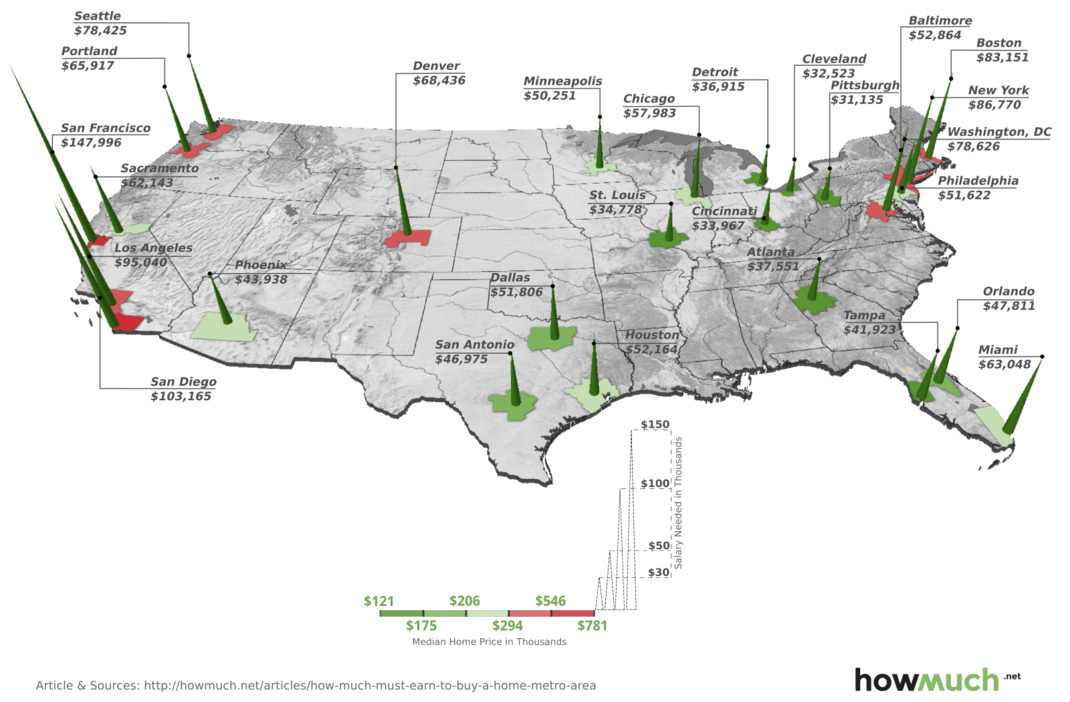

How Much You Need to Earn to Buy a Home in 27 U.S. Cities

How much salary do you need to earn in order to afford the principal, interest, taxes and insurance payments on a median-priced home in your metro area?

| Cities | 30-Year Fixed Mortgage Rate |

Median Home Price | Monthly Payment (PITI) |

Salary Needed* | ||

| National | 4.02% | $222,700 | $1,192.67 | $51,114.62 | ||

| Pittsburgh | 3.90% | $128,000 | $726.47 | $31,134.50 | ||

| Cleveland | 4.00% | $121,800 | $758.88 | $32,523.47 | ||

| Cincinnati | 4.02% | $136,600 | $792.56 | $33,967.01 | ||

| St Louis | 4.00% | $143,700 | $811.48 | $34,777.53 | ||

| Detroit | 4.07% | $148,667 | $861.34 | $36,914.56 | ||

| Atlanta | 4.03% | $169,200 | $876.19 | $37,551.08 | ||

| Tampa | 4.16% | $175,100 | $978.19 | $41,922.58 | ||

| Phoenix | 4.03% | $221,000 | $1,025.21 | $43,937.76 | ||

| San Antonio | 4.01% | $192,100 | $1,096.08 | $46,974.78 | ||

| Orlando | 4.08% | $205,000 | $1,115.59 | $47,810.81 | ||

| Minneapolis | 4.00% | $223,700 | $1,172.52 | $50,250.68 | ||

| Philadelphia | 4.00% | $213,700 | $1,204.52 | $51,622.40 | ||

| Dallas | 4.05% | $206,200 | $1,208.81 | $51,806.01 | ||

| Houston | 4.04% | $209,200 | $1,217.16 | $52,163.93 | ||

| Baltimore | 3.98% | $233,500 | $1,233.51 | $52,864.57 | ||

| Chicago | 4.04% | $209,800 | $1,352.93 | $57,982.85 | ||

| Sacramento | 4.05% | $294,100 | $1,450.01 | $62,143.45 | ||

| Miami | 4.07% | $286,000 | $1,471.12 | $63,048.07 | ||

| Portland | 4.05% | $318,800 | $1,538.07 | $65,917.47 | ||

| Denver | 4.05% | $353,500 | $1,596.85 | $68,436.22 | ||

| Seattle | 4.09% | $385,300 | $1,829.91 | $78,424.93 | ||

| Washington | 4.01% | $371,600 | $1,834.60 | $78,625.71 | ||

| Boston | 3.96% | $393,600 | $1,940.20 | $83,151.43 | ||

| New York City | 4.00% | $384,600 | $2,024.64 | $86,770.19 | ||

| Los Angeles | 4.02% | $481,900 | $2,217.60 | $95,040.20 | ||

| San Diego | 3.90% | $546,800 | $2,407.18 | $103,164.96 | ||

| San Francisco | 3.94% | $781,600 | $3,453.24 | $147,996.19 |

* Income required to cover the mortgage’s principal, interest, tax and insurance payment assuming the standard 28% “front-end” debt ratios and a 20 percent down payment subtracted from the median-home-price

Source: Visual Capitalist