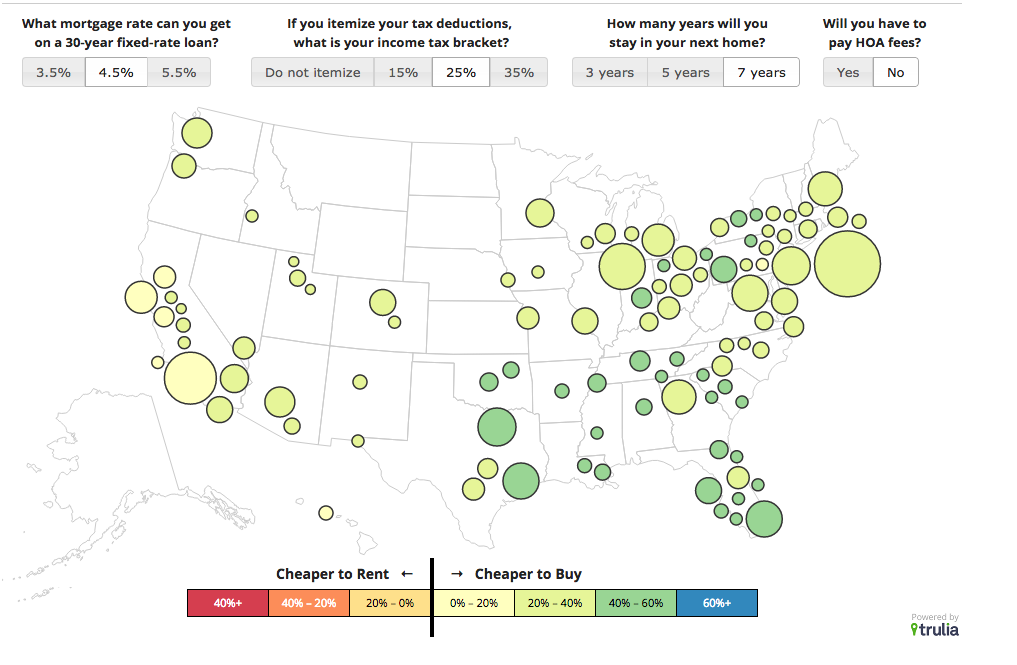

Renting vs. Buying: Which is Cheaper for You?

The decision to rent or buy a home depends on where you live, and also on your mortgage rate, tax bracket, how long you’ll stay put—and whether you’ll need to pay homeowners’ association fees. ‘Cause in some markets, this added cost makes renting cheaper than buying.

Click for an interactive graphic.

Source: Trulia