The Best Advisors Will Tell You “NO”

As a fiduciary we’re obligated to put our clients’ interests first. This essential mandate can on occasion run into direct conflict with what a client wants. There are circumstances where an advisor knows that what the client is requesting defies common sense and is at odds with his or her long-term interest.

What kind of things are we talking about? Here’s a short list courtesy Barry Ritholtz:

• Taking on more risk than is prudent.

• Buying the hot new thing.

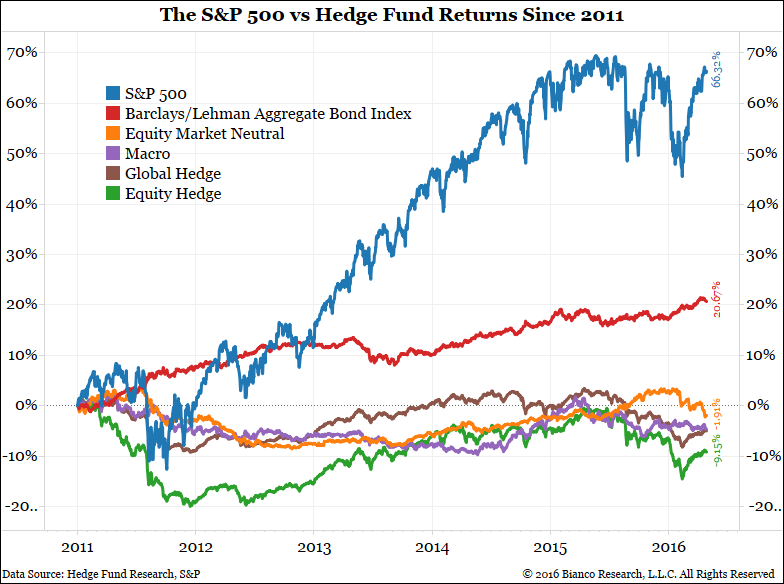

• Participating in an expensive, underperforming private investment (e.g., hedge funds, venture capital).

• Using excess leverage.

• Following the advice of pundits or talking heads.

• Overtrading.

• Pursuing the latest media fixation.

• Speculating in commodities.

• Allowing emotions to steer investments.

• Buying low-quality, high-yield “junk” fixed income paper.

• Buying non-liquid investments (private equity, gated private investments).

• Market timing.

• Buying IPOs.

• Cherry-picking portfolio allocations.

Our gently communicated but firm response to all of these is “NO.” All the academic research in the world suggests these are a bad bet. As Barry says, “if you want to make an expensive gamble, enjoy a lovely vacation to Monte Carlo, but please leave your retirement plans out of it.”

That’s our stance on this issue and we take it from a position of deep care and protection for our clients. But what’s your opinion? Should advisors do what a client wants, even when the advisor knows it is not in the client’s best interests?

P.S. In case you’re wondering…here’s what a big “YES” is in our book:

We invest through a broadly diversified set of indexes via a robust asset allocation model. It is global, inexpensive and primarily passive. It is statistically what is most likely to generate the highest returns for the least amount of risk over the long-term.