How much inflation can the country afford before we’re in trouble?

Let’s discuss.

First, let’s get on the same page about some basics.

If you’ve noticed the price of a thing increasing over time (say, your favorite candy bar, postage stamps, or the cost of college tuition), that’s inflation in action.

Retirement planners and investment managers like us keep a keen eye on inflation because the whole point of investing our clients’ money is to keep up with or outpace the rising cost of living.

Economists use the broad increase (or decrease) in prices of goods and services across the country as a measure of economic health.

When inflation is stable and predictable, it’s a sign of a basically healthy, growing economy.

But, high inflation can quickly eat away at the purchasing power of your dollars, indicating that the economy might be overheated.

Deflation, or a decline in prices, can be a warning sign of a shrinking economy.

Recent data highlighted a surprise spike in inflation, indicating that prices increased faster than economists expected last month.1

Could this be a worrisome sign that the economy is overheated? Could $50 burgers be in our future?

Maybe.

On the other hand, could it be a temporary blip caused by the economy emerging from the pandemic-driven slowdown, complicated by supply chain issues?

Very possible.

Are the headlines catastrophizing?

They always are.

Let’s look at the data.

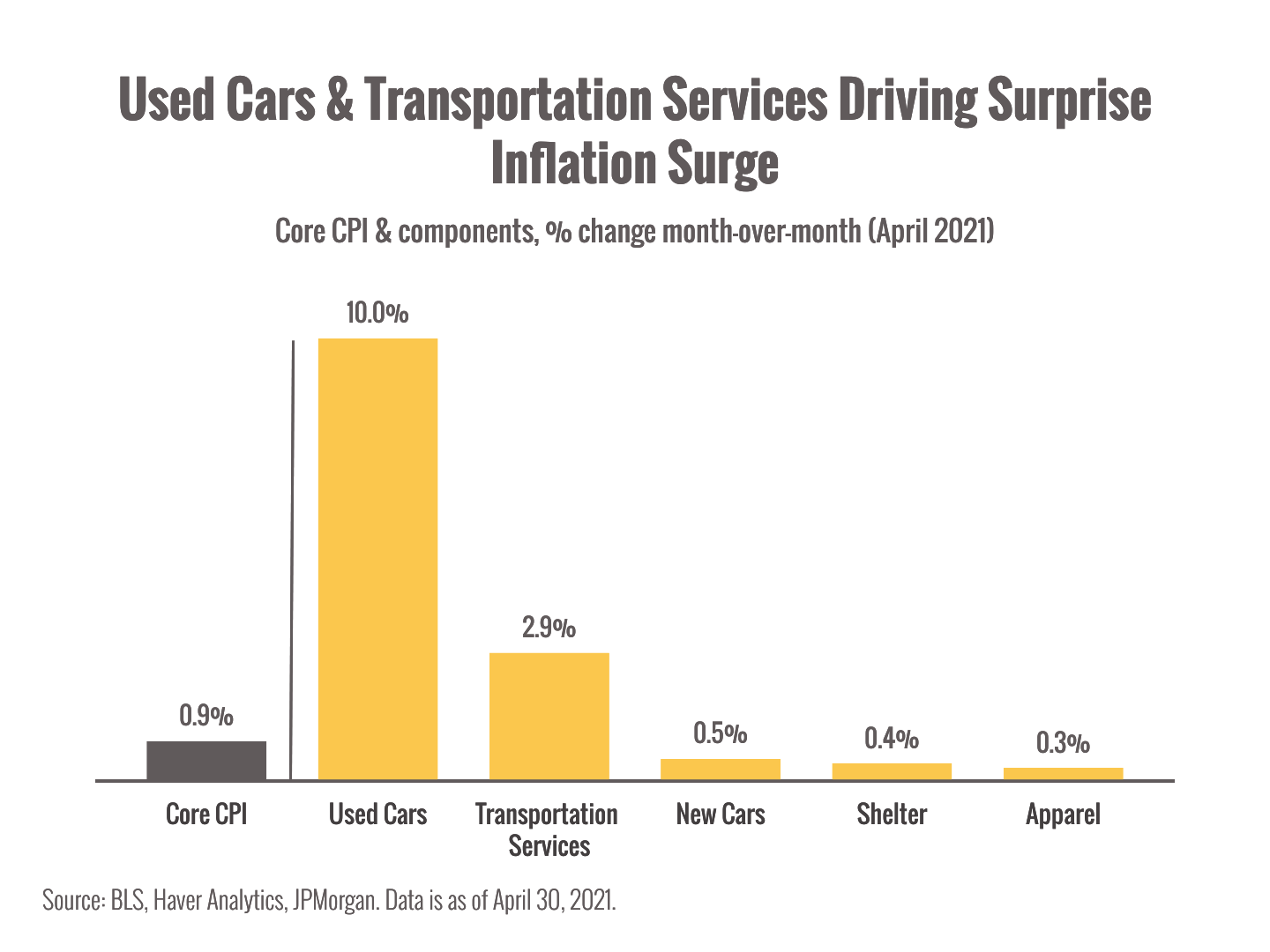

The Consumer Price Index (CPI), one of the major indexes economists use to track inflation, showed a surprising spike in April, igniting fears of runaway inflation.

Core CPI (which excludes the highly volatile categories of energy and food) showed a 0.9% increase in April month-over-month and 3.0% year-over-year. That’s much higher than the expected 0.3% and 2.3%, respectively.1

However, digging a bit deeper, we see that just two categories of goods (used cars and transportation services) accounted for the vast majority of the surge.2

That suggests things like flights and train travel suddenly became more expensive after a year of rock-bottom prices.

Is that runaway inflation or the normalization of prices as the world reopens?

We can’t tell from a single data point, but it’s not unusual to see prices increase in sectors that experienced a severe slowdown last year.

And the jump in used car prices? Well, many folks are turning to the second-hand market right now, in part because new cars are caught up in global supply chain bottlenecks for things like semiconductors and raw materials.3

Inflation is something to keep an eye on, especially in a year when so many of the usual variables have been thrown into flux. An ongoing surge in prices could hurt our wallets as our dollars buy less over time.

However, a single monthly spike following a very weird period for the economy is not cause for alarm yet; we should prepare ourselves for more odd numbers coming out of different parts of the economy in the weeks and months to come.

Shortages of everything from ketchup to gasoline could lead to price increases and fluctuations as supply chains attempt to disentangle from pandemic disruptions.4

Should we expect markets to react to inflation? How should we deal with it?

A negative market reaction in the short term is not surprising after weeks of strong performance. We should expect volatility ahead as we (and the economy) adjust to a post-pandemic world.

But remember, the stock market is a powerful hedge against inflation over the long term. During the last 90+ years, stocks have gained 9.8% per year while inflation has averaged 3% per year.

The engines of this elegant defense are the earnings and dividends of the great companies that we own which grow at healthy clips above inflation.

Plus value stocks, which play a key role in our NorthStar Globally Diversified Portfolio, tend to perform better than growth stocks when inflation surges.

Whether it’s high or low inflation, never lose sight of this enduring truth:

All lastingly successful investing is goal-focused and planning-driven.

All failed investing is market-focused and current events-driven.

Successful investors act continuously on her or his lifetime plan.

Failed investors react continually to economic (inflation!) and market developments.

Until next time,

Chris

Chris Mullis, Ph.D.,CDFA® Founding Partner & Financial Planner

Two things to discuss today: the economy (getting better) and taxes (going up?).

Let’s dive in.

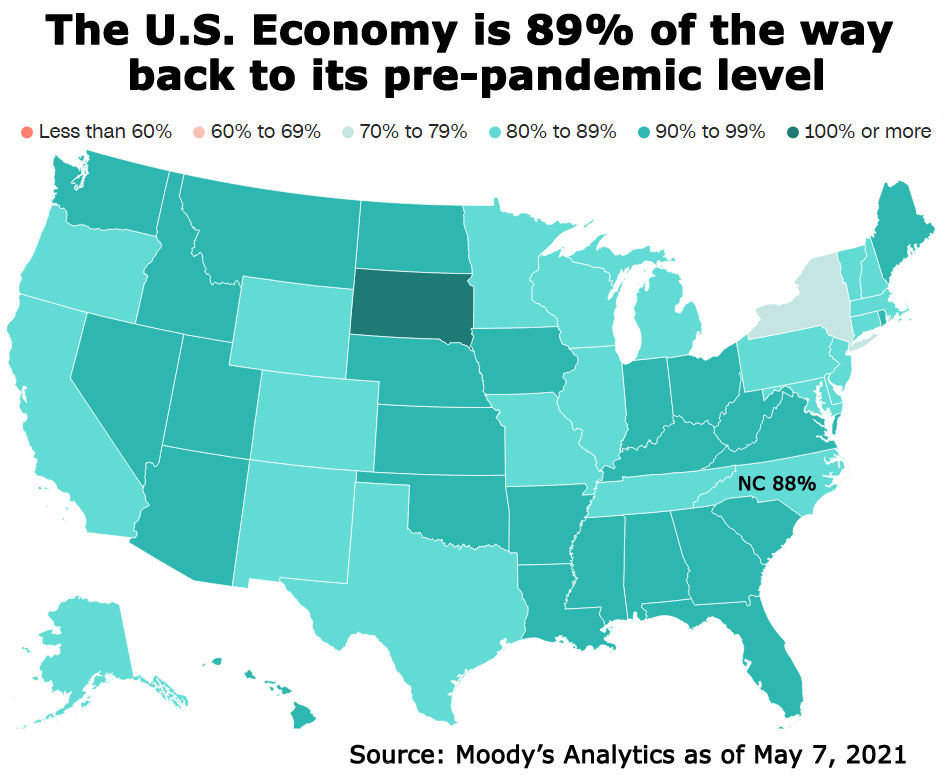

The light at the end of the tunnel is getting closer and brighter.

The economy is booming and we’re getting much closer to pre-pandemic levels of economic growth.1

COVID-19 cases are declining, as the math starts to work for us (instead of against us as it did at the beginning of the pandemic).2 As more folks gain immunity, there are fewer ways for the virus to spread.

All U.S. adults are now eligible for a vaccine.3

Yesterday the first shot was approved in the U.S. for children paving the way for inoculations before summer camps and the start of the next school year.4

Restrictions are easing and areas are opening up for travel, meaning we can start planning those missed vacations and seeing loved ones again.

After over a year of uncertainty and dread, the future is looking up.

Major COVID-19 surges in India and Brazil mean millions are still suffering.5

Viral variants mean the pandemic may not be “over” for a long time and we still need to be careful not to undo all our gains.

Many folks are not experiencing the economic recovery and may need years to recover what they have lost.

However, let’s not let the work ahead take away from the progress we’ve made.

Let’s take a deep breath and appreciate how far we’ve come since March 2020.

… Deep Breath …

Now, let’s talk about taxes.

President Biden just unveiled a plan to increase taxes on high earners to pay for economic reforms as part of the American Families Plan.6

What’s on the table is likely to change as political wrangling continues, but here are a few things we’ve got to consider so far:

A higher top income tax rate of 39.6% (though it’s not clear yet who falls into that top tax bracket).

Raising the top tax rate on long-term capital gains to 39.6%. With the 3.8% Medicare surtax, that means the highest earners could pay a 43.4% rate on gains.

The elimination of the step-up basis for estates, meaning heirs could get stuck paying taxes on capital gains over $1 million (even if nothing has been sold) when they inherit.

This change could impact folks who, for example, inherit family homes that have appreciated in value. They might want to keep the home, but may not be able to afford the tax bill.

So, should I be worried?

Alert and informed, definitely. Anxious and worried, no.

Here’s why:

This is a proposal. It’s got a long way to go before becoming law and the details may change.

It’s still unclear how much impact these proposed changes will actually have. There are many advanced strategies that can help mitigate the impact of higher taxes. That’s why tax and estate strategies matter so much.

A study done by Wharton Business School suggests that tax mitigation strategies could help avoid 90% of the proposed tax increases on capital gains.7

Bottom line, the proposed changes are concerning, especially with so many details left to be determined, but it’s not time to panic.

We’re paying close attention to the process and will be in touch if we feel changes to your strategies are needed.

Be well,

Chris

Chris Mullis, Ph.D.,CDFA® Founding Partner & Financial Planner Reduce Taxes. Invest Smarter. Optimize Income

That seems likely with a $2 trillion American Jobs Plan (that could eventually cost trillions more) on the table to bolster America’s crumbling infrastructure and invest in R&D.1

What could those tax hikes look like? Let’s consider the possibilities.

Though President Biden committed to not raising taxes on folks earning less than $400,000 per year, it seems hard to believe that he’ll be able to keep that promise with such a massive bill to cover.2

Also, it appears that married folks filing jointly could find themselves facing a big marriage penalty if they get swept over the $400k threshold as a household.2

One option on the table is a new auto mileage tax, which would raise money for highway infrastructure. Another is higher fuel taxes, which could increase what Americans pay at the pump.3 However, both proposals would be difficult to get through Congress, so they seem unlikely to come to fruition.

Some economists favor funding long-term infrastructure spending with ultra-long bonds and it’s possible Treasury Secretary Yellen will consider issuing 50-year bonds for the first time since 1911 to take advantage of low interest rates.4

Bottom line: we don’t know exactly what will ultimately come out of Congressional haggling; however, it’s smart to prepare ourselves for potentially higher tax rates in 2022.

What could those look like? While I don’t have a crystal ball, the following changes seem very possible:

A higher top income tax rate

A higher capital gains tax rate

A higher corporate tax rate

A lower estate tax exemption amount

We’ll know more as the final deal shakes out, but it’s clear these possibilities make 2021 even more critical for tax and estate planning.

In other tax news, the IRS has extended the deadline for making 2020 IRA and HSA contributions to May 17, giving folks an extra few weeks to get them in.5

Also, folks who already filed and paid taxes on 2020 unemployment benefits and are due money back under the recent rule change will automatically get refunds from the IRS, avoiding the need to file an amended return (unless they became newly eligible for additional credits or deductions).6

There’s a lot going on right now in Washington and we can’t know what the final resolution will be until all sides have their say.

However, it’s wise to remember that laws and circumstances change all the time. All we can do is stay on top and plan ahead as best we can.

This information is not intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax professional.

This is probably our most important share of 2021.

Tell us how well you appreciate this video and we’ll tell you how successful an investor you’ll be.

When an American’s portfolio suddenly declines 14% from a previous peak, he will never calmly announce, “I’m experiencing a perfectly ordinary, unsurprising, and above all temporary correction — indeed, merely the average intra-year correction of the last 65 years — and it will have no lasting effect on my long-term return.”

Instead, he screams, “I’ve lost 14% of my money, and there’s no end in sight!” as CNBC trumpets the apocalypse du moment.

Watch this video and be able to make that exceptionally calm and financially productive proclamation…”I’m experiencing a perfectly ordinary, unsurprising, and temporary…”

So, the next (final?) round of stimulus was signed into law by President Biden.

Let’s dive in.

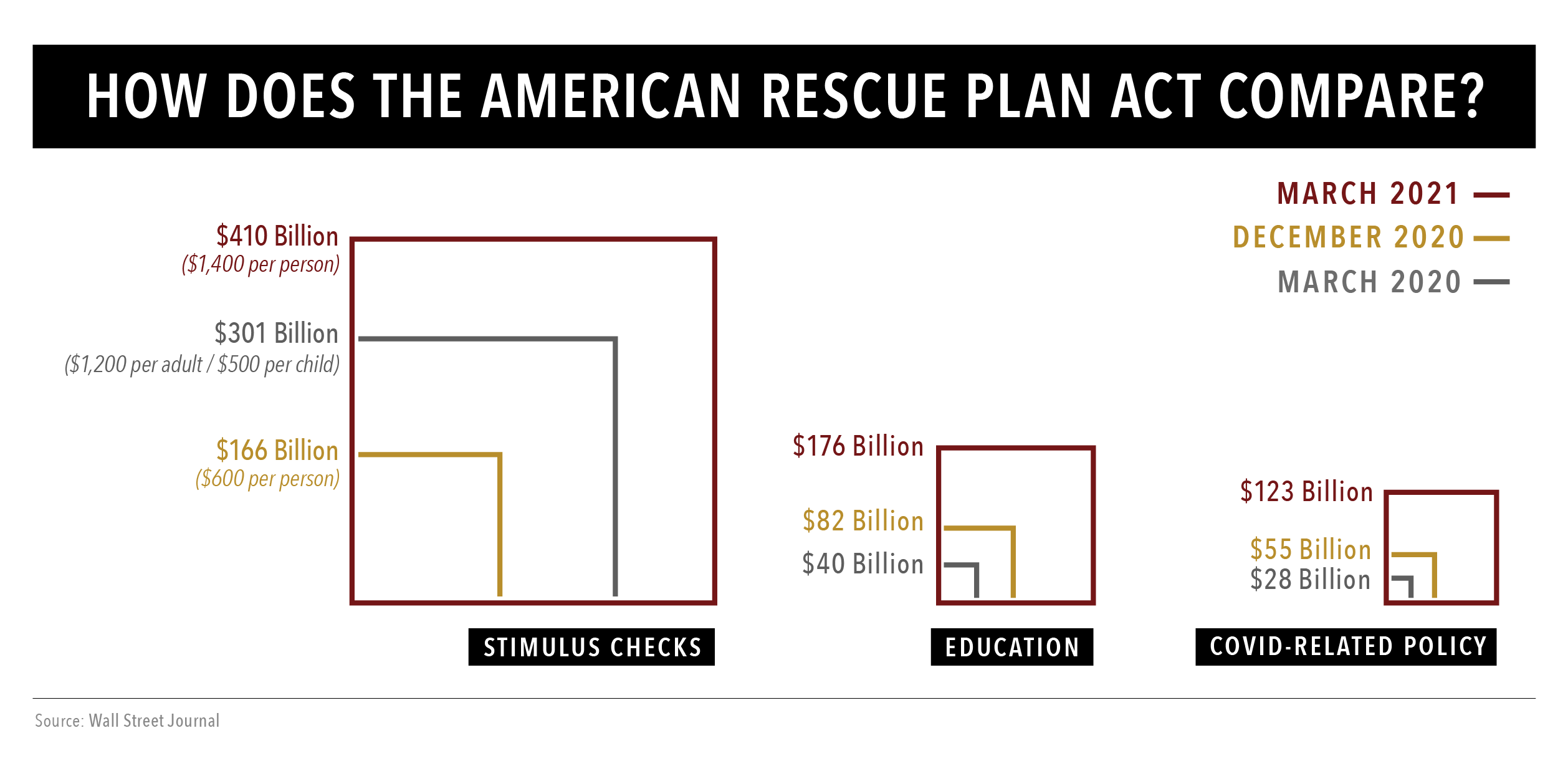

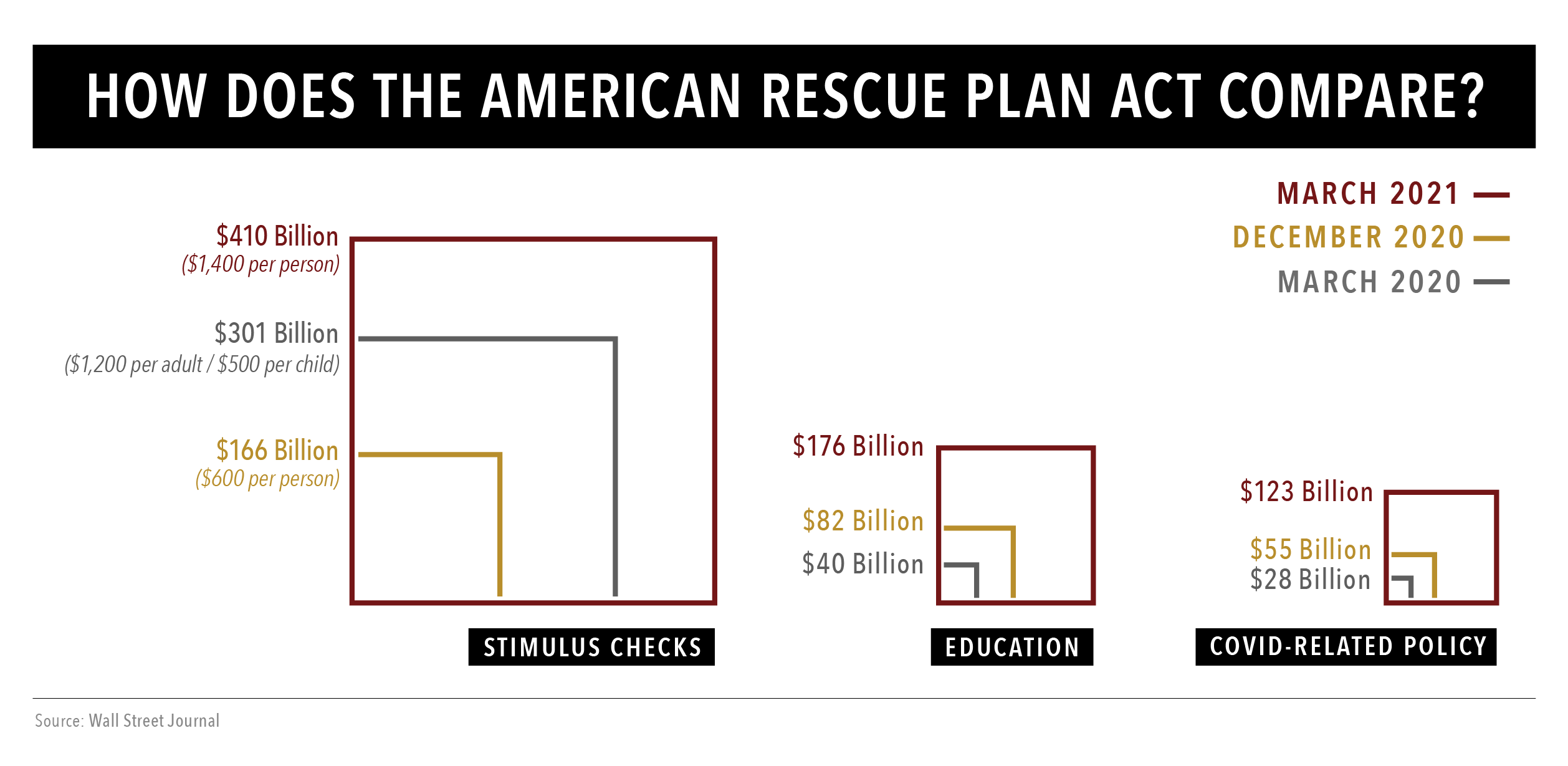

The $1.9 trillion bill called the American Rescue Plan Act of 2021 includes stimulus checks, child tax credits, jobless help, vaccine-distribution money, healthcare subsidies, and aid for struggling restaurants. What’s not inside? A higher minimum wage.

Here’s a quick visual of how it compares to prior rounds of stimulus.

Here are some immediate takeaways:

More stimulus checks are coming: $1,400 checks could be hitting bank accounts and mailboxes this month, going out to adults, children, and adult dependents such as college students and elders. These adult dependents did not qualify for previous payments, so that’s good news for many.1

Who gets paid? Individual filers who earn as much as $75,000 (or joint filers making $150,000), plus their household members, qualify for the full $1,400 per person.1

Folks filing as a head of household can earn up to $112,500 and still qualify for the full payment. Phaseouts kick in quickly this round, and an individual with an income of $80,000 or a couple earning $160,000 get nothing.1

If you’ve filed your 2020 taxes, your check would be based on that income. If not, it would be based on your 2019 tax filing. If you’re waiting for a missed payment, individual tax returns have an extra line called “recovery rebate credit” to claim your stimulus payment.

Enhanced unemployment benefits are extended through Sept. 6: Folks claiming jobless benefits will receive $300/week on top of what they already get from their state through the fall.2

Some unemployment income is now tax-free: Individuals who earned less than $150,000 in 2020 can shield up to $10,200 in unemployment benefits from taxes. For married couples filing jointly who both received unemployment, the tax-free amount goes up to $20,400, but the $150,000 income cap still applies. Unfortunately, if you earn over $150,000, it currently appears that all of the unemployment benefits become taxable with no phaseout.3

If this applies to you or someone you love, my advice is to wait to file or update your tax return until the IRS issues guidance on what to do.

The child tax credit is larger: The bill increases the child tax credit for one year to $3,600 for kids under 6, and $3,000 for kids between 6 and 17 (the current credit is a flat $2,000 per child under 17). 50% of the credit would be available as advance monthly payments that the IRS will start sending to families in July 2021.4

Unfortunately, not all families will qualify. Phaseouts begin at $75,000 for single filers, $112,500 for heads of households, and $150,000 for joint filers. However, families who earn less than $200,000 ($400,000 for joint filers) could still claim the regular $2,000 credit.4

Health insurance costs could drop on health exchanges/marketplaces: The bill removes the income cap on insurance premium tax credits for folks who purchase insurance on the federal health exchange or state marketplace (for two years). That means the amount you would pay for health insurance would be limited to 8.5% of your income as calculated by the exchange.5

Final thoughts

A lot of rules have changed in the last year, throwing an already complex tax season into a bit of confusion.

Could there be more stimulus passed this year? It seems unlikely if the U.S. economy continues to expand.

According to a fresh estimate, our economy will expand nearly twice as fast as originally expected, growing at an estimated 6.5% in 2021 versus the 3.2% projected in December.6

Obviously, these projections rest on a lot of assumptions about vaccination rates, reopening, and consumer spending.

Let’s hope we stay on track.

That was a lot of information to absorb. Have questions?

P.S. Markets have hit new highs as fears of out-of-control inflation faded and hopes about the recovery surged. The usual caveats apply: we’re in a roaring bull market and any time stocks reach new highs, pullbacks and corrections are possible. Keep calm, cool, and focused. I’m here for questions.7

P.S.S. The last day to contribute to an IRA for 2020 is April 15, 2021.

For the past year, it has seemed (to me, anyway) that the stream of bad news has mainly been interrupted by worse news.

Every week it seems we’re confronted by death tolls, natural disasters, political shenanigans, business closures, viral variants, and more.

It’s so easy to become fixated on doom scrolling and negative headlines. The media makes that easy.

But what if things are getting better?

How would your life change if things were getting back to normal?

Are you ready for that?

Because I think we’re on the upswing.

Here’s why I think things are going to get better rapidly in 2021.

Vaccines are proving to be effective against COVID-19 and we’ve got several of them.1

At least one (the newly approved Johnson & Johnson vaccine) is effective against the vicious new variants that have popped up.2

Vaccine rollouts are going (kinda) well and are accelerating. Once a large proportion of Charlotte and cities across America are vaccinated, we can expect to see community transmission rates plummet and normal life resume.

Imagine what that will feel like.

Economists think a tidal wave of growth is coming and the economy will roar back this year.3

That’s good news for businesses, workers, and markets.

The next round of stimulus looks like it’s going to get passed in the next couple of weeks, getting money into the pockets of the folks struggling to pay bills and keep their businesses open.

That’s a lot of good news.

What do you think, are you ready to start planning life after the pandemic?

What’s the first thing you will do when it’s safe?

Me? I’m going to give everyone I love a big hug.

I can’t wait.

Does that mean that everything’s going to be just peachy?

I wish it would, but I don’t think it will. We’ve lost too much and still have too much to do.

The 500,000+ folks we lost to the pandemic. Each one a vibrant member of our society and a loved one.

The millions of jobs that probably aren’t coming back.4

The medical staff, essential workers, and teachers who are burning out under the strain of a pandemic.

The divisions in our society that still remain.

Markets are frothy and volatile and will likely remain so. A temporary sell-off is quite possible.

But, I’m hopeful for 2021.

Are you?

Yours optimistically,

Chris Mullis, Ph.D.,CDFA® Founding Partner Reduce Taxes. Invest Smarter. Optimize Income

P.S. Though the new stimulus bill has been passed by the House, it still has a ways to go before being passed into law.5 And it’s likely that the Senate will make modifications before passing it.

Chris Mullis, Ph.D.,CDFA® Founding Partner Reduce Taxes. Invest Smarter. Optimize Income AskNorthStar.com(704) 350-5028

This information is not intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax professional.

Transcription:

Hi, I’m Dr. Chris Mullis with NorthStar Capital Advisors, and I’m here to help you make the most of your tax savings opportunities.

In this video, I’m going to talk about what could happen, and what you can do to potentially maximize your tax savings before the rules change.

We don’t know when tax laws might change but we know they will at some point. That’s what tax laws do.

Our philosophy at NorthStar is that we have a moral obligation to pay the IRS every dollar we owe, but “leaving a tip” doesn’t make us more patriotic.

And if we ever save you “too much” in taxes, you can donate the difference to your favorite charity or even against the national debt for which you’ll receive a deduction which is better than overpaying your taxes.

Now before we describe some of the current-event driven opportunities, please let me remind you an essential truth — playing the long game is where we win in taxes.

The way that most people prepare taxes is one year behind. What happened last year and what do I need to minimize that tax bracket. The problem is you’re playing the IRS’s game and you’re going to lose looking at it one step at a time.

We may or may not be able to beat the IRS working in this narrow, one-step fashion, but you give us time and tax planning, and we can save hundreds of thousands of dollars.

Now that we’ve underscored the criticality of long time horizon in successful tax planning, let’s pivot to more time-sensitive issues.

We have a new administration in Washington, and the Democrats control the House and the Senate. So, what’s next for taxes?

In the near term, we can expect lawmakers to focus on urgent issues, like vaccine distribution, stimulus aid, and the economy. But at some point, a new tax plan is likely to show up.

The Biden administration is likely to raise taxes, at least for some folks. Hopefully, not until the pandemic settles down and the economy gets stronger.

If 2022 sees tax rule changes, 2021 might be our last chance to take advantage of the current rules.

So, what actions can you take now to make the most of today’s low tax rates?

Here are three key areas of your taxes you want to consider in 2021.

Point #1: Biden’s proposed plan targets high-income earners for an income tax hike. If that’s you, 2021 may be an excellent time to consider accelerating income (especially if you own a business) or completing a Roth conversion.

These are big moves with financial consequences, so you’ll want to get advice before you pull the trigger.

Point #2: Estate and gift tax exemptions went up to $11.7 million this year, but they might drop again under a new tax plan. That makes 2021 a critical year for estate planning.

Please don’t think new laws couldn’t affect a much smaller estate, either. As recently as 2001, the federal estate tax exemption amount was just $675,000.

It’s not likely that new rules would go back to such low levels, but I don’t want you to be caught flatfooted by a change.

Point #3: Deductible retirement plan contributions might be treated differently for tax purposes in the future. If you’re a high earner, maxing out deductible contributions this year and considering a Roth-style plan in the future might be smart.

Tax laws are in a constant state of flux. We don’t know when the rules will change or what they’ll look like once Congress gets done haggling, but we can take some proactive steps now.

Part of my job as a financial planner is to help you stay on top of the rules and maximize your opportunities every year.

Remember — tax planning is a cornerstone of real financial planning. And it’s a game of chess won with a multi-year perspective.

If you have a question about what I’ve discussed in this video or you’d like to speak personally about what’s going on, please reach out. I’ll respond personally.

P.S. The market boom times are here, and a lot of folks are looking for magic bullets. But there aren’t any. It’s easy to look brilliant in a rising market or feel like you’re missing out on a hot trend. But the tide will turn. It usually does. If FOMO is keeping you up at night, (or keeping your kids up at night because they’re experiencing their first big bull market) please reach out. We’ll talk about the difference between gambling and investing. And how building wealth takes consistent, incremental progress, not chasing fads.