Youtube & Vimeo videos

Nihil quaeque moderatius quo ut, eu vix noster fierent postulant. Est ut magna tation, nec timeam tractatos dissentiunt id, ne integre albucius eam. Animal docendi efficiantur ut eam.

Soundcloud Audio Post Format

Malorum temporibus vix ex. Ius ad iudico labores dissentiunt. In eruditi volumus nec, nibh blandit deseruisse ne nec, vocibus albucius maluisset ex usu.

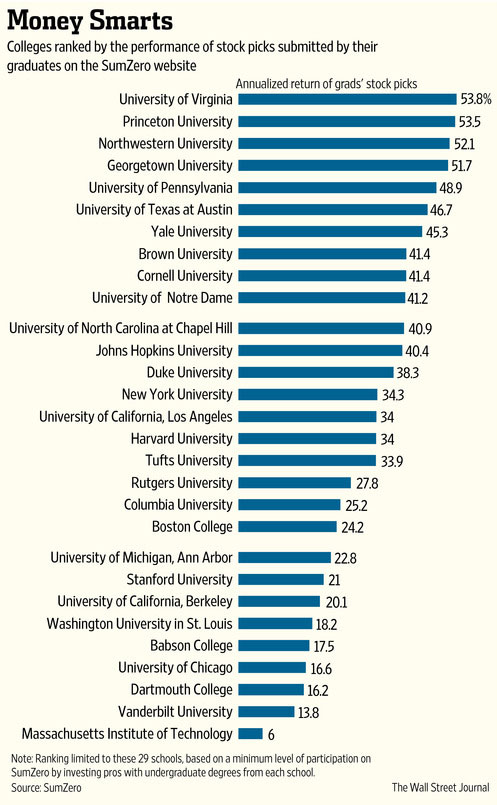

Colleges That Produce The Best Investors (?)

A new study on which schools produce the best investors has U.Va. in the top spot, according to the Wall Street Journal.

A new study on which schools produce the best investors has U.Va. in the top spot, according to the Wall Street Journal.

SumZero – “a gated online community” for investment pros analyzed their user data reaching back to 2008. The University of Virginia produces better stock pickers on average than any of the Ivy Colleges.

And just in case you’re wondering, two-third of the personnel at NorthStar Capital Advisors are U.Va. graduates!

By the way — we consider these results as pure entertainment. Stock picking is only part of the big picture. Long-term success for most investors requires careful planning, diligent saving, and disciplined execution of your investing strategy.

7 Fatal Flaws in 401(k) Plans

Paul Merriman writes about seven fatal flaws in America’s 401(k) plans:

Paul Merriman writes about seven fatal flaws in America’s 401(k) plans:

#1 Restricted Access

The first and biggest flaw in 401(k) plans is restricted access to the best investment choices

#2 Participation not required

I believe that many American households, with nothing saved for retirement, are headed by employed breadwinners who could participate in a 401(k) retirement plan

#3 Insufficient employer match

I also think employers should be required to match at least a quarter of what each employee contributes — after the waiting period, of course.

#4 Employees bear the costs

Many employers make their workers pay the costs of administering a 401(k) plan, which should be treated as an employee benefit that’s paid for by the company. In far too many cases, the costs paid by employees are hidden in the form of higher fees for investment funds.

#5 No Rollover IRA option

Federal law allows — but doesn’t require — employers to let employees move part or all of their 401(k) balances into a Rollover IRA while continuing to contribute to the company plan. All workers should have this option, which gives them access to virtually unlimited investment choices.

#6 Too much company stock

Corporate 401(K) plans often encourage participants to load up on company stock. There’s probably no way to stop this short of a federal law, because employers with publicly-traded stock love the steady market that’s created for their shares every payday.

#7 Default options are too safe

Too many plans steer contributions to low-performance investments. It’s bad enough that the employee’s default option in many plans is simply not to participate. But for those who do sign up, it’s equally wrong to have a default option of a stable value fund that virtually guarantees the employee will gradually lose some of the purchasing power of their savings.

Risks to Family Wealth

source: U.S. Trust

source: U.S. Trust

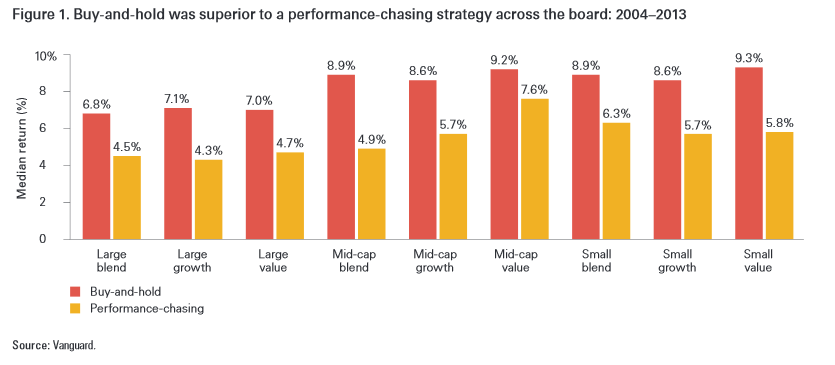

Chasing Past Performance is Expensive

A new study demonstrates that chasing the hot mutual fund is an inferior investing strategy compared to good, old-fashioned buy and hold.

A new study demonstrates that chasing the hot mutual fund is an inferior investing strategy compared to good, old-fashioned buy and hold.

Vanguard analyzed a decade of data ending December 31, 2013 across nine asset classes. In every case the investor would have been significantly better off just sticking with the index. On average the indexes generated 50% higher returns than the performance-chasing strategy!

Buy and hold may not be perfect, but it can be a lot better than flitting from mutual fund to mutual fund.

Regulators Urge Small Investors to Avoid Non-Traded REITs

REITs stands for Real Estate Investment Trusts. REITs sell like a stock on the major exchanges and invests in real estate directly, either through properties or mortgages. REITs receive special tax considerations and typically offer investors high yields, as well as a highly liquid method of investing in real estate.

REITs stands for Real Estate Investment Trusts. REITs sell like a stock on the major exchanges and invests in real estate directly, either through properties or mortgages. REITs receive special tax considerations and typically offer investors high yields, as well as a highly liquid method of investing in real estate.

Real Estate is historically a good performing asset class. Allocating approximately 10% of your stock portfolio is a generally prudent choice. However, state regulators are seeing more and more trouble with a certain type of real estate investment: non-traded REITs.

Non-Traded REITs

Unlike normal REITs, non-traded REITs do not trade on a securities exchange. They have several very significant issues:

- Non-traded be can very illiquid.

- They can be very difficult or impossible to price on a regular basis.

- It can be difficult to exit the investment.

Front-end fees can be as much as 15% (much higher than traded REITs due to the limited secondary market)

Non-traded REITs buy office buildings, stores, and other properties. They are sold directly to private investors by financial advisors and brokers.

State Securities Regulators Worried

Regulators are concerned that small investors are not fully aware nor understand the risks associated with non-trade REITs. States are on the verge of adopting new restrictions to protect “mom and pop” investors including:

- Limit how much an individual’s net worth could be put into any a single REIT

- Limit the ability of REITs to pay dividends immediately after raising new money (to avoid a Ponzi-scheme like dynamic of paying old investors with new investors’ money)

The State of Massachusetts has brought enforcement actions against brokerages for improper sales of non-traded REITs including

- LPL Financial

- Ameriprise

- Commonwealth Financial

- Lincoln Financial

Source: WSJ

Credit Card Comparison Sites are NOT unbiased

If you google “credit card comparison” you’ll get a long list of review websites. These sites purportedly provide an objective, unbiased analysis for consumers looking for a good credit card. But if you dig into the fine print, you’ll discovered that very often lenders pay to advertise on those sites! If fact, credit card providers take a heavy hand in dictating how their cards show up on these sites.

If you google “credit card comparison” you’ll get a long list of review websites. These sites purportedly provide an objective, unbiased analysis for consumers looking for a good credit card. But if you dig into the fine print, you’ll discovered that very often lenders pay to advertise on those sites! If fact, credit card providers take a heavy hand in dictating how their cards show up on these sites.

These six websites’ credit card comparison tools show only cards from lenders that pay to advertise:

- Credit.com

- CreditDonkey.com

- CreditSeasame.com

- FindTheBest.com

- Mint.com

- MyRatePlan.com

Many others show mostly advertiser cards and those credit cards receive preferential treatment.

Usually, the card-comparison sites get paid only if consumers start the card application process on the site and the lender approves them for a card.

Buyer (or credit card carrier) be ware!

Source: WSJ

Recent Posts

-

Are Financial Advisors Worth It? (DIY vs. Hiring a Pro) August 6,2026

Are Financial Advisors Worth It? (DIY vs. Hiring a Pro) August 6,2026 -

-

Four Things That Can Sabotage Retirement July 9,2026

Four Things That Can Sabotage Retirement July 9,2026 -

Is 2032 the End of Social Security? June 25,2026

Is 2032 the End of Social Security? June 25,2026 -