One big thing you may have heard about in the headlines is the Federal Reserve’s hint that it might start “tapering” soon.1

Could the Fed’s actions cause a market correction or economic slowdown?

Let’s discuss.

First of all, what does ”tapering” mean?

In econ-speak, tapering means winding down the pace of the assets Fed has been buying since last summer.

Why is it a big deal?

Well, the last time the Fed tapered in 2013, during the recovery from the 2008 financial crisis, markets panicked and pitched a “taper tantrum.”2

That’s because traders worried that less Fed support would hurt fundamentals and potentially cause a market downturn.

Now, that old taper tantrum narrative is making folks worry that another market downturn could be ahead of us, especially with concerns about the Delta variant.

Before we dive into what could happen, let’s talk about where we are and how we got here.

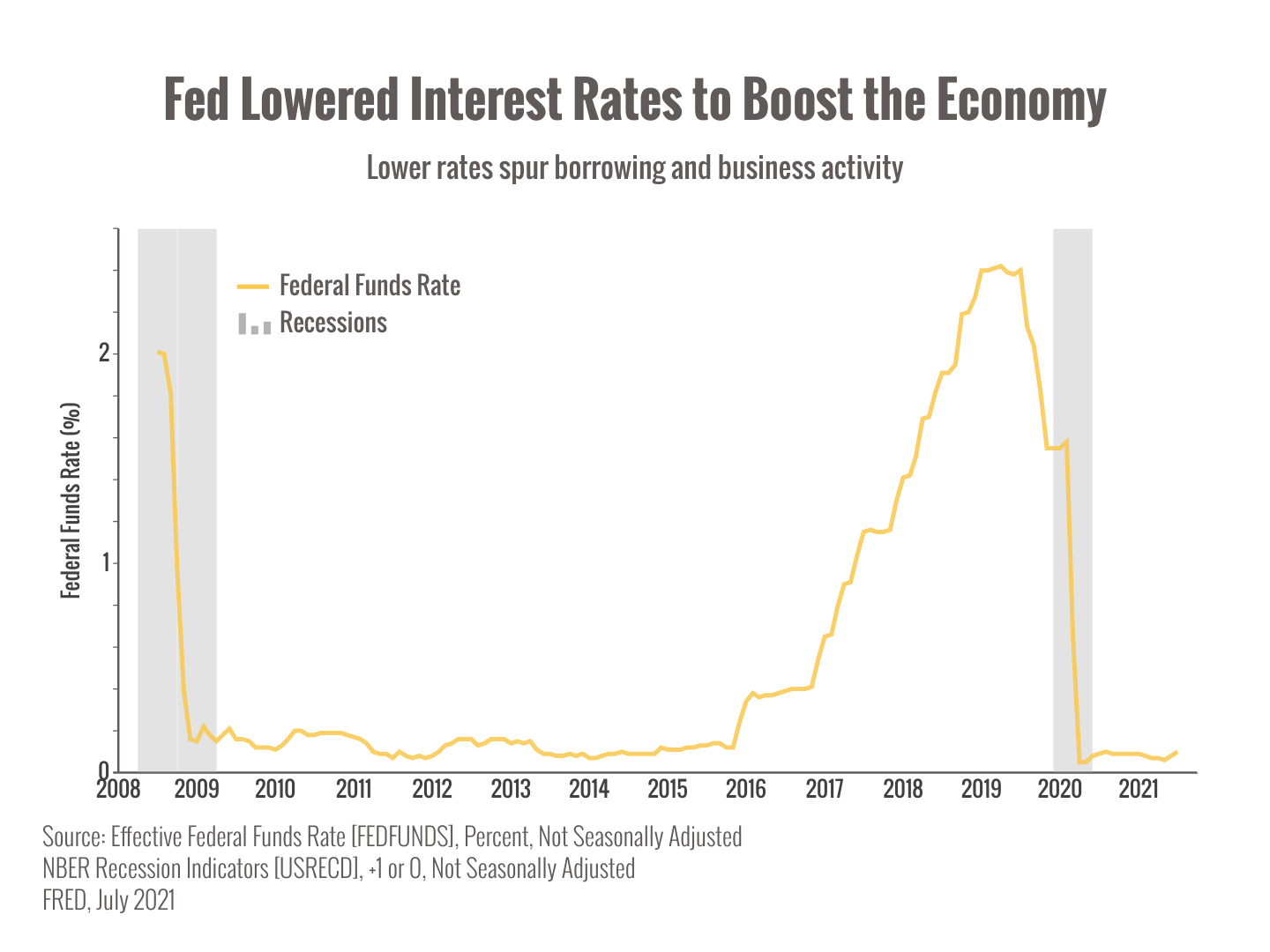

When the pandemic started, the Fed slashed interest rates and began buying $120 billion a month in bonds and mortgage-backed securities to reduce interest rates, lower borrowing costs, and give businesses and the economy a boost.1

However, now that the economy is much stronger, the employment situation has improved, and inflation is a concern, the Fed wants to start paring back those asset purchases to return interest rates to a more “natural” level.

What could that look like?

Obviously, we don’t know exactly when or how the Fed will decide to act, but analysts have some pretty good guesses.

The latest prediction by Bank of America suggests tapering could start this November as the Fed gradually pares back asset purchases through next year.1

The takeaway is that the Fed isn’t going to stop buying assets and raise interest rates immediately.

It’s going to gradually remove the support and see how the economy reacts.

So, will we see another taper pullback?

The main reason folks worry about the Fed reducing support is because of the effect higher interest rates could have on stocks, particularly companies that rely on borrowed money.

However, interest rates are just one piece of the puzzle. Economic fundamentals, earnings, and other factors also weigh on stock prices.

With the benefit of hindsight, we can see that the 2013 taper tantrum wasn’t even that bad. The S&P 500 tumbled 5.8% over the course of a month, but quickly recovered (the caveat here is always this: the past does not predict the future).2

(Sidebar — keep in mind the 2013 taper tantrum decline of 5.8% was less than half of the the average intra-year decline of 13.8% annually that we typically see in the stock market. I.e., yet another piece of “noise”…a semi-random, temporary decline overlaid on the market’s permanent, long-term advance.)

We think the main reason markets declined in 2013 was that investors hadn’t experienced tapering before; they didn’t have context for what the Fed would do.

Since we’ve seen this happen before fairly recently, we think that uncertainty is lessened.

However, we also have other worries to consider: a deteriorating crisis in Afghanistan, continued pandemic worries, and political wrangling over infrastructure.

Any of these factors could derail the bull market.

But it’s not going to be the end of the world.

Pullbacks, corrections, and bear markets are always something we should expect. They happen regularly and are a natural part of markets.

Bearmarkets are common — they occur about 1 in 5 years and there have been 16 since World War II. With the average retirement lasting 30 years, you should expect to encounter 6 bears during this encore of your life.

So, the Fed is one more thing we’re keeping an eye on, and we’ll reach out if there’s more you should know.

Headlines are looking grim again, so let’s pause and take stock.

Why are the headlines terrible?

Because the media loves drama. This is not news to you or us or anyone who pays attention. The 24-hour news cycle is there to whip up emotions and keep us glued to the latest “BREAKING NEWS.”

So, what’s behind the noise and should we worry?

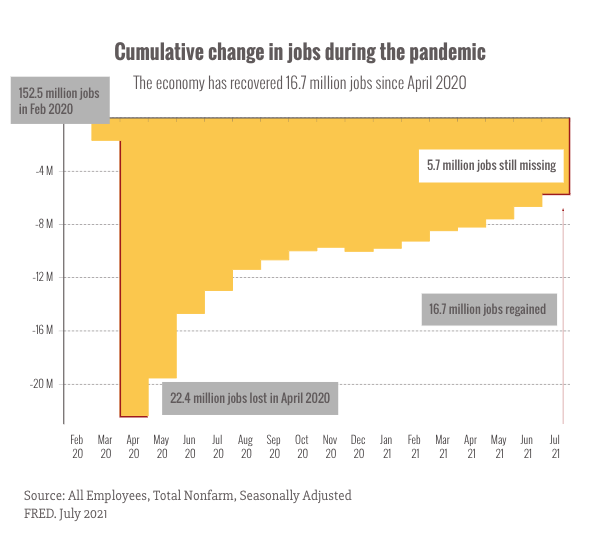

Before we jump into unpacking the news, let’s take a moment and remind ourselves of how far we’ve come since the pandemic began.

You can see it right here in this chart:

We’ve recovered the vast majority of jobs lost since the bottom of the pandemic’s disruption last April. The economy is still missing several million jobs to regain pre-pandemic levels, but we’ve made up a lot of ground, and jobs growth is still strong.1

In fact, there are more job openings right now than job seekers to fill them.2

But there’s an important caveat to the chart above.

The monthly jobs report is what economists call a “lagging” indicator, meaning that it’s telling us where the economy was, not where it’s going.

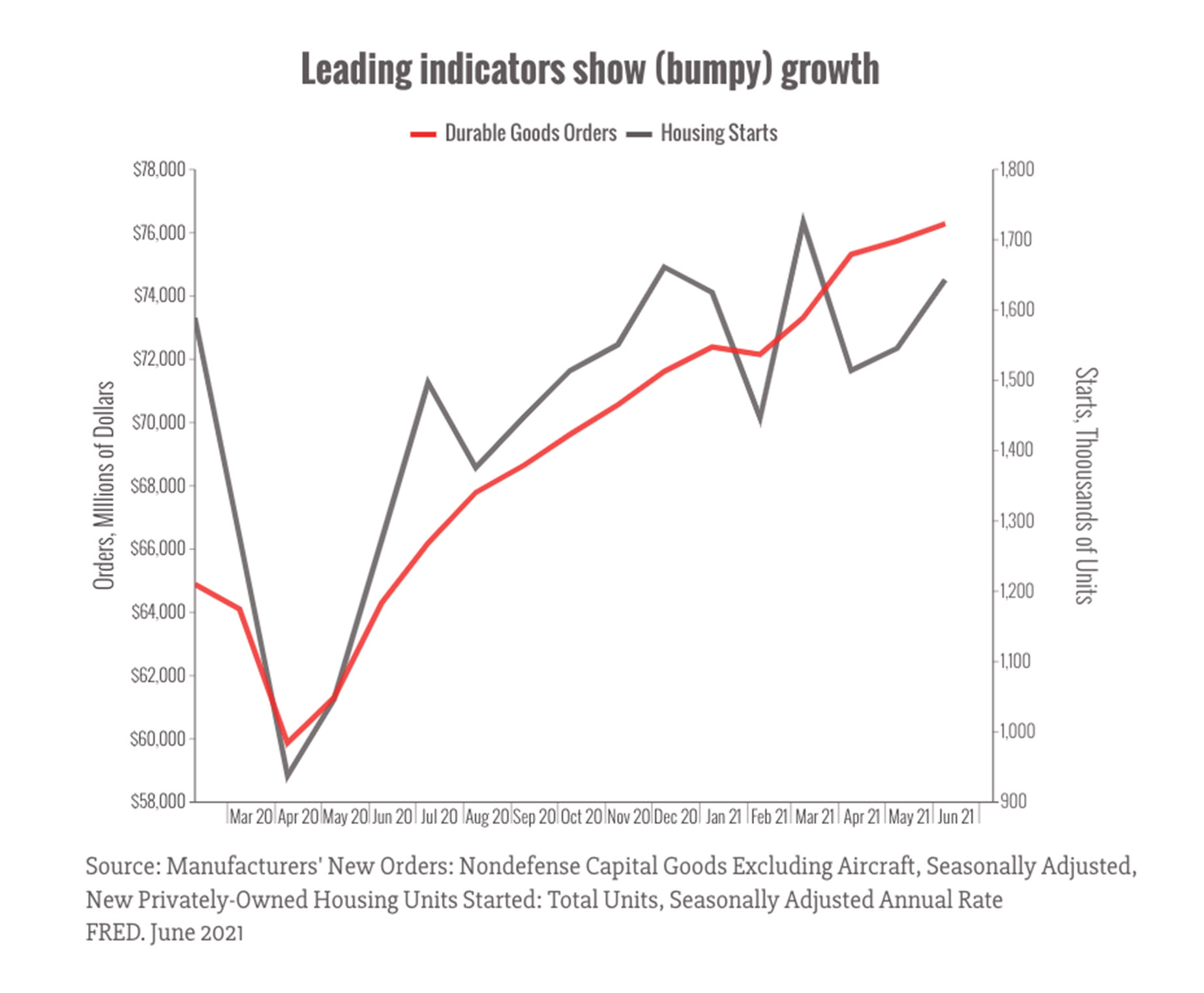

To figure out what might lie ahead, economists turn to “leading” economic indicators that help forecast future trends.

So, what are the leading indicators telling us about the economy?

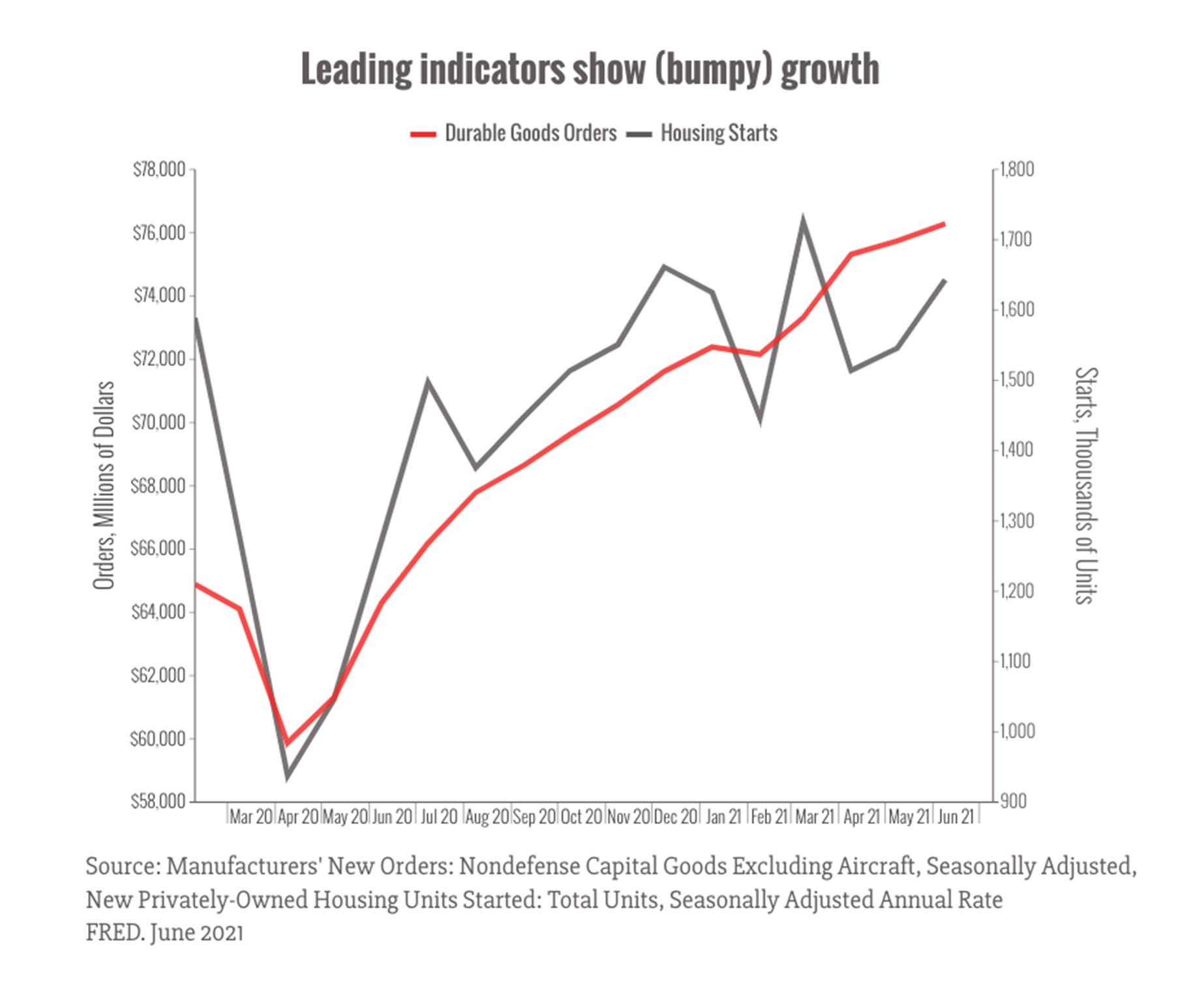

A couple of the most popular indicators are manufacturing orders for long-lasting (durable) goods, since companies don’t like to order expensive equipment unless they expect to need soon.

Another one is groundbreaking (starts) on new houses, which indicate how much demand builders expect for housing.

Let’s take a look:

Both indicators suggest continued (if bumpy) growth. Now, those are just two sectors, and we want to be thorough, so let’s take a look at a composite.

The Conference Board Leading Economic Index (LEI) gives us a quick overview each month of several indicators.

It increased by 0.7% in June, following a 1.2% increase in May, and a 1.3% increase in April, showing broad, but slowing growth.3

What does that tell us? That the economy still has legs.

Will the Delta variant derail the recovery?

New numbers came out this morning showing that retail sales fell slightly (1.1%) in July from the month before, with spending down broadly across categories as concerns about the Delta variant grew.

But most economists, while acknowledging the threat posed by the current rise in Covid cases, aren’t expecting a significant slowdown in consumer spending.

Though a serious slowdown due to the Delta variant seems unlikely, we could potentially see a bumpy fall, especially in vulnerable industries and areas with surging case counts.

There’s also some potentially good news about the Delta variant that we can take from other countries.

India and Great Britain both experienced Delta-driven surges earlier this summer.4

And what happened?

A steep and scary rise in case counts and hospitalizations…followed by a rapid decline.

It seems that these fast-moving Delta waves might burn themselves out.

Unfortunately, these surges come with a painful human cost to patients, overburdened medical staff, communities, and families.

But, if this pattern holds true in the U.S., it doesn’t appear that the economic impact will be heavy enough to derail the recovery.

All this to say, it’s clear that the pandemic is still not over.

But we’ve come such a long way since the darkest days of 2020 and the road ahead still seems bright (if a little potholed).

Please remember to take panicky headlines with a shaker or two of salt.

We’re here and we’re keeping watch for you.

Have questions? Please reach out.

P.S. The bipartisan infrastructure deal is still making its way through Congress, and we don’t yet know what the final details will look like. The Democrat-led infrastructure deal is also in the works, but we’re not likely to see serious movement until the fall. We’ll keep updating you as we know more.