HSA = Tax Triple Play!

Tis the season to select your health insurance plan either through your employer’s offering or the private insurance market. If you’re considering a high-deductible health plan (HDHP), keep in mind that many (but not all!) come with the fantastic opportunity called a Health Savings Account (HSA).

Tis the season to select your health insurance plan either through your employer’s offering or the private insurance market. If you’re considering a high-deductible health plan (HDHP), keep in mind that many (but not all!) come with the fantastic opportunity called a Health Savings Account (HSA).

We love HSAs because they do two things:

- They help you pay for your medical costs either today or in the future

- They are triple tax advantaged

The government makes these accounts triple tax-advantaged because they want to incentivize you to save for your future medical costs. We know as the nation greys and gets older, we need to have a pot of money set aside to cover our potential out-of-pocket costs.

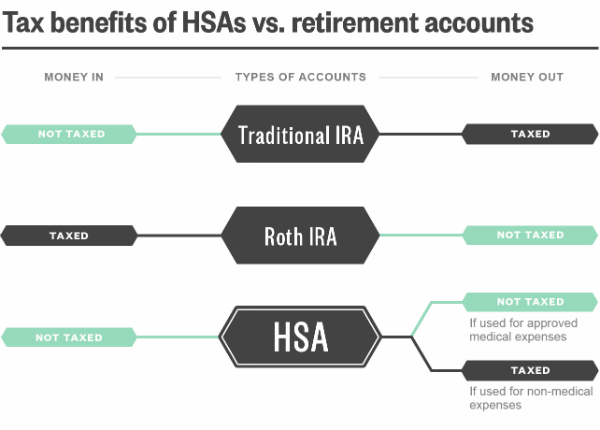

Here’s the triple tax saving advantage:

- When you have an HSA account attached to a high-deductible plan, you get to take a tax deduction on your current your contribution. For families, it’s $6,900 in 2018 ($7,000 in 2019). This means you get to lower your adjusted gross income by $6,900, a tax savings of potentially around $2,000 if you take into account state and federal income taxes. That’s $170 of savings each month if you do a little rounding. That’s pretty incredible. That’s step 1 – you get a tax deduction in current year. If you’re age 55 or older, you eligible for a $1,000 “catch-up contribution” so your can lower your AGI by $7,900 (thus lowering your tax bill by ~$2,300 or $190 a month).

- Layer two of the triple tax advantage is it grows completely tax deferred meaning it is growing without taxation on any appreciation, any dividends, or any income that’s going on a long as that money is sitting in the HSA account.

- Here’s the third layer and really the knockout that makes it an awesome savings tool for the future. If you use the money in the future for medical expenses, your HSA distributions are completely tax free.

(Here’s another cool thing. Once you reach retirement, you don’t have to use your HSA for medical expenses, but if you want them to be tax free, it needs to be medical expenses.)

Be careful when you select a high-deductible health plan (HDHP) to make sure it qualifies for HSA eligibility:

- HDHP minimum deductibles: self-only $1,350; family: $2,700

- HDHP maximum out-of-pocket amounts: self only $6,650; family $13,300

HSAs can be one of your best friends for the future.