Are We Still in a Recession + Some Good News

So, what’s going on with the economy?

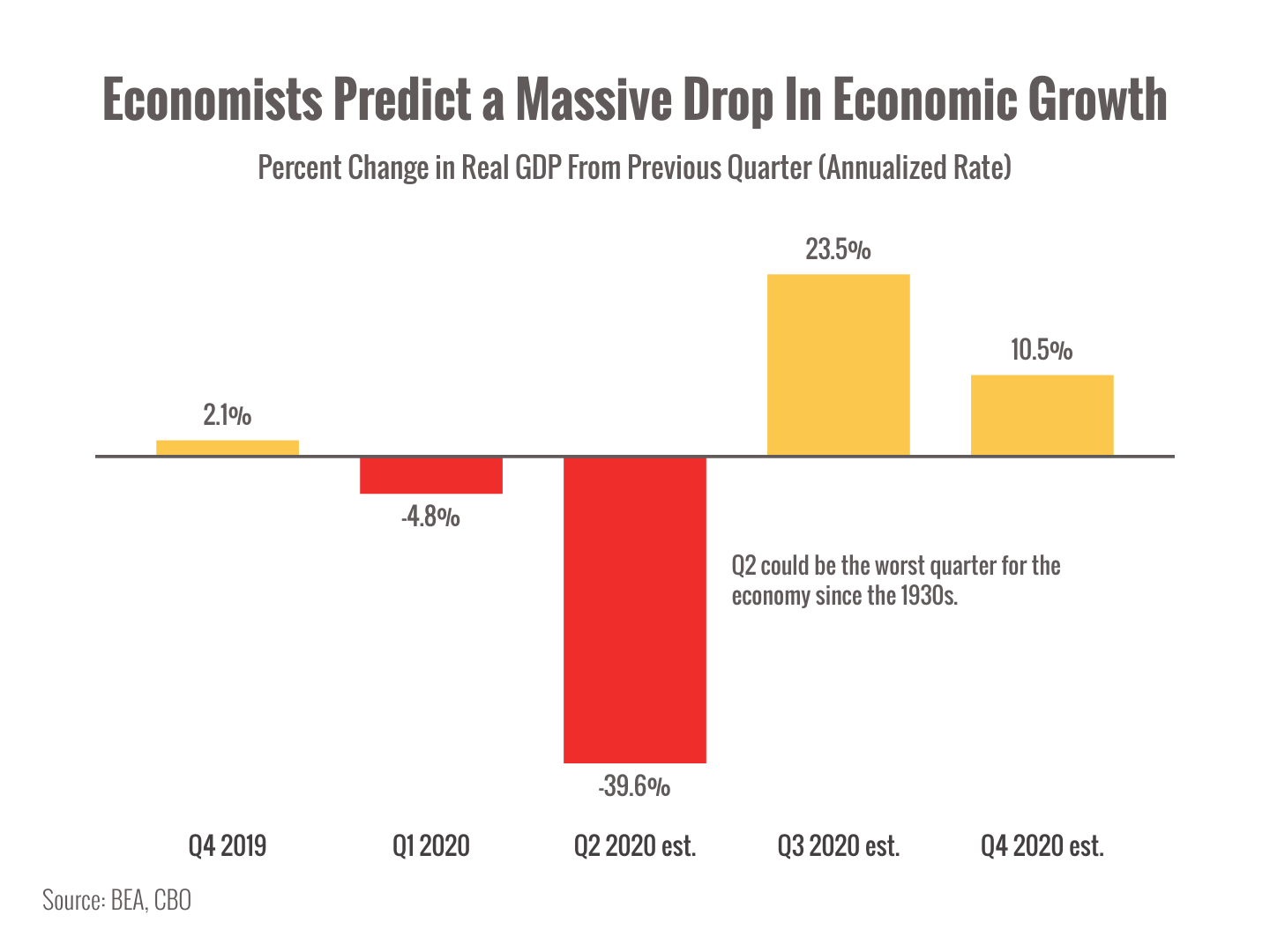

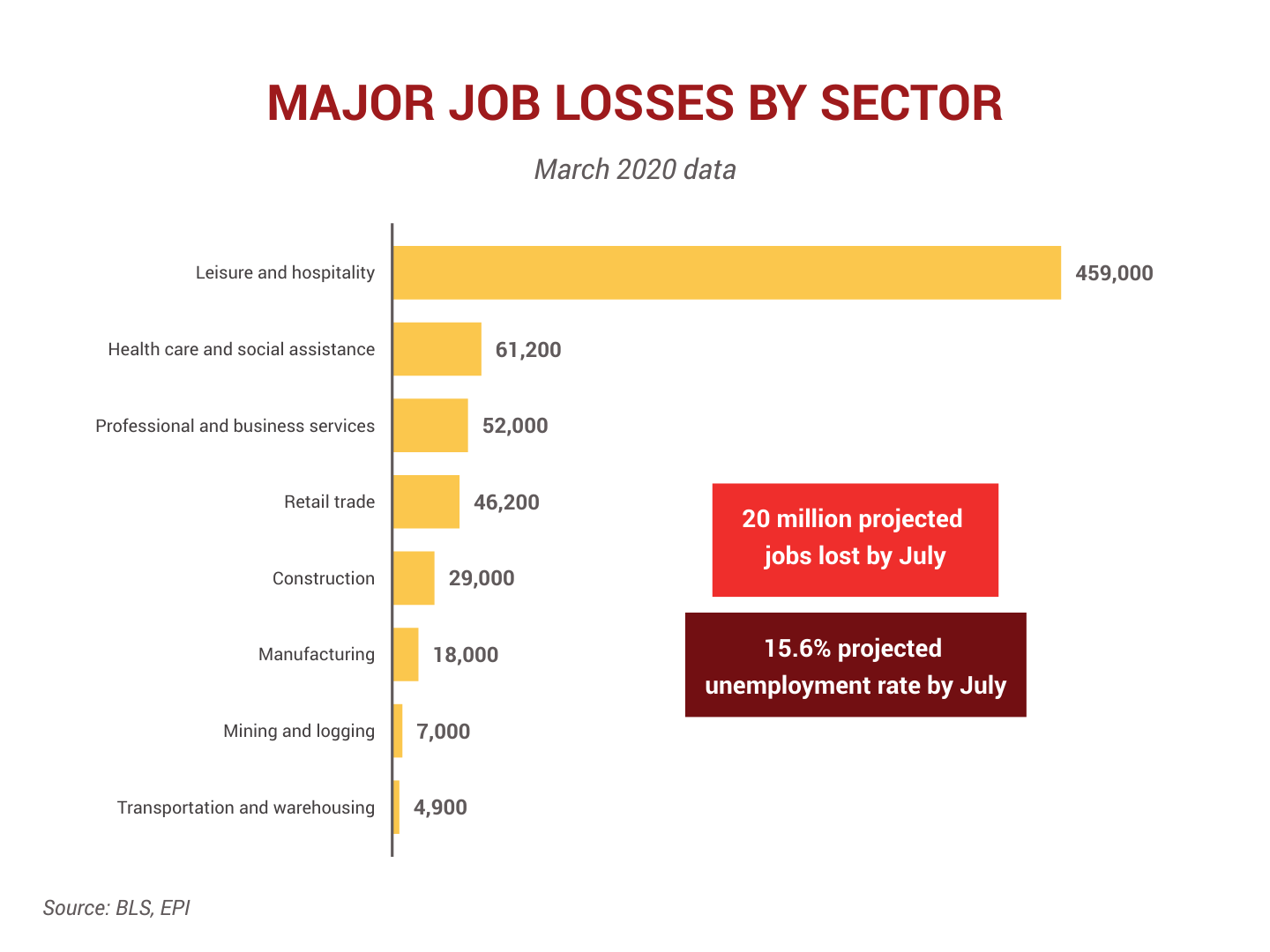

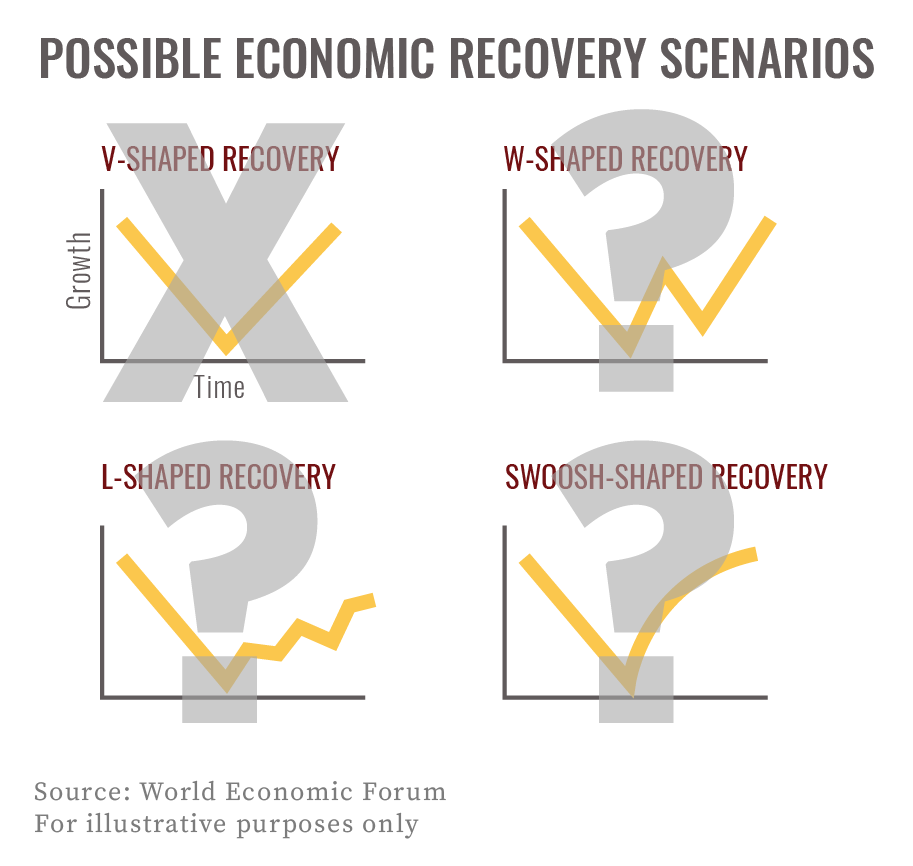

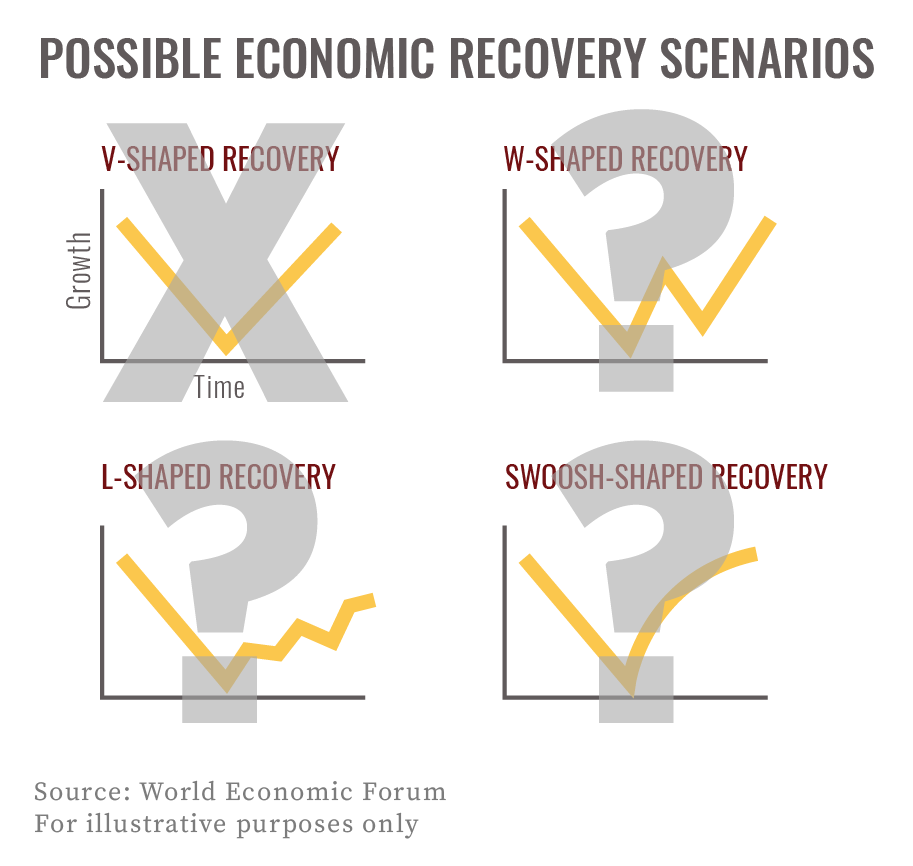

Well, hopes for the “V-Shaped” recovery economists wanted seem to be fading.1 Though businesses reopened and millions of people got their jobs back, millions more are still unemployed.2 And more layoffs are likely coming.3

Does that mean we’re still in a recession?

Technically, we won’t know until Q2 and Q3 economic data are released.

Best guess? We’re probably still in a recession.

The more optimistic recovery scenarios depended on containing COVID-19 infections so Americans could safely get back to business.

That…didn’t happen.

The question now is whether rising infection rates will put us in a “W-Shaped” double-dip recession, or a slower “L-Shaped” or “Swoosh-Shaped” climb back.

That’s all very interesting, but how does it affect us in Charlotte?

In many ways, our local economy is a microcosm of the larger state of affairs.

As COVID-19 cases have drifted back higher in the Queen City and North Carolina, we’ve still got a ways to go before we’re on solid ground.

Our ability to bounce back depends on a few things: 1) keeping infection rates down; 2) workers keeping the jobs they have and returning to the ones they lost; 3) folks shopping, eating out, and spending money locally.

In terms of markets, the recent gains make it clear that investors are looking past the current gloom to a hopefully rosy future.

Are they clairvoyant? Foolishly optimistic? Not optimistic enough?

I agree with Yale economist Dr. Robert Shiller’s take: he thinks this is a FOMO market driven by the Fear Of Missing Out.

Many investors regret not participating in the 2009 rally and are determined not to miss out again. That psychological narrative is pushing up the market even in the face of bad news.4

Will it continue?

We’re in earnings season and investors are waiting to see how badly U.S. companies were damaged last quarter.

Since many companies have refused to release earnings forecasts, we’re prepared for surprises. Positive and negative.

Bottom line: Buckle up, I think we’re in for a choppy ride.

Ok, so where’s the good news you promised?

When times are tough and headlines are overwhelmingly negative, it becomes harder to find the good news. But it’s there:

- A New Jersey hospital once described as a “war zone” now has zero COVID-19 patients.5

- 17 COVID-19 vaccines are in human trials. At least one may be ready for approval by the end of 2020.6

- 2 million folks gathered to plant trees in Northern India (while maintaining social distance).7

- A young man who lost hope of attending college is headed to Harvard Law after the good people he met as a sanitation worker took him under their wings.8

Uplifting stories are out there if we look for them.

7https://apnews.com/f1d41fd4772742279da89e972dd8493d

8https://www.cnn.com/2020/07/07/us/sanitation-worker-harvard-law-trnd/index.html