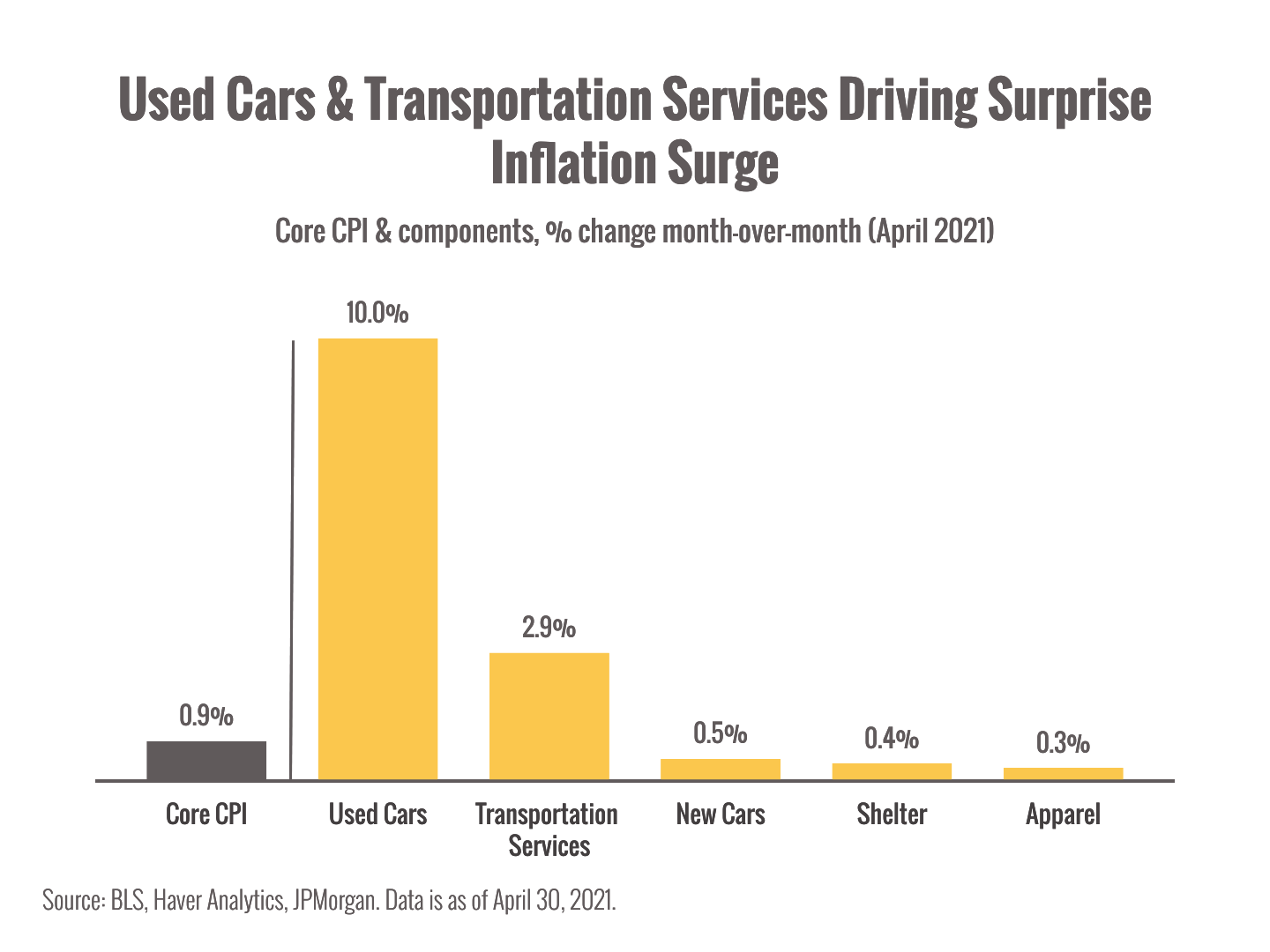

The Consumer Price Index (CPI), one of the major indexes economists use to track inflation, showed a surprising spike in April, igniting fears of runaway inflation.

Core CPI (which excludes the highly volatile categories of energy and food) showed a 0.9% increase in April month-over-month and 3.0% year-over-year. That’s much higher than the expected 0.3% and 2.3%, respectively.1

However, digging a bit deeper, we see that just two categories of goods (used cars and transportation services) accounted for the vast majority of the surge.2

That suggests things like flights and train travel suddenly became more expensive after a year of rock-bottom prices.

Is that runaway inflation or the normalization of prices as the world reopens?

We can’t tell from a single data point, but it’s not unusual to see prices increase in sectors that experienced a severe slowdown last year.

And the jump in used car prices? Well, many folks are turning to the second-hand market right now, in part because new cars are caught up in global supply chain bottlenecks for things like semiconductors and raw materials.3

Inflation is something to keep an eye on, especially in a year when so many of the usual variables have been thrown into flux. An ongoing surge in prices could hurt our wallets as our dollars buy less over time.

However, a single monthly spike following a very weird period for the economy is not cause for alarm yet; we should prepare ourselves for more odd numbers coming out of different parts of the economy in the weeks and months to come.

Shortages of everything from ketchup to gasoline could lead to price increases and fluctuations as supply chains attempt to disentangle from pandemic disruptions.4

Should we expect markets to react to inflation? How should we deal with it?

A negative market reaction in the short term is not surprising after weeks of strong performance. We should expect volatility ahead as we (and the economy) adjust to a post-pandemic world.

But remember, the stock market is a powerful hedge against inflation over the long term. During the last 90+ years, stocks have gained 9.8% per year while inflation has averaged 3% per year.

The engines of this elegant defense are the earnings and dividends of the great companies that we own which grow at healthy clips above inflation.

Plus value stocks, which play a key role in our NorthStar Globally Diversified Portfolio, tend to perform better than growth stocks when inflation surges.

Whether it’s high or low inflation, never lose sight of this enduring truth:

All lastingly successful investing is goal-focused and planning-driven.

All failed investing is market-focused and current events-driven.

Successful investors act continuously on her or his lifetime plan.

Failed investors react continually to economic (inflation!) and market developments.

Until next time,

Chris

Chris Mullis, Ph.D.,CDFA® Founding Partner & Financial Planner

Two things to discuss today: the economy (getting better) and taxes (going up?).

Let’s dive in.

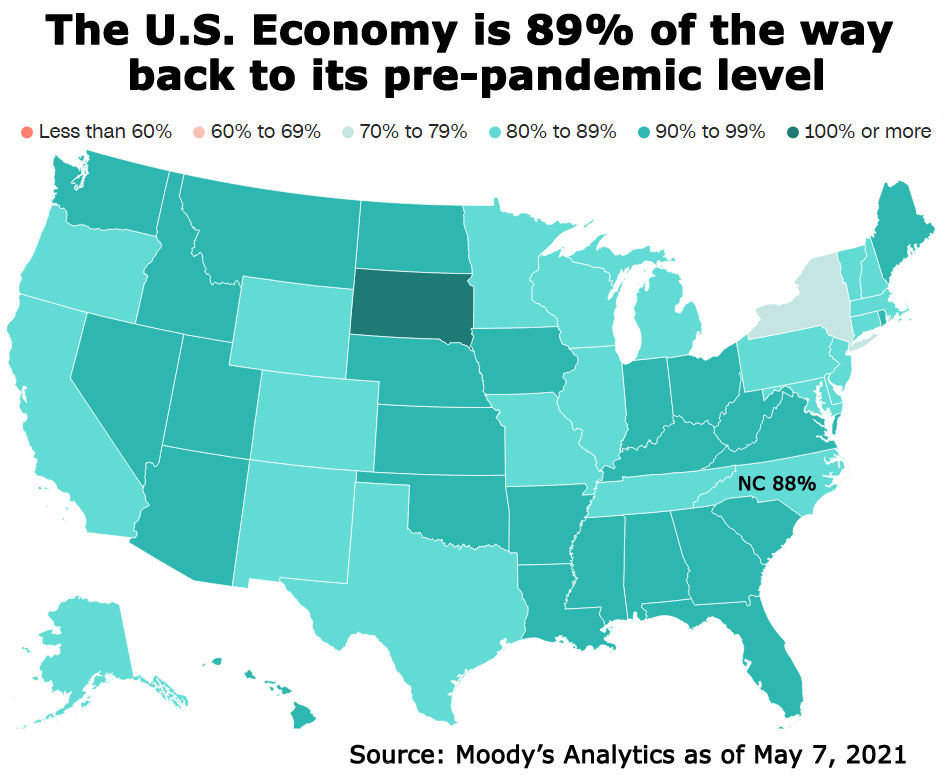

The light at the end of the tunnel is getting closer and brighter.

The economy is booming and we’re getting much closer to pre-pandemic levels of economic growth.1

COVID-19 cases are declining, as the math starts to work for us (instead of against us as it did at the beginning of the pandemic).2 As more folks gain immunity, there are fewer ways for the virus to spread.

All U.S. adults are now eligible for a vaccine.3

Yesterday the first shot was approved in the U.S. for children paving the way for inoculations before summer camps and the start of the next school year.4

Restrictions are easing and areas are opening up for travel, meaning we can start planning those missed vacations and seeing loved ones again.

After over a year of uncertainty and dread, the future is looking up.

Major COVID-19 surges in India and Brazil mean millions are still suffering.5

Viral variants mean the pandemic may not be “over” for a long time and we still need to be careful not to undo all our gains.

Many folks are not experiencing the economic recovery and may need years to recover what they have lost.

However, let’s not let the work ahead take away from the progress we’ve made.

Let’s take a deep breath and appreciate how far we’ve come since March 2020.

… Deep Breath …

Now, let’s talk about taxes.

President Biden just unveiled a plan to increase taxes on high earners to pay for economic reforms as part of the American Families Plan.6

What’s on the table is likely to change as political wrangling continues, but here are a few things we’ve got to consider so far:

A higher top income tax rate of 39.6% (though it’s not clear yet who falls into that top tax bracket).

Raising the top tax rate on long-term capital gains to 39.6%. With the 3.8% Medicare surtax, that means the highest earners could pay a 43.4% rate on gains.

The elimination of the step-up basis for estates, meaning heirs could get stuck paying taxes on capital gains over $1 million (even if nothing has been sold) when they inherit.

This change could impact folks who, for example, inherit family homes that have appreciated in value. They might want to keep the home, but may not be able to afford the tax bill.

So, should I be worried?

Alert and informed, definitely. Anxious and worried, no.

Here’s why:

This is a proposal. It’s got a long way to go before becoming law and the details may change.

It’s still unclear how much impact these proposed changes will actually have. There are many advanced strategies that can help mitigate the impact of higher taxes. That’s why tax and estate strategies matter so much.

A study done by Wharton Business School suggests that tax mitigation strategies could help avoid 90% of the proposed tax increases on capital gains.7

Bottom line, the proposed changes are concerning, especially with so many details left to be determined, but it’s not time to panic.

We’re paying close attention to the process and will be in touch if we feel changes to your strategies are needed.

Be well,

Chris

Chris Mullis, Ph.D.,CDFA® Founding Partner & Financial Planner Reduce Taxes. Invest Smarter. Optimize Income