Today marks a most significant anniversary in the economic and financial history of the United States, and I could not let it pass without comment. When properly appreciated, it can serve as an importantly teachable moment.

For it was a quarter century ago, on the night of Thursday, December 5, 1996, that the iconic Federal Reserve chairman Alan Greenspan, speaking at a dinner of the American Enterprise Institute in Washington, gave his instantly legendary “irrational exuberance” speech.

And this is what the oracle said. Or more accurately, this is what he asked:

“How do we know when irrational exuberance has unduly escalated asset values, which then become subject to unexpected and prolonged contractions as they have in Japan over the past decade? And how do we factor that assessment into monetary policy?” [43:38 in the video above]

Mr. Greenspan asked these twin rhetorical questions essentially because he did not have conclusive answers. And if he didn’t, you knew no one else in the world did either. But coming from him, even this interrogative form of thinking out loud was a financial thunderbolt — a shot heard round the world.

He surely understood that, when he so much as broached the question, he had at least suggested an answer. And that answer was unmistakably: we’re either already there, or will be mighty soon, as this greatest of all bull markets morphs into mania.

I thought it might be instructive — as well as a certain amount of good fun — to cast an eye over the intervening quarter century. Let’s begin with a key item of baseline data that may and certainly should inform our inquiry.

Fact: The Standard & Poor’s 500 Stock Index had closed that Thursday afternoon, in blissful ignorance of what was coming later in the evening, at 744.38. And sure enough — just as the oracle had darkly suggested it must — the S&P 500 topped out…three years, three months and 19 days later, on March 24, 2000, at 1,527.50. You read that right: it more than doubled in the 40 months after Greenspan’s dire warning.

I suppose I could just stop here, invite you to draw the obvious inference from the above, and call it a day. Said inference is, of course: No one — no central banker, no economist, no market strategist, no hedge fund manager — no one can predict the market, much less tell you where to get out and/or back in. The economy cannot be consistently forecast, nor the market consistently timed. By anyone.

But before I let you go, I’d just like to throw out a very few other potentially relevant factoids.

Friday afternoon, December 3, the S&P 500 closed at 4,538.43, up more than six times since Greenspan spoke.

With dividends reinvested, and any taxes paid from some other source, $10,000 invested in the S&P 500 on 12/4/96 is getting pretty close to $100,000 along about now.

The earnings of the S&P 500 for the year 1996 were $40.63. With less than a month to go in the current year, the consensus forecast is around $200, up almost exactly five times.

The S&P 500’s cash dividend in 1996 was $14.90. Consensus forecast for this year is about $60, up almost exactly four times.

The Consumer Price Index was 158.6 in December 1996. It will most likely close out this year around 280, up a mere 1.8 times.

What, then, was the single best financial decision you could have made on Thursday night, December 5, 1996 — when the 11 o’clock news breathlessly reported Greenspan’s electrifying remarks? Right: turn off the TV and go to bed.

Just my opinion, of course, but the best move you can make this morning, 25 years on, regardless of the headlines? The same: turn off the TV, log out of your computer. Enjoy the rest of your day.

And let the compounding proceed, uninterrupted.

With every good wish,

Dr. Chris Mullis

Sources:

Historical S&P 500 Index and dividends: “S&P 500 Earnings History, NYU Stern School”

Consensus 2021 earnings forecast: Yardeni Research

Consensus 2021 dividend forecast: Bloomberg

Consumer Price Index: Inflationdata.com

Current net profit margin of the S&P 500: FactSet

Let’s face it. Buying meaningful gifts for our family and friends is really, really hard.

If you want to give something that has a larger impact long after the holiday season has passed, why not give the gift of financial knowledge and wisdom for living a fulfilled life?

Given the academic background of our firm, we know the following is going to be a big shocker:We really love reading books and giving books as gifts!

Below you’ll find our 2021 Guide to Gifts That Pay Off.

It’s full of our 23 favorite money-related and living-big gift recommendations for those ages 4 to 94!

Let us highlight a couple of our new recommendations this year:

The Total Money Makeover (Dave Ramsey) A proven plan for financial fitness

We love giving this book out to our clients for their adult children. And we like to give these out as graduation and wedding gifts with a $100 bill tucked inside. About 80% of this book is really good, but we (and history) may not agree with perhaps the other 20% (e.g., unrealistic investment return assumptions; over-reliance on growth investments; unsustainably high withdrawal rates in retirement). Nonetheless, Mr. Ramsey does a great job of teaching the basics of money.

The Price You Pay for College (Ron Lieber) An entirely new road map for the biggest financial decision your family will ever make

One of our savvy clients in Washington, D.C. brought this 2021 book to our attention and it’s excellent! This book discusses why college costs so much, digs into the allure of elite schools, uncovers hacks that may not really be hacks, and talks about how to plan and pay for college.

Knocking on Heaven’s Door (Katy Butler) The path to a better way of death

While it can be very difficult, having tough conversations about end-of-life care well in advance can help our dying loved ones cope later on. We have the ability to cultivate a “good death.” Give this book to your parents if they are still living and discuss it with them. And depending on your age, give it to your spouse and discuss it with them.

Retirement Heaven or Hell (Michael Drak et al.) 9 principles for designing your ideal post-career lifestyle

Don’t be fooled, the transition to retirement is a very difficult transition for many. To retire well you need enough purpose to wake up in the morning and enough money to sleep at night. Taking the time to read this book, reflect, explore, and be intentional will mean the difference between ending up in “retirement heaven” and “retirement hell.”

So what is the ultimate gift of 2021?

Life-changing wisdom about managing your money and living your best life that you can give to those that you truly care about!

Are you taking stock of your life and thinking about moving on? (You’re not alone.)

Are you a boss struggling to fill roles and retain your people? (You’re in good company.)

America is going through a pretty major reconfiguration of the labor market.

Headlines are calling it the “Great Resignation” but I think it’s deeper than that.

The pandemic threw many assumptions out of the window. It caused us to think long and hard about a lot of things.

Where we work. How we work. What work means. What we want out of life.

That existential crisis is visible on the supply side of the labor market:

Folks retiring ahead of schedule (not all by choice).1

Folks quitting their jobs.2

Folks (primarily women) caring for kids and family instead of going back to work.3

Folks striking over pay and working conditions.4

Folks starting new businesses.5

And it’s visible on the demand side as well:

Restaurants struggling to staff up.6

Shipping ports clogging up because there aren’t enough truckers to haul goods away.7

Employers offering higher wages and perks to attract job seekers.8

At its most basic level, employment is a transaction: a certain amount of work for a certain amount of pay.

But it’s really much more than that.

For many of us, who we are as a worker…

A business owner…

A boss…

Is central to our identity.

And the ground is shifting under our feet. That makes folks anxious.

High-anxiety times like these bring plenty of judgment, blame, and dramatic headlines.

Are workers who don’t want to take low-paying, high burnout jobs lazy?

Of course not.

Are business owners worried about keeping their doors open evil capitalists?

Nope.

Are employees organizing strikes or leaving for better opportunities disloyal?

No way.

We’re all doing the best we can every day.

When we see talking heads griping about “entitled” workers or “greedy” businesses, let’s remember that behind the numbers are real people with real struggles.

A parent with a medically fragile kid who is afraid to go back to work.

A business owner who worries the staffing shortage will put her out of business.

A laid-off worker who doesn’t have the skills needed to get a different job.

A manager who is doing two jobs because he can’t fill a key role.

Let’s be compassionate toward one another.

What does the labor market upheaval mean for the economy?

That’s hard to say.

It could cause a slowdown in some sectors if businesses struggle to fulfill demand.

It could lead to increased inflation if higher wages get passed on as higher prices.

It could be a factor in a market correction.

It could also accelerate trends toward automation, remote work, and offshoring.

Bottom line: Like most major events in history, the overall consequences won’t be fully visible for a long time.

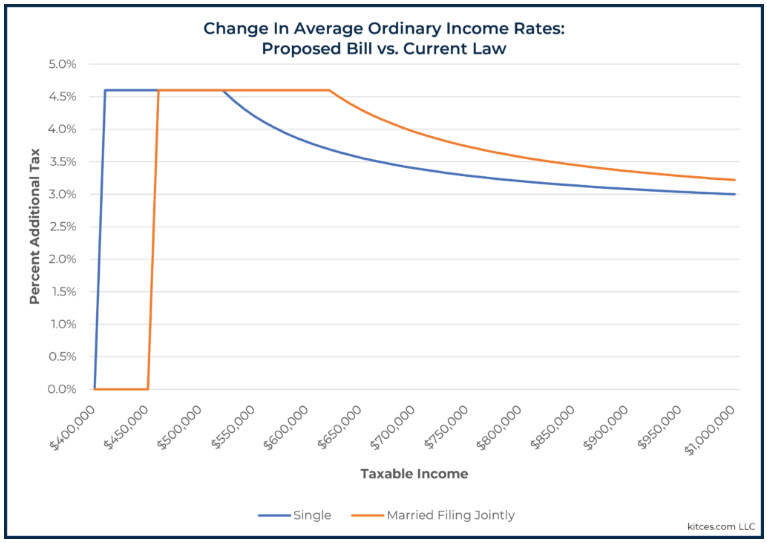

By now, you’ve likely seen that the House Ways and Means Committee released a draft of major tax legislation last week.

What’s ahead?

Significant changes to U.S. tax policy for 2022 seem likely, including around income tax rates, rules regarding retirement accounts, estate and transfer laws and much more.

Many of the features of Biden’s original plan are included in the House plan, most significantly the raising of income and capital gains tax rates on high earners.

The changes that have been made suggest that a lot of negotiations have already taken place among Democrats so, if the legislation becomes law, its final form will likely be similar to the House plan.

How will this impact you?

We’ve already parsed through the draft and have started building some of the proposed changes into our tax planning tools so that we will be able to illustrate, on a “what if” basis, the potential impacts to our clients compared to the current tax law.

While we do that, we wanted to provide you with a quick summary of some of the key points of the proposed legislation (as best as we can glean at the present time):

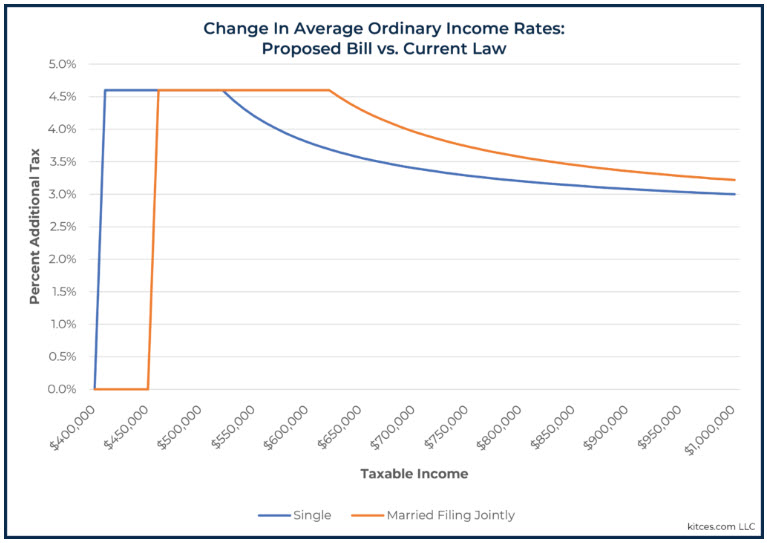

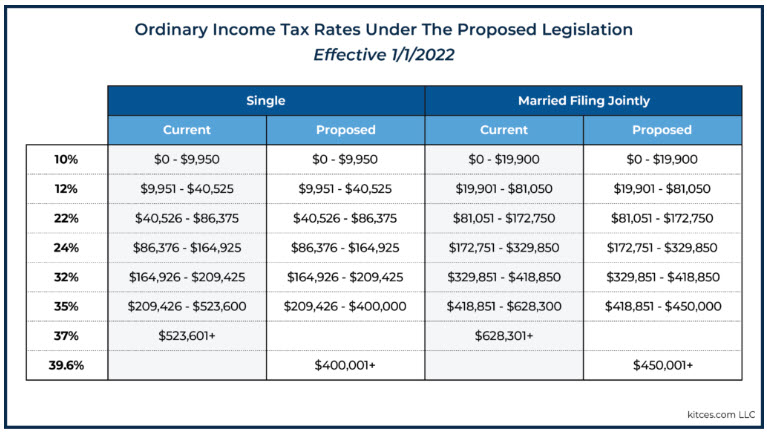

Single filers with income below $400,000 and Married Filing Joint filers with income below $450,000 will probably not see significant impact right away.

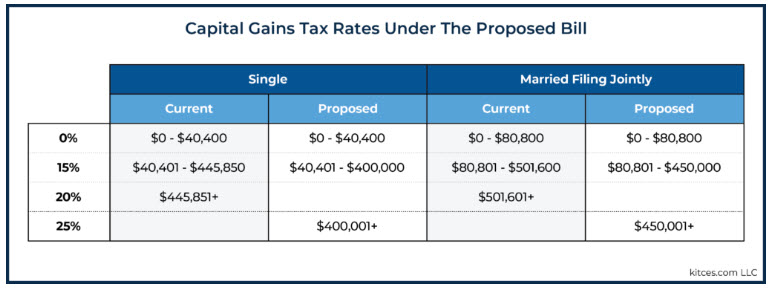

Taxpayers with income over those thresholds should expect higher marginal rates and higher capital gains rates.

The bill brings back the 39.6% marginal bracket on ordinary income while compressing the existing 32% and 35% brackets.

For folks over the $400K/$450K thresholds, capital gains increase from 20% to 25%. While unpleasant, recall that President Biden’s original proposal included a top capital gains rate of 39.6%.

The strategy of making non-deductible IRA contributions and then converting them to a Roth IRA – or the “backdoor Roth” – looks like it’s on its way out starting in 2022. The same goes for the “mega backdoor Roth” strategy inside of 401k plans.

Increases to both the Child Tax Credit and the Child and Dependent Care Credits.

Elimination of Roth conversions for folks over the income thresholds…but not until 2031!

The gift and estate tax exemption amounts would effectively be cut in half starting in 2022. That would still be over $5 million/person, though.

Application of the 3.8% Net Investment Income Tax (NIIT) to S-corp distributions for taxpayers with income higher than $400,000 (individual) or $500,000 (married filing jointly).

Limitations of the QBI Deduction (199A deduction) for high income taxpayers

One additional item worth keeping track of is a 3% surcharge on very, very high-income people. But that’s also going to apply to trusts with income of over $100,000. For clients who have left IRAs to a trust for the benefit of minor children, this income threshold may come faster than you think given the 10-year requirement to deplete an inherited IRA.

REMEMBER: Tip your server, not the IRS

The legislation will now be debated in Congress and finalized in the weeks to come.

We continue to monitor developments and strategize around this plan to give you the best possible outcomes when this new tax reality arrives.

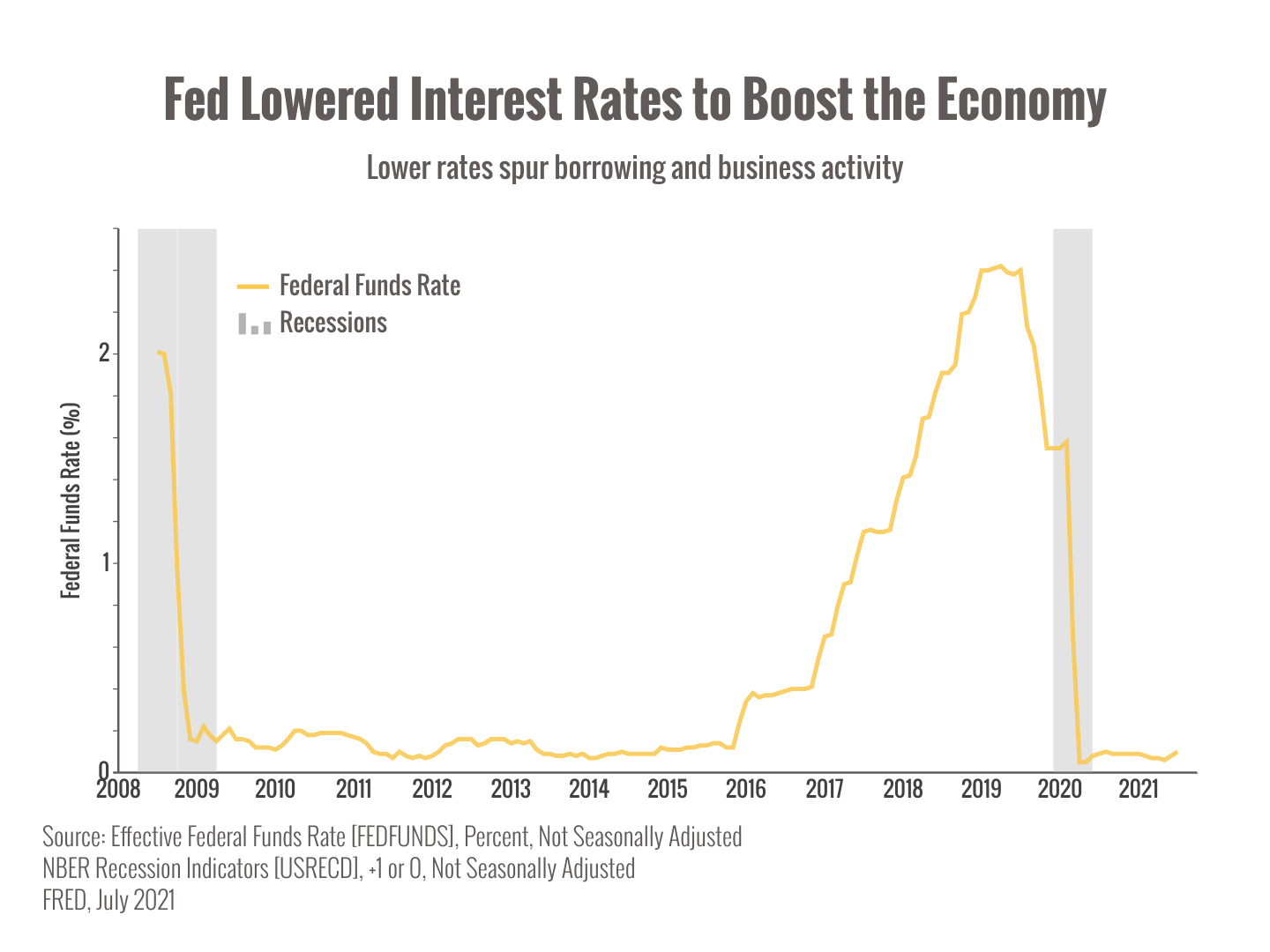

One big thing you may have heard about in the headlines is the Federal Reserve’s hint that it might start “tapering” soon.1

Could the Fed’s actions cause a market correction or economic slowdown?

Let’s discuss.

First of all, what does ”tapering” mean?

In econ-speak, tapering means winding down the pace of the assets Fed has been buying since last summer.

Why is it a big deal?

Well, the last time the Fed tapered in 2013, during the recovery from the 2008 financial crisis, markets panicked and pitched a “taper tantrum.”2

That’s because traders worried that less Fed support would hurt fundamentals and potentially cause a market downturn.

Now, that old taper tantrum narrative is making folks worry that another market downturn could be ahead of us, especially with concerns about the Delta variant.

Before we dive into what could happen, let’s talk about where we are and how we got here.

When the pandemic started, the Fed slashed interest rates and began buying $120 billion a month in bonds and mortgage-backed securities to reduce interest rates, lower borrowing costs, and give businesses and the economy a boost.1

However, now that the economy is much stronger, the employment situation has improved, and inflation is a concern, the Fed wants to start paring back those asset purchases to return interest rates to a more “natural” level.

What could that look like?

Obviously, we don’t know exactly when or how the Fed will decide to act, but analysts have some pretty good guesses.

The latest prediction by Bank of America suggests tapering could start this November as the Fed gradually pares back asset purchases through next year.1

The takeaway is that the Fed isn’t going to stop buying assets and raise interest rates immediately.

It’s going to gradually remove the support and see how the economy reacts.

So, will we see another taper pullback?

The main reason folks worry about the Fed reducing support is because of the effect higher interest rates could have on stocks, particularly companies that rely on borrowed money.

However, interest rates are just one piece of the puzzle. Economic fundamentals, earnings, and other factors also weigh on stock prices.

With the benefit of hindsight, we can see that the 2013 taper tantrum wasn’t even that bad. The S&P 500 tumbled 5.8% over the course of a month, but quickly recovered (the caveat here is always this: the past does not predict the future).2

(Sidebar — keep in mind the 2013 taper tantrum decline of 5.8% was less than half of the the average intra-year decline of 13.8% annually that we typically see in the stock market. I.e., yet another piece of “noise”…a semi-random, temporary decline overlaid on the market’s permanent, long-term advance.)

We think the main reason markets declined in 2013 was that investors hadn’t experienced tapering before; they didn’t have context for what the Fed would do.

Since we’ve seen this happen before fairly recently, we think that uncertainty is lessened.

However, we also have other worries to consider: a deteriorating crisis in Afghanistan, continued pandemic worries, and political wrangling over infrastructure.

Any of these factors could derail the bull market.

But it’s not going to be the end of the world.

Pullbacks, corrections, and bear markets are always something we should expect. They happen regularly and are a natural part of markets.

Bearmarkets are common — they occur about 1 in 5 years and there have been 16 since World War II. With the average retirement lasting 30 years, you should expect to encounter 6 bears during this encore of your life.

So, the Fed is one more thing we’re keeping an eye on, and we’ll reach out if there’s more you should know.

Headlines are looking grim again, so let’s pause and take stock.

Why are the headlines terrible?

Because the media loves drama. This is not news to you or us or anyone who pays attention. The 24-hour news cycle is there to whip up emotions and keep us glued to the latest “BREAKING NEWS.”

So, what’s behind the noise and should we worry?

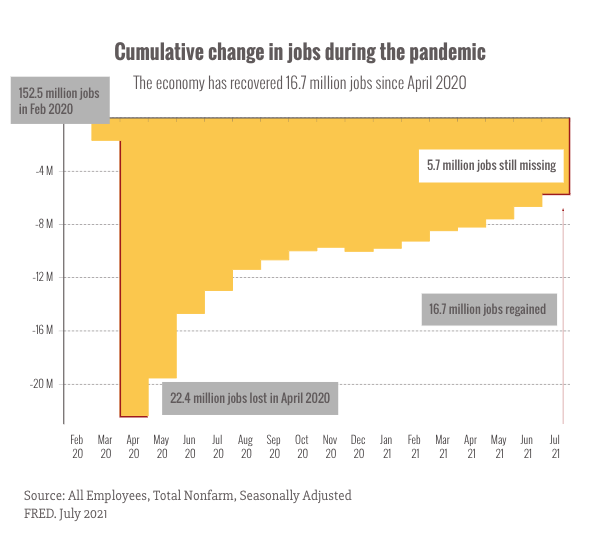

Before we jump into unpacking the news, let’s take a moment and remind ourselves of how far we’ve come since the pandemic began.

You can see it right here in this chart:

We’ve recovered the vast majority of jobs lost since the bottom of the pandemic’s disruption last April. The economy is still missing several million jobs to regain pre-pandemic levels, but we’ve made up a lot of ground, and jobs growth is still strong.1

In fact, there are more job openings right now than job seekers to fill them.2

But there’s an important caveat to the chart above.

The monthly jobs report is what economists call a “lagging” indicator, meaning that it’s telling us where the economy was, not where it’s going.

To figure out what might lie ahead, economists turn to “leading” economic indicators that help forecast future trends.

So, what are the leading indicators telling us about the economy?

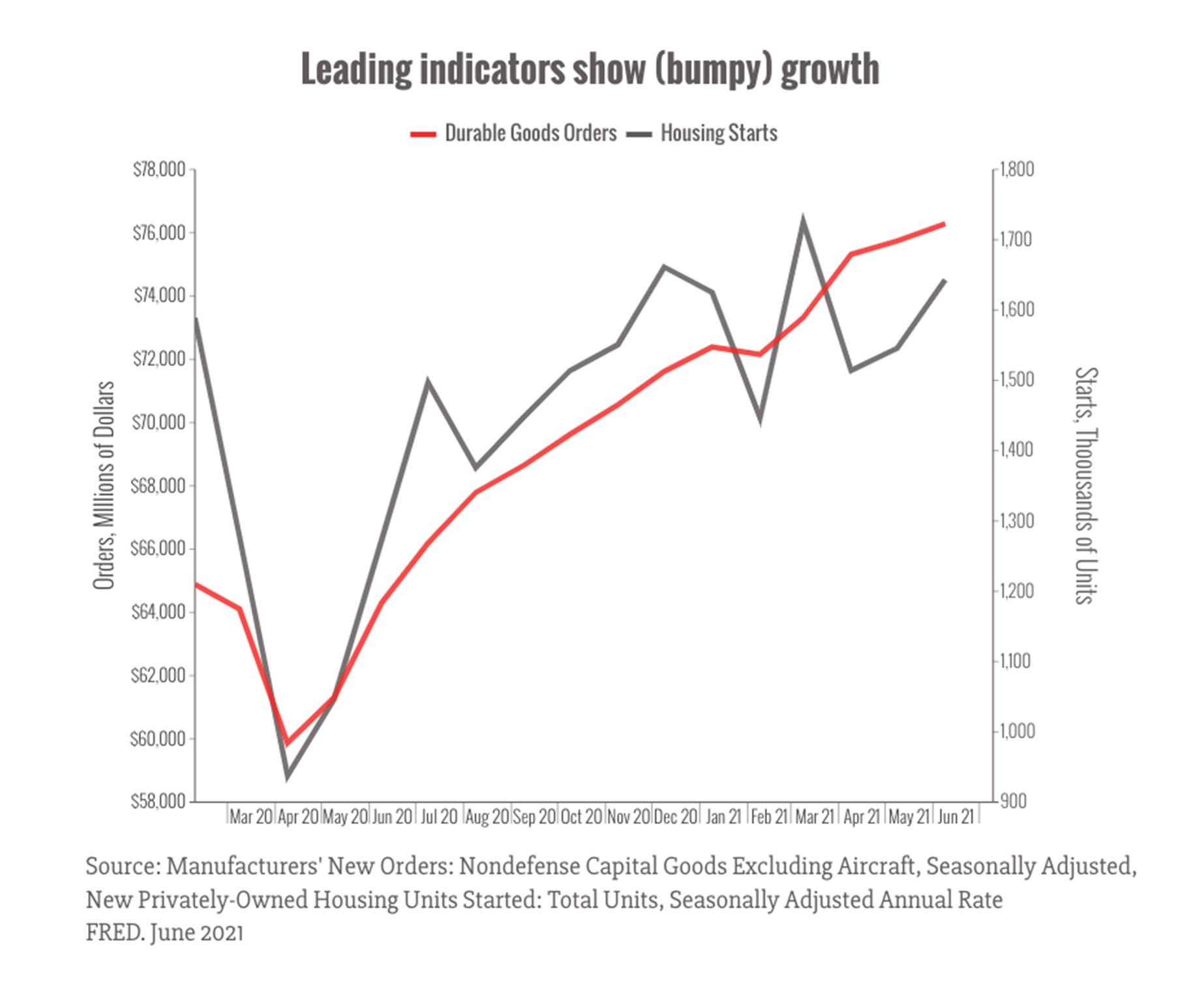

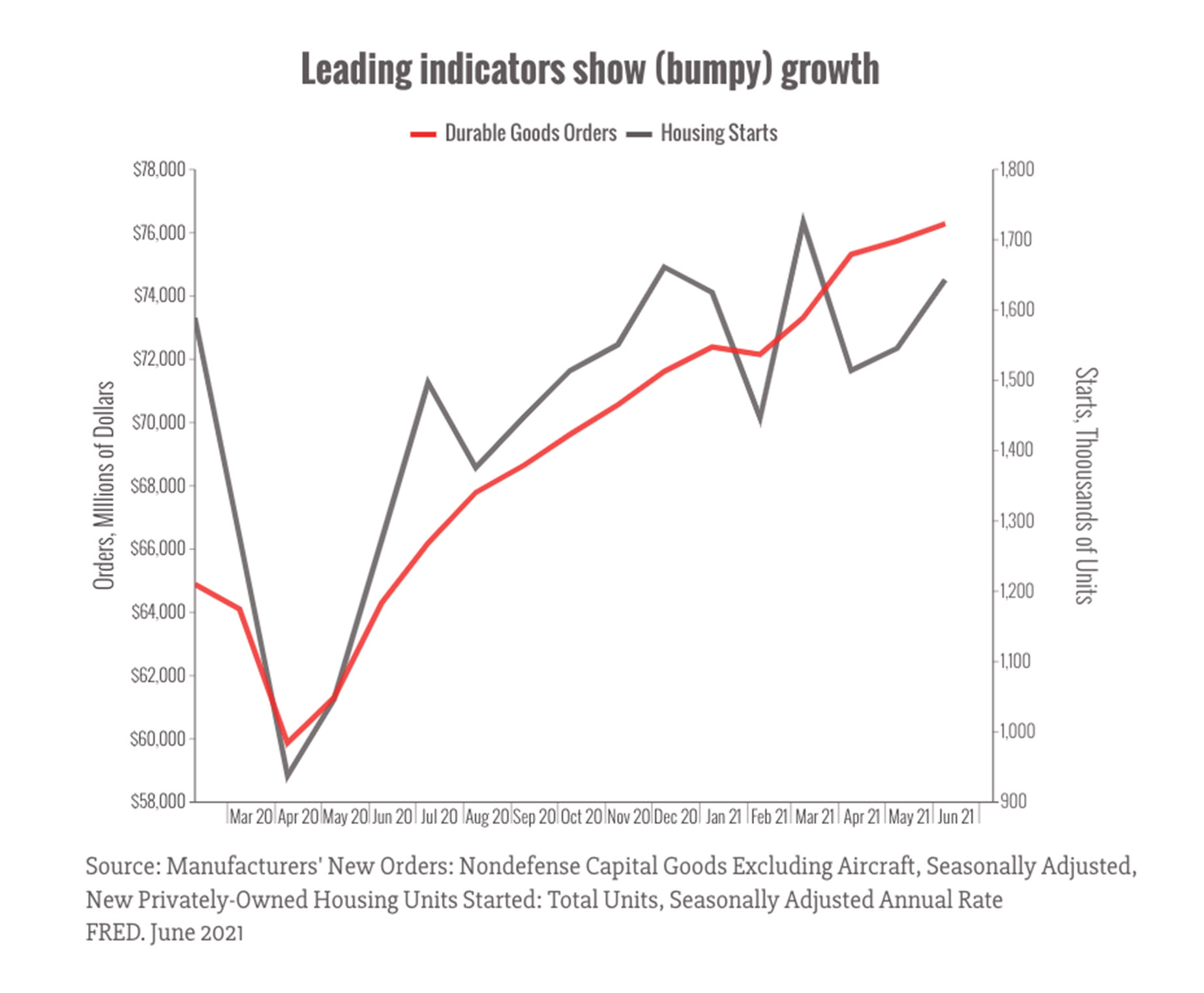

A couple of the most popular indicators are manufacturing orders for long-lasting (durable) goods, since companies don’t like to order expensive equipment unless they expect to need soon.

Another one is groundbreaking (starts) on new houses, which indicate how much demand builders expect for housing.

Let’s take a look:

Both indicators suggest continued (if bumpy) growth. Now, those are just two sectors, and we want to be thorough, so let’s take a look at a composite.

The Conference Board Leading Economic Index (LEI) gives us a quick overview each month of several indicators.

It increased by 0.7% in June, following a 1.2% increase in May, and a 1.3% increase in April, showing broad, but slowing growth.3

What does that tell us? That the economy still has legs.

Will the Delta variant derail the recovery?

New numbers came out this morning showing that retail sales fell slightly (1.1%) in July from the month before, with spending down broadly across categories as concerns about the Delta variant grew.

But most economists, while acknowledging the threat posed by the current rise in Covid cases, aren’t expecting a significant slowdown in consumer spending.

Though a serious slowdown due to the Delta variant seems unlikely, we could potentially see a bumpy fall, especially in vulnerable industries and areas with surging case counts.

There’s also some potentially good news about the Delta variant that we can take from other countries.

India and Great Britain both experienced Delta-driven surges earlier this summer.4

And what happened?

A steep and scary rise in case counts and hospitalizations…followed by a rapid decline.

It seems that these fast-moving Delta waves might burn themselves out.

Unfortunately, these surges come with a painful human cost to patients, overburdened medical staff, communities, and families.

But, if this pattern holds true in the U.S., it doesn’t appear that the economic impact will be heavy enough to derail the recovery.

All this to say, it’s clear that the pandemic is still not over.

But we’ve come such a long way since the darkest days of 2020 and the road ahead still seems bright (if a little potholed).

Please remember to take panicky headlines with a shaker or two of salt.

We’re here and we’re keeping watch for you.

Have questions? Please reach out.

P.S. The bipartisan infrastructure deal is still making its way through Congress, and we don’t yet know what the final details will look like. The Democrat-led infrastructure deal is also in the works, but we’re not likely to see serious movement until the fall. We’ll keep updating you as we know more.

Life is finally moving toward “normal” in Charlotte and across America. We’ve been in short-term mode so much… How do we build the long-term mindset we need to pursue long-term success?

In this video, we talk about some simple strategies you can use to switch from a short-term mindset to a long-term one. Click to watch!

Hi, I’m Dr. Chris Mullis with NorthStar Capital Advisors, and I’m here to help you balance your long-term goals against your short-term reality.

As we start to emerge from the COVID-19 pandemic, and life shifts back toward “normal” for many, I have a lot of people telling me that they’re struggling with thinking about long-term planning.

And that makes sense, since we’ve seen how quickly our long-term plans and goals can be turned upside down, and we’ve spent the past year or so dealing with a lot of short-term changes.

So how do we bring the long run into focus without getting derailed by the short run?

One way is by thinking of the long term as a series of short-term challenges, rather than one uninterrupted straight line.

Here are three simple strategies that you can use to train your mind:

Strategy #1 — Create a “future-you” mindset.

Who is future you? What do they want? How can you help them get there?

Embracing your future self as someone who needs you will help you create a better future with smart choices now.

Sound a little woo woo? It’s actually based on the concept of “future-orientation,” or embracing the idea that not only is the future unwritten, but that you can write it — especially for yourself.

And this idea can have real benefits. Studies have shown that future-orientation is a strong predictor for achievement, health, and happiness in life.

Strategy #2 — Prioritize flexibility over certainty.

As humans, we’re wired to look for certainty.

It feels good to think we have everything figured out.

Our instincts tell us to act quickly in the short-term to avoid the discomfort we feel with uncertainty.

But in a complex world with complex problems, acting quickly isn’t always the best move.

We often get better results in the long term by keeping a flexible mindset and experimenting with different solutions.

Strategy #3 — Recognize how emotions affect our decision-making.

We’ve all had times when we’ve acted in the heat of the moment.

Something makes us unusually happy or upset in the short-term, and we make a snap decision that has long-term consequences.

One way this plays out in investing is loss aversion, a cognitive bias that causes us to focus so hard on avoiding losses that we often miss out on the big picture, long-term benefits of our investment strategy.

The reason you pay a professional to look after your financial life is so you can share your worries and have someone help you take action — both in the short term and the long term — so that ultimately you get to do the things you love most in life.

Which of these approaches — “future-you” mindset, prioritizing flexibility, and recognizing emotions — which of these would make a positive impact on your success?

Send me a message and let me know! I read and respond to all emails.

As America continued to recover from the COVID-19 pandemic in the first half of 2021, the economy and the equity markets made significant progress. My midyear report to you is, as always, divided into two parts. First is a brief recap of our enduring investment philosophy; second is my perspective on the current situation. As always, I welcome your questions and your comments.

General Principles

You and I are long-term, goal-focused, planning-driven equity investors. We’ve found that the best course for us is to formulate a financial plan — and to build portfolios — based not on a view of the economy or the markets, but on our most important lifetime financial goals.

Since 1960, the Standard & Poor’s 500 Stock Index has appreciated approximately 70 times; the cash dividend of the Index has gone up about 30 times. Over the same period, the Consumer Price Index has increased by a factor of nine. At least historically, then, mainstream equities have functioned as an extremely efficient hedge against long-term inflation and a generator of real wealth over time. We believe this is more likely than not to continue in the long run, hence our investment policy of owning successful companies rather than lending to them.

We believe that acting continuously on a rational plan — as distinctly opposed to reacting to current events — offers us the best chance for long-term investment success. Simply stated: unless our goals change, we see little reason to alter our financial plan. And if our portfolio is well-suited to that plan, we don’t often make significant changes to that, either.

We do not believe the economy can be consistently forecast, nor the markets consistently timed. We’re therefore convinced that the most reliable way to capture the long-term return of equities is to ride out their frequent but ultimately temporary declines.

The performance of our equity portfolios relative to their benchmark is irrelevant to investment success as we define it. (It is also a variable over which we ultimately have no control.) The only benchmark we care about is the one that indicates whether you are on track to achieve your financial goals.

Current Observations

The American economy continued its dramatic recovery in the first half of 2021, spurred by (a) the proliferation of effective vaccines against COVID-19 and the retreat of the pandemic, (b) massive monetary and fiscal accommodation, and (c) its own deep fundamental resilience, which ought never to be underestimated.

The S&P 500 ended the first half at 4,297, an increase of 14.4% from its close at the end of 2020. Coming into the year, the consensus earnings estimate for the Index in 2021 was around $165; as I write, the consensus for the next 12 months has reached $200, and is still being raised.

The economy continues to struggle with supply chain imbalances, as well as with a historic mismatch between the number of job openings available and continued high (though rapidly declining) unemployment. The chattering class of pundits and financial journalists continues to speculate on when these blockages will clear; to long-term investors like us, the key is our belief that they will, in the fullness of time.

We are still in the midst of an unprecedented experiment in both fiscal and monetary policy; the outcome remains impossible to forecast. The possibility that we’ve overstimulated the economy was highlighted this spring by a significant resurgence in inflation. But as the first half ended, statements by Fed Chair Powell and Governor Bullard indicated a keen awareness of this risk, and a readiness to act against it. The markets evidently took these gentlemen at their word, as inflation hedges like gold and oil sold off, the equity market pulled back modestly, and the yield on the bellwether 10-year U.S. Treasury note retreated to the area of 1.5%. One does not want to read too much into short-term phenomena like these; suffice to say that the Fed appears acutely cognizant that its credibility is almost existentially on the line here.

There is also the issue of the Biden administration’s fairly radical tax proposals with respect to capital gains and estates. The best that can be said on this subject is that, as the first half ended, the momentum behind these initiatives seemed to be ebbing. But the political climate remains as inimical to capital (and capitalists) as it’s been in quite a while.

Nonetheless, for investors like us, I think the most important economic report of this whole six-month period came just a few days ago. It was that household net worth in this country spiked 3.8% in the first quarter of 2021 — to $136.9 trillion — propelled by broad gains in the equity market and in home prices. Even more important, perhaps, is the fact that the ratio of household debt to assets continued to fall, and is now back down to about where it was 50 years ago.

The consumer powers this economy, and the consumer has rarely carried more manageable debt levels relative to disposable income — and has simply never been holding more cash — than he/she does today. In June, the National Retail Foundation raised its outlook yet again; it now expects retail sales to grow 10.5% to 13.5% (that is, $4.44 trillion to $4.56 trillion) year over year. Just this past month, the retail giant Target raised its dividend by a whopping 32%.

On February 19, 2020 — the market’s peak just before the pandemic took hold — the S&P 500 closed at 3,386. It then proceeded to decline 34% in 33 days, amid the worst global health crisis in a century. But if you bought the Index at that epic top, and were still holding it on June 30 of this year, your total return with reinvested dividends has been close to 28%. I’ve never seen — and don’t expect to ever see again — a more vivid demonstration of Peter Lynch’s dictum that “The real key to making money in stocks is not to get scared out of them.”

I believe I was put here for just that reason: to help you not get scared out of them.

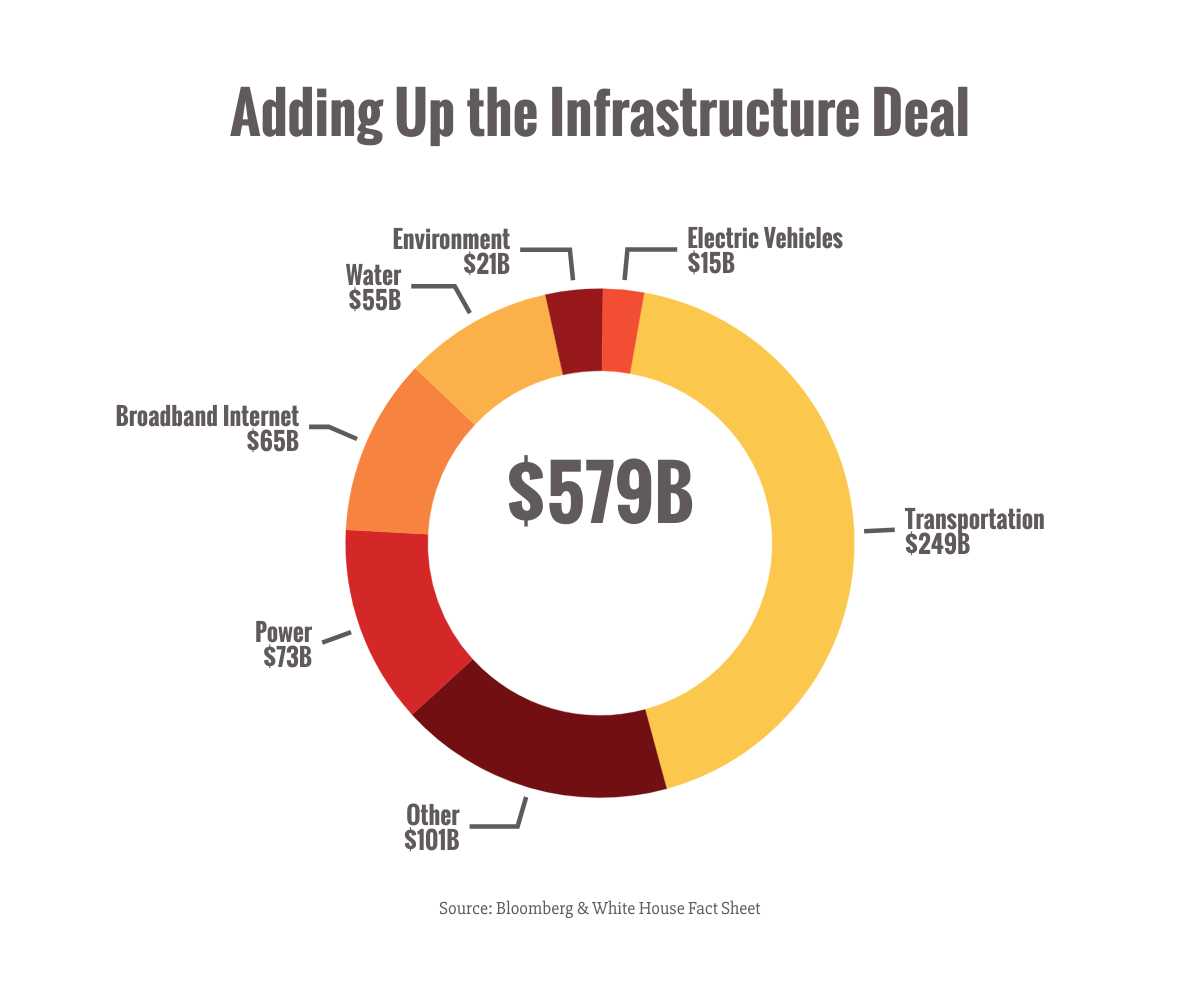

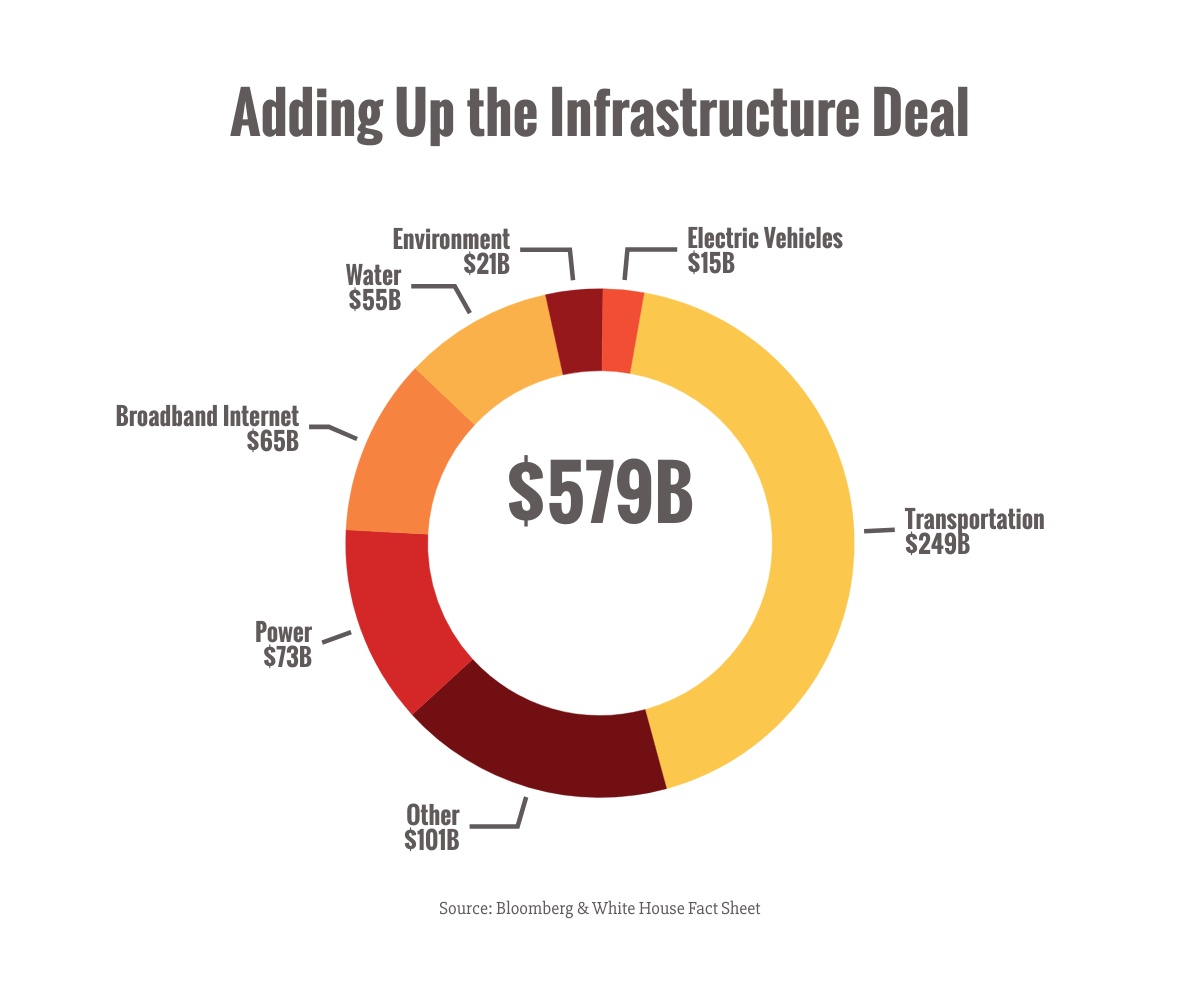

After weeks of grandstanding, posturing, and wrangling, it looks like a bipartisan infrastructure deal that both parties can live with is in the works.

Good news: no tax hikes. But you’ll want to read on because we’re not out of the woods yet.

The bipartisan deal (can’t call it a bill yet) finds $579 billion of common ground from President Biden’s original $2.25 trillion American Jobs Plan.1

It focuses on “hard” infrastructure — such as roads, bridges, rail, and public transit projects, as well as electric vehicle infrastructure and broadband internet — that both sides can agree on.

So, is it a done deal?

Not even close.

The current framework represents a compromise that makes no one happy, and there’s still a fair bit to hammer out (including how to pay for the plan).

The deal still needs to gather broad support in both parties, especially among those who think it’s too little or too much and might seek to scuttle the whole thing.

Fortunately, it doesn’t look like higher taxes are part of the deal. Though the math looks a little fuzzy from where I’m standing, it looks like funding sources could include repurposed pandemic funding, better IRS enforcement, and possibly digging through couch cushions for spare change (joking).1

So, that means my taxes won’t go up, right?

Not so fast.

There’s another bill on the table. And it’s a $1.8 trillion doozy.2

The second bill, called the American Families Plan, focuses on so-called “human” infrastructure and contains many Democrat-backed priorities like childcare, climate change, health care, and education.3

Basically, the initiatives that couldn’t get Republican support are packaged up in a separate bill.

It looks like the Democrats are planning to pass that bill through a reconciliation process that doesn’t require Republican support to get through Congress.

Inside that bill are the tax increases we’ve been on the watch for. Higher taxes on wealthy individuals and corporations, as well as eliminating the step-up basis on inherited assets, among other tax hits.4

Since the bills are independent, it’s really not certain yet which (if either) will pass. Or when.

Will one pass and not the other? Will both grind to a halt this summer?

Hard to say.

What does all this mean?

That depends on where you’re standing. For industries expecting to benefit, it means an influx of tasty government cash.

For those worried about America’s crumbling infrastructure, it represents some critical moves in the right direction.

For those concerned about the spending spree the government’s been on (and how we’re going to pay for it all), it’s another brick in a looming wall of debt that will eventually come due.

Bottom line, it’s not nearly over yet. I strongly suspect the coming weeks will be full of more politicking, more grandstanding, and more arm twisting.

I’ll reach out when I know more.

Now, go enjoy your summer. You deserve it.

Infrastructurally yours,

Chris

Chris Mullis, Ph.D.,CDFA® Founding Partner & Financial Planner

It’s a fascinating question because it cuts right down to the question of what it means to live in an uncertain world.

Humans are wired to dislike uncertainty.1

And we’re used to a fair amount of (often unwarranted) certainty in the models and paradigms we use to make sense of the world around us.

We’re so attracted to certainty that when economic forecasts and reports come back with “surprises” (also known as being wrong) we tend to freak out.

Especially when the news trumpets every weird bit of data like it’s a huge deal.

Over the last few weeks and months, we’ve had a lot of “surprise” reports.

Inflation surprises.

Job market surprises.

Housing market surprises.

Economic growth surprises.

Why are we so surprised?

In a year like 2021, the margin for error is greater than ever.

Predictions, forecasts, and expectations that are based on averages, trends, and other backward-looking methods are ill-equipped to handle the outliers and oddities of a year that’s unlike anything that has come before.

When in history has an entire global economy simply come to a halt?

And then arthritically restarted with many creaks and groans.

To my knowledge, it’s never happened before.

Of course the data is going to have surprises.

We’re probably going to get a lot of things wrong.

I can’t wait for the best-sellers written about all the ways we could have done things better.

So. What does that mean for you and me?

Crystal balls are out of commission.

Surprise is the order of the day, the week, and the year.

The models haven’t caught up yet (though that’s not stopping anyone from issuing very confident predictions).

So we’re being careful and looking out for the opportunities (as well as the hidden pitfalls) in these uncharted waters.

We’re cultivating patience, gratitude, and our ability to make good decisions with incomplete information.

To staying frosty,

Chris

Chris Mullis, Ph.D.,CDFA® Founding Partner & Financial Planner