Rebalancing is Important

An investment portfolio must be periodically rebalanced back to its original targets to maintain the intended risk level and asset allocations (i.e., mix of stocks and bonds).

An investment portfolio must be periodically rebalanced back to its original targets to maintain the intended risk level and asset allocations (i.e., mix of stocks and bonds).

Drifting Through Time

Say you started out with a portfolio of 50% stocks and 50% bonds at age 21. Stocks go up 2 out of 3 years on average. By the time you’re 50 your portfolio mix could drift to 90% stocks and 10% bonds. That’s quite out of balance!

In rebalancing, we would sell the “excess” of stocks and use the proceeds to purchase bonds. In doing so, we ensure that we sell investments at a relatively high prices and buy investments at a low price.

Effects of Rebalancing

In a balanced portfolio of stocks and bonds, you will typically be selling stocks and buying bonds when you rebalance. You will be removing excess volatility from the outsized stock allocation and going back to your initial combination of stocks and bonds.

Quarterly or Annually — Which is better?

In a taxable account, there is a tax benefit for waiting more than a year to rebalance. In a non-taxable account, quarterly rebalancing can have some advantages. You probably don’t want to rebalance on shorter time periods because you need to give your strong-performing investments time to run and avoid the potential costs of excess transactions.

Easy Rebalancing

Is it possible to set up automatic rebalancing? One way is to work with a professional money manager like NorthStar. We do this for our clients. Big firms like Vanguard usually don’t have an automatic option, but they say they will spend 15 to 30 minutes on the phone with customers to help walk through the process and get rebalanced.

When promised quick profits, respond with a quick “no”

Warren Buffett is one of the most successful and sage investors alive today. Students of investing anxiously await his annual letter to shareholders to glean pearls of the wisdom from this master.

Warren Buffett is one of the most successful and sage investors alive today. Students of investing anxiously await his annual letter to shareholders to glean pearls of the wisdom from this master.

Here’s one of our favorite Warren Buffett quotes from the 2014 letter:

“You don’t need to be an expert in order to achieve satisfactory investment returns. But if you aren’t, you must recognize your limitations and follow a course certain to work reasonably well. Keep things simple and don’t swing for the fences. When promised quick profits, respond with a quick ‘no.’”

Unfortunately there are many people that are victimized by financial fraudsters. Just this week a Charlotte, NC man, Mitchell Brian Huffman, was ordered to a pay $2.1 million civil penalty for operating a Ponzi scheme that bilked clients out of about $3.2 million.

Huffman told his 30 victims that he was generating outrageously high annual rates of return of 100% to 150% using a proprietary trading program. Huffman used their money to fund a lavish lifestyle including classic cars and luxury vacations.

3 1/2 Weeks Until an Important Deadline

Here’s an important reminder if you have an individual retirement account (IRA) or are considering opening an IRA. 2013 contributions to IRAs can still be made up through April 15, 2014.

Make it a double? If you really want to make the most of the growth potential that retirement accounts offer, you should consider making a double contribution this year: a last-minute one for the 2013 tax year and an additional one for 2014, which you’ll claim on the tax return you file next year. That strategy can add much more to your retirement nest egg than you’d think.

2013/2014 Annual IRA Contribution Limits*

- Traditional/IRA Rollover: $5,500 ($6,500 if you are 50 years old or older)

- Roth IRA: $5,500 ($6,500 if you are 50 years old or older)

- SIMPLE IRA: $12,000 ($14,500 if you are 50 years old or older)

- SEP IRA: $51,000 (2013), $52,000 (2014)

*Note: The maximum contribution limit is affected by your taxable compensation for the year. Refer to IRS Publication 590 for full details.

The savings, tax deferral, and earnings opportunities of an IRA make good financial sense. The sooner you make your contributions, the more your money can grow.

If you have any questions or would like to make an IRA contribution give us a call at (704) 350-5028 or email info@nstarcaptical.com.

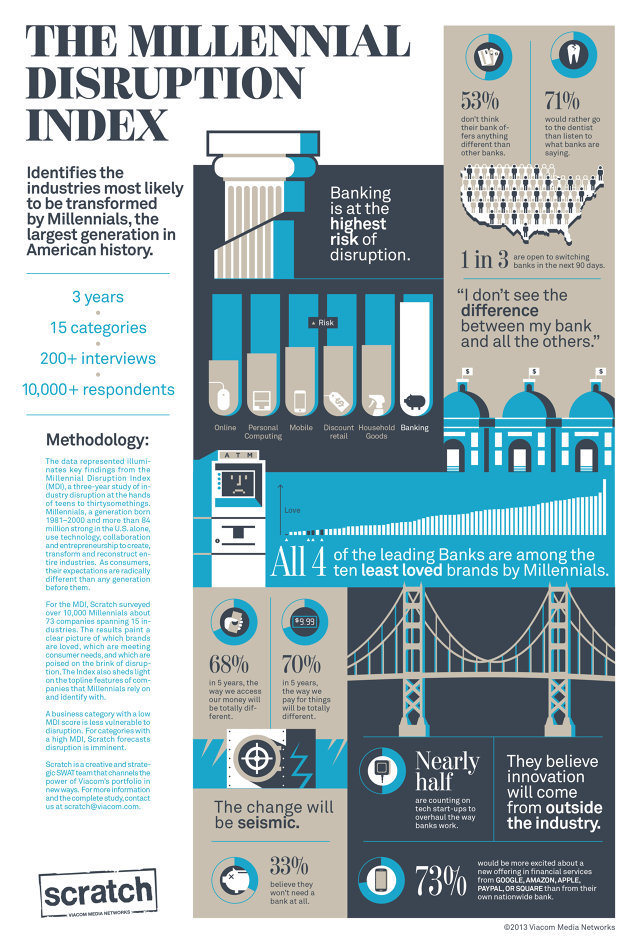

Sorry Banks, Millennials Hate You

A three-year study involving 10,000 millennials (born 1981-2000) reveals an overwhelmingly negative sentiment toward banks:

- Banking is the most prime industry for disruption in millennials’ opinion

- Banks make up four of the top 10 most hated brands for millennials

- Millennials increasingly view banking institutions as irrelevant

Source: FastCo

Source: FastCo

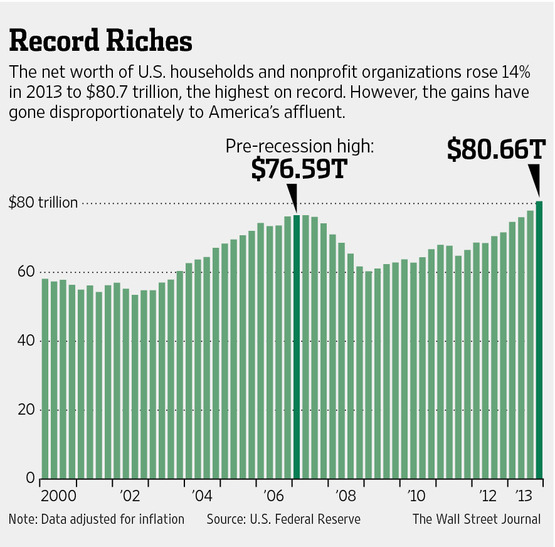

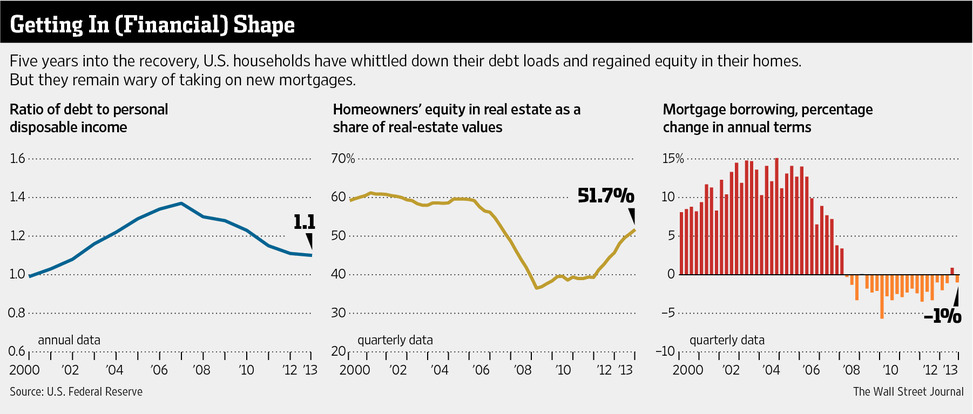

American’s Wealth at Fresh High

Americans’ wealth hit the highest level ever last year reflecting a surge in the value of stocks and homes. A record-setting rally of +30% in the U.S. stock market drove most of the past year’s gains.

Americans’ wealth hit the highest level ever last year reflecting a surge in the value of stocks and homes. A record-setting rally of +30% in the U.S. stock market drove most of the past year’s gains.

According to a Federal Reserve report released today, the net worth of U.S. households and nonprofit organizations rose 14% last year.

The Fed’s report shows that Americans have made good progress on repairing the damage caused by the housing crash and the recession (Dec 2007 – Jun 2009). Americans have been reducing their debt loads and regaining equity in their homes.

Source: Wall Street Journal

Source: Wall Street Journal

Oklahoma Schools Required To Teach High School Students to Manage Finances

Oklahoma high school students, effective this May, now must demonstrate an understanding in banking, taxes, investing, loans, insurance, identity theft and eight other areas to graduate.

Oklahoma high school students, effective this May, now must demonstrate an understanding in banking, taxes, investing, loans, insurance, identity theft and eight other areas to graduate.

The intent of personal financial literacy education is to inform students how individual choices directly influence occupational goals and future earnings potential. Successful money management is a disciplined behavior and much easier when learned earlier in life.

Real world topics covered by the Oklahoma standards include the following:

- Earning an income;

- Understanding state and federal taxes;

- Banking and financial services;

- Balancing a checkbook;

- Savings and investing;

- Planning for retirement;

- Understanding loans and borrowing money, including predatory lending and payday loans;

- Understanding interest, credit card debt, and online commerce;

- Identity fraud and theft;

- Rights and responsibilities of renting or buying a home;

- Understanding insurance;

- Understanding the financial impact and consequences of gambling;

- Bankruptcy; and

- Charitable giving

22: Your Magic Retirement Number

Most Americans need to save more to assure a financially secure retirement.

Most Americans need to save more to assure a financially secure retirement.

But many people struggle with key retirement questions like “how much do I need to save?”

You should save 22 times the annual income you want to have in retirement.

For example, if you want $100,000 in annual income (not including Social Security), then you need to have $2.2 million in total retirement savings.

(22 x $100,000 = $2.2 million)

See this recent article in the Wall Street Journal on how researchers arrived at this magic number of 22.

IBM and AOL Are Messing with Your 401(k)

401(k) accounts are an important part of many people’s retirement savings. And the employer match is a critical part of that system. So when big companies like IBM and AOL start monkeying with that match, you should pay attention because other companies may follow suit!

401(k) accounts are an important part of many people’s retirement savings. And the employer match is a critical part of that system. So when big companies like IBM and AOL start monkeying with that match, you should pay attention because other companies may follow suit!

IBM changed its 401(k) system in 2012 to hand out employee matches in one lump sum at the end of the year leading to an uproar. IBM employees are now missing out on compounding throughout the year that they used to get from contributions peppered in throughout the year. In addition, if you leave IBM before December 15th and you’re not retiring, you lose the match entirely.

Experts warned that others would try to follow IBM’s example by watering down their 401(k) programs as well. Sure enough, AOL took things even further!

AOL said starting in 2014, an employee must be active on December 31st to receive the company match. Furthermore, the contribution will a “one time lump sum after the end of the Plan Year.” So you have to stay with the company through the end of year and you don’t even get the match during 2014!

The protest following AOL’s announcement was so intense, AOL chief Tim Armstrong reversed the changes to the 401(k) policy after just one week of bad publicity.

11 Questions To Ask When Hiring A Tax Preparer

The IRS started accepting tax returns January 31st so it’s a good time to start thinking about your own taxes. Kelly Phillips Erb recently wrote an article that provides an excellent check list of questions to ask your tax preparer when filing your taxes before handing over your w-2’s or 1099’s:

The IRS started accepting tax returns January 31st so it’s a good time to start thinking about your own taxes. Kelly Phillips Erb recently wrote an article that provides an excellent check list of questions to ask your tax preparer when filing your taxes before handing over your w-2’s or 1099’s:

- Do you have a PTIN? (This is a Tax Preparer Identification Number)

- What is your tax background? (CFP®, CPA, EA, JD, VITA) Tax preparers that are being compensated for their time should carry one of the these professional designations or certifications: CERTIFIED FINANCIAL PLANNER™, Certified Public Accountant, Enrolled Agent, Juris Doctor, Voluntary Income Tax Assistance.

- Have you prepared a tax return before?

- Do you know the requirements for filing returns in my area? (Filing taxes for income earned in multiple state or states other than the one you are currently residing in)

- What records or documentation will you need from me? It is a good idea to bring the previous year’s tax returns as well as all income documentation, and proof of any expenses that you think could be deductible.

- How do you determine your fee? (By the hour or per line item on the return, etc.)

- Can I file electronically? (Pretty much a given – just about all returns are e-filed now)

- Who will sign my return? Remember the first question. Do not trust a preparer that will not sign your return or cannot tell you who will be signing your return.

- Will I receive a copy of my return? (This sounds like a given but sometimes preparers do not provide a copy of the return without a request)

- How do I find you if there is a problem with my return after the tax season is over? (Especially important if the preparers is only in business during tax season)

- What happens if I get audited?

Be sure to check out Erb’s article for the “right” and “wrong” responses to these key questions.

Source: Forbes

Recent Posts

-

Real Estate Investing — Love It or Leave It? April 2,2026

Real Estate Investing — Love It or Leave It? April 2,2026 -

5 Conversations Every Couple Needs Before Retirement March 19,2026

5 Conversations Every Couple Needs Before Retirement March 19,2026 -

Timing Social Security and Taming Scary Markets March 5,2026

Timing Social Security and Taming Scary Markets March 5,2026 -

Don’t Make These Mistakes on Your Tax Return February 19,2026

Don’t Make These Mistakes on Your Tax Return February 19,2026 -