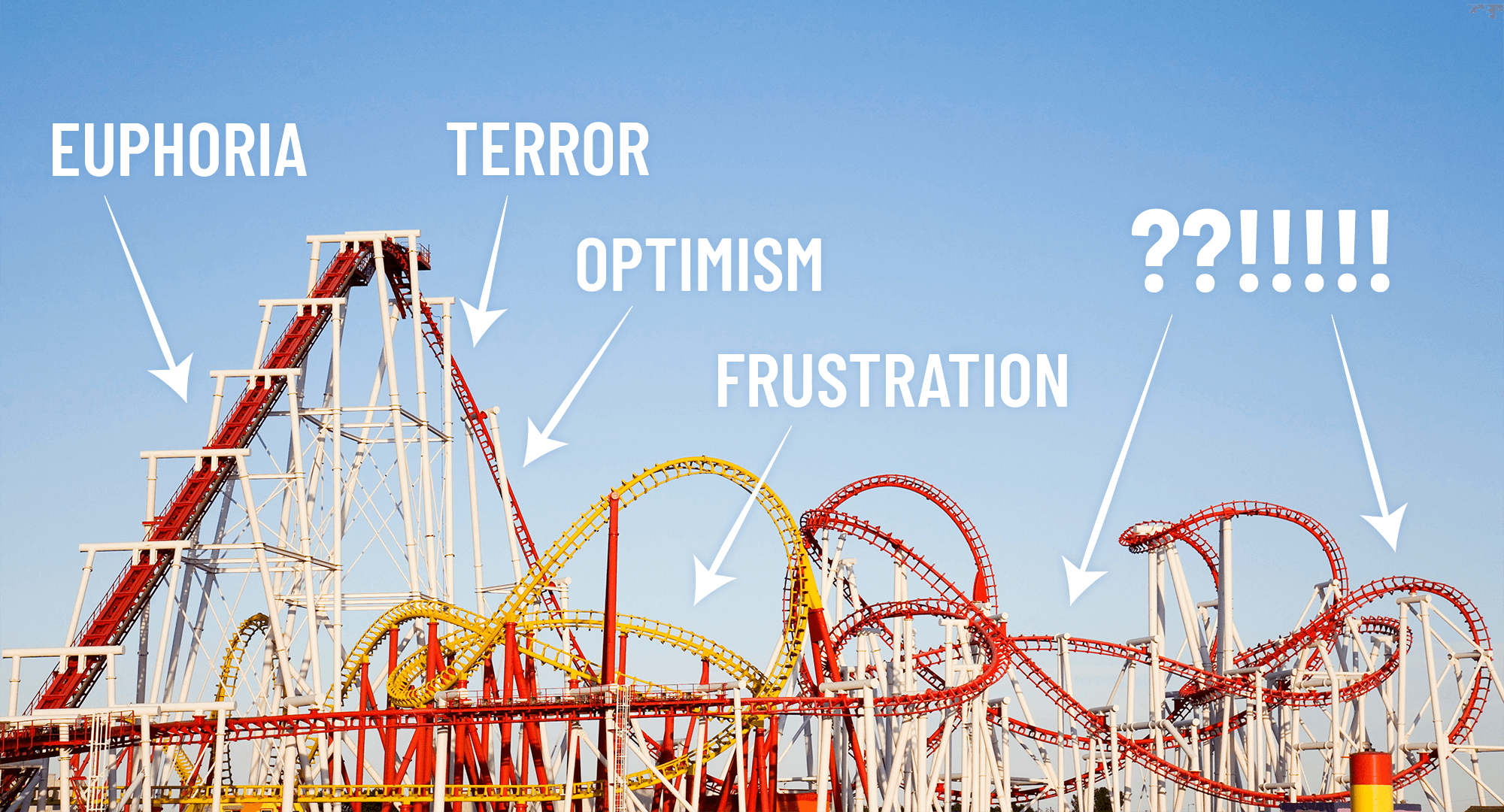

Rollercoaster ride?

Markets rallied in relief on some better-than-expected data on Friday.1 It was a bright spot in what has seemed like a relentless parade of bad news.

But the Dow, S&P 500, and Nasdaq still all closed out the week with losses.1

Is this the bottom of the bear market?

Maybe. Or maybe we’re somewhere in the middle with the loop-the-loops.

Let’s be prepared for volatility to continue.

Folks tend to focus a lot on the numbers, but emotions and behaviors may matter even more.

Knowing how to stick with a strategy during the loops and curves and uphills and downhills is a HUGE part of being a successful investor.

Market bottoms don’t come with a signpost. There’s no one waving a flag saying, “the worst is over, it’s all uphill from here!”

The end of a bear market looks an awful lot like the middle, and we don’t know if it’s the bottom until after we’re already past it.

That’s why it’s so important to stick to a strategy and not let the euphoria of a rally or the fear of drops sway our decisions.

Investors who bail during the downturns and miss the ride back up tend to lose spectacularly.

Why? Because the best days and worst market days have historically clustered.2

We don’t know how long this bear market will last. We don’t know if a recession is coming.

We do know this: you can’t enjoy the upside of the rollercoaster if you get off at the bottom.

Bottom line: it’s nice to get a reprieve from the selling pressure, but let’s be (emotionally and financially) prepared for a lot more volatility ahead.