Top Investing Ideas for 2016 (or any other year)

It that time of year where the financial media machine is awash with seemingly important predictions for the new year. Despite all the hype, no one can reliably forecast market moving events or trends. Resisting the urge to build investment strategies around faulty forecasts, Bob Seawright provides a quick summary of his top investment ideas for 2016 (or any other year), none of which is dependent upon predicting the future:

- Einstein wisely advised that we keep things as simple as possible, but no simpler. Overly complicated systems, from financial derivatives to tax systems, are difficult to comprehend, easy to exploit and possibly dangerous. Simple rules, in contrast, can make us smart and create a safer world.

- Out of our general fear, we all too frequently bail on our investments and our plans and fail to invest altogether. But if we’re going to succeed, we need to invest, continue to invest and stay the course. Multiple studies have shown that those who trade the most earn the lowest returns. Remember Pascal’s wisdom: “All man’s miseries derive from not being able to sit in a quiet room alone.”

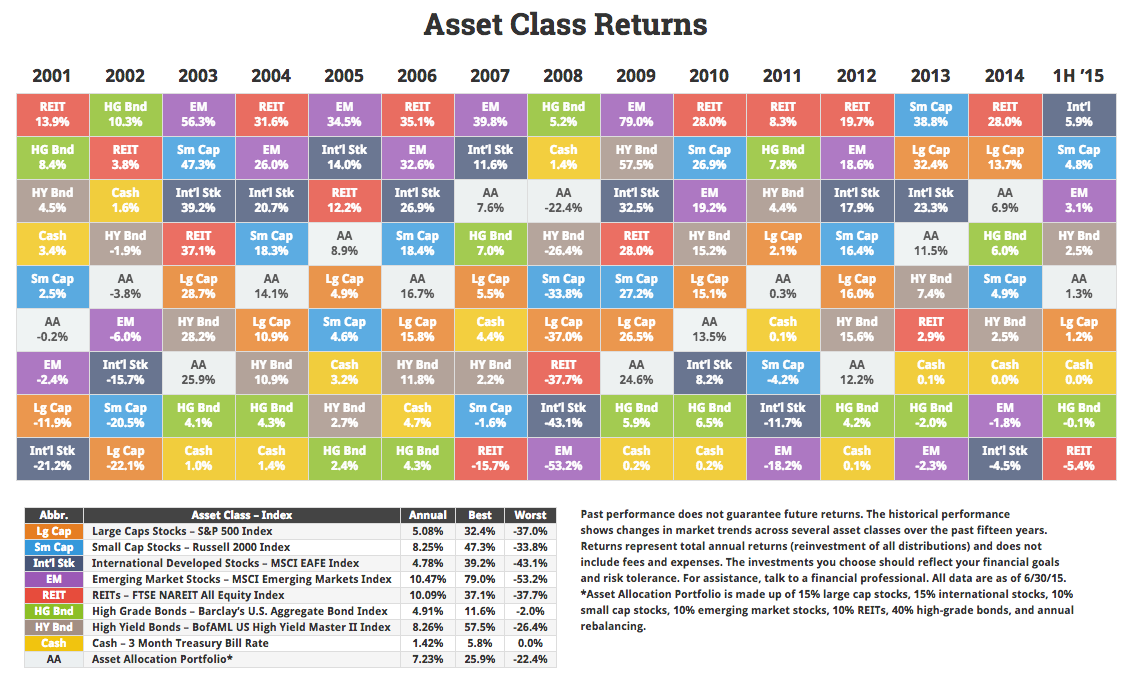

- The Uniform Prudent Investor Act stated: “Because broad diversification is fundamental to the concept of risk management, it is incorporated into the definition of prudent investing.” Fortunately, a well-diversified portfolio captures most of the potential upside available with much lower volatility. On the other hand, a well-diversified portfolio will always include some poor performers, and that’s hard for us to abide. Do it anyway.

- The idea that an investor ought to be aware and nimble enough to avoid market downturns or simply to find and move into better investments is remarkably appealing. But nobody does it successfully over time. We’ve all seen and done this: we find a hot new approach or hot new manager and, because what we own hasn’t been doing so well, we switch, only to find that the hotness that caused us to buy has cooled. We need to get off that merry-go-round.

- The leading factor in the success or failure of any investment is fees. In fact, the relationship between fees and performance is an inverse one. Every investor needs to count costs.

- Multiple studies establish what we should already know: a manager who has a significant ownership stake in his fund is much more likely to do well than one who doesn’t. Make sure to look for “skin in the game” from every money manager you use.

- Don’t be afraid to ask for and get help. American virologist David Baltimore, who won the Nobel Prize for Medicine in 1975, once told me that over the years (and especially while he was president of Caltech) he had received many manuscripts claiming to have solved some great scientific problem or overthrown the existing scientific paradigm to provide some grand theory of everything. Many prominent scientists have drawers full of similar submissions, usually from people working alone and outside the scientific community. As Dr. Baltimore emphasized, good science is a collaborative, community effort; crackpots work alone.

Happy New Year and all the best in 2016!

Source: TA