GameStop + memes = tulips (and Sirens)

|

|

|

|

|

|

| Here’s a quick note about the new economic relief package that Congress passed just yesterday. The Consolidated Appropriations Act, 2021 comes in at over 5,000 pages and the NorthStar Team has been totally nerding out on it!

What’s in the box?

Who is eligible for the stimulus payments? While dependent children under 17 will also receive $600 each, it doesn’t appear that adult dependents like college students or elders qualify for the payments. If your family added dependents in 2020 or you earned too much in 2019 to qualify (but would qualify in 2020), you may not receive full payments immediately but can request additional money once you file your 2020 taxes. If you qualified based on your 2019 income but your 2020 income would have reduced your payment, you won’t have to pay it back; nor will it count as taxable income. How do I claim a stimulus payment? While the IRS hasn’t released a timeline for sending out payments, it’s possible electronic payments could start before the end of the year. When the last round of stimulus passed, the IRS began distributing payments two weeks later; however, plenty of eligible folks still haven’t received them many months later.3 What else do I need to know? Small business relief: Congress included another round of relief for small business owners by extending the Paycheck Protection Program with another $284 billion in forgivable loans. Some of the funds will be set aside for very small businesses, and the PPP is now available to nonprofits and local media outlets.4 An extra $20 billion has also been appropriated for Economic Injury Disaster Loans for businesses in low-income communities, and $15 billion more is earmarked for live venues, movie theaters, and cultural institutions that have been financially damaged by the pandemic. The deal also clarifies that PPP borrowers will be able to deduct expenses paid for with forgiven loans, clearing up a potentially nasty tax issue. Unemployment benefits: The package also extends unemployment benefits of $300/week for another 11 weeks, beginning as early as December 27 and lasting at least until March 14, 2021. A benefits program specifically for contract and gig workers that was slated to expire at the end of the year is also extended through March. What should I do with my payment? If you’re among the very fortunate who don’t need to shore up your finances, we’d recommend putting it toward your retirement savings, other financial goals, or investing it in yourself through a course or hobby. Or even better, donate it to your favorite charity. That’s it for now. We hope you and your loved ones are safe, warm, and well. Questions? We’re here. Reach out at (704) 350-5028. Happy Holidays and Warmest Wishes!

P.S. Wherever there’s money, there are scammers after it. Please be on alert for “official-looking” emails asking you to open an attachment or click a link—they may contain malware. If you get a suspicious email, check the sender’s name and email address to make sure they’re not fake. When in doubt, delete the email. The IRS or Treasury department will not require you to follow emailed instructions to receive a stimulus check. P.P.S. Some great news to share: 556,208 folks were vaccinated against COVID-19 in the first week! That’s the power of human ingenuity and collective effort. We’re so grateful to be seeing some light at the end of this dark tunnel!5 1https://www.washingtonpost.com/business/2020/12/20/stimulus-package-details/ https://www.wsj.com/articles/what-is-in-the-900-billion-covid-19-aid-bill-11608557531 3https://www.wcvb.com/article/when-will-you-get-a-second-stimulus-check/35025504 4https://www.cbsnews.com/news/stimulus-check-600-dollars-eligibility-2020-12-21/ This information is not intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific situation with a qualified tax professional. |

|

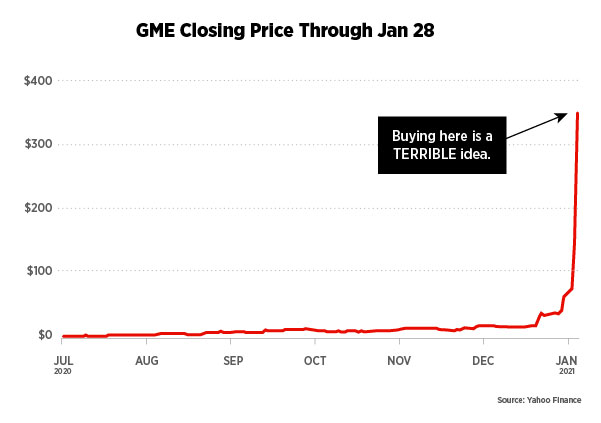

Warren Buffett once said, “The most important quality for an investor is temperament not intellect.”

Warren Buffett once said, “The most important quality for an investor is temperament not intellect.”

Investors very often buy at high prices when the market is hot and attractive, and sell at low prices after observing periods of poor performance.

This leads average investors to severely trail both the S&P 500 index and the Barclays Aggregate Bond Index over long time periods. This is why investors are very often their own worst enemy.

CBS MoneyWatch author Larry Swedroe recommends in this article that you ask yourself if you believe that you’re best served by being your own advisor:

Let’s face it. Buying meaningful gifts for our family and friends is really, really hard.

If you want to give something that has a larger impact long after the holiday season has passed, why not give the gift of financial education and wisdom for living a fulfilled life?

Given the academic background of our firm (“PhDs with passion”), I know the following is going to be a big shocker.

We love reading books and we love giving books as gifts!

Below you’ll find our revised & expanded 2020 NorthStar Guide to Gifts That Pay Off. It’s full of our favorite book and money-related gift recommendations for those ages 4 to 94!

So what’s the most valuable holiday gift of 2020? A fun lesson in financial literacy and living your best life!

Happy shopping!

|

It’s a season for giving thanks. And we wanted to thank you, our dear clients and friends, for allowing us to do what we love every day.

We’re thankful for the opportunity to work toward a mission that we truly believe in — helping families and communities articulate, underwrite, and fully embrace their great lives.

Please know that at Thanksgiving and always, we’re grateful for you.

May the good things in life be yours in abundance throughout the holiday season.

Happy Thanksgiving!

The NorthStar Team