10 Ways Financial Advisors Fail Their Clients

- Acting as if they know exactly what the financial markets are doing and why.

- Not being quickly and easily accessible via phone or email.

- Not continuing to research a client’s financial situation for a better solution.

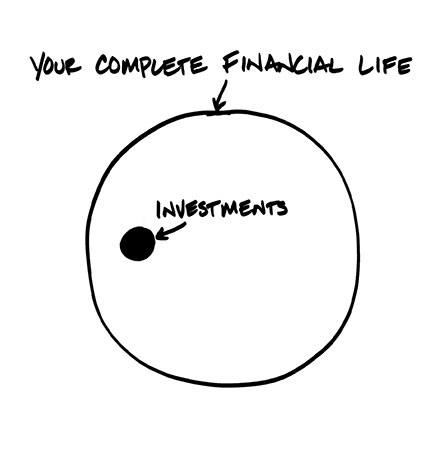

- Not recognizing a total solution by ignoring the client’s portfolios managed by outside firms.

- Not speaking to and working deeply with both members of a couple.

- Limiting recommendations to the products provided by the advisor’s firm.

- Failing to address the risks associated with an investment.

- Failing to give ancillary and holistic advice on a client’s financial issues once the portfolio is established.

- Talking over a client’s head and using jargon.

- Managing client assets without knowledge of the client’s comprehensive financial plan.