Lowest Thanksgiving Dinner Cost in Five Years

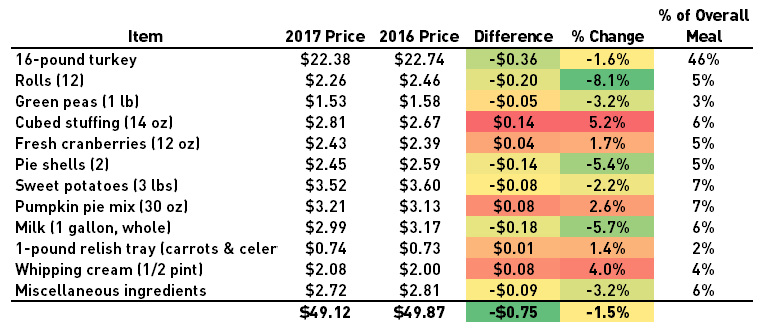

This year’s turkey dinner will cost you 75 cents less or -1.5% compared to last year. The average cost of a classic Thanksgiving Dinner for 10 people is $49.12 according to the American Farm Bureau Federation’s survey. The mild decrease in the turkey index is somewhat at odds with the government’s Consumer Price Index for food eaten at home which increased 0.5% over the past year.

The bird soaks up the lion’s share of the budget at 46% of the meal’s cost. The 16-pound turkey came in at $22.38 this year or $1.40 per pound. The price of most ingredients was quite stable compared to last year. Biggest losers: turkey down $0.36 (-1.6%) and rolls down $0.20 (-8.1%). Biggest gainers: cube stuffing up $0.14 (5.2%), pumpkin pie mix up $0.08 (2.6%), and whipping cream up $0.08 (4.0%).

This is the second consecutive year that the average cost of a turkey dinner decreased and it’s the lowest cost in five years.

Happy Thanksgiving!

Source: AFBF