NorthStar Client Family Featured in AARP The Magazine

Debra and Gary Wilhoit, a NorthStar client family, are featured in the June/July 2016 issue of AARP The Magazine. Dr. Chris Mullis, CEO and senior planner at NorthStar, is quoted in the article alongside senior advisors from Charles Schwab and T. Rowe Price.

Kudos to the Wilhoits for candidly sharing their early-retirement anxieties and the actions they have taken to ultimately reach greater peace of mind and long-term success. Millions of Americans who are transitioning toward and into retirement can immediately relate to the Wilhoits’ experience. And millions of Americans can benefit by adopting the Wilhoits’ long-term perspective and positive investor behavior.

AARP The Magazine addresses the evolving life stages of 50+ Americans and is the largest circulation magazine in the United States (35.9 million readers).

Advice for New (and soon-to-be) Retirees

Dr. Glyn Cowlishaw (right), Head of School, stands with 9 of the 10 retiring faculty and staff honored during a reception in the McMahon Fine Arts Center theater May 12 at Providence Day School. Pictured (from left) are Middle School Head Sam Caudill, Summer Programs Director Nancy Stockton, Admissions Associate Director Barbara Bodycott, Lower School Computer Science Department Chair Beth Hunter, Lower School Librarian Debra Wilhoit, Extended Day teacher Judy Bennett, Lower School Head Kay Montross, 3rd-grade teacher Marsha Small and Middle School math teacher Beth Ralston. Not pictured is Janis Roten of the Business Office. (Photo credit: Mike McCarn / Providence Day School)

Yesterday I had the honor to attend the retirement ceremony for two of my former & beloved teachers and seven additional educators that came after my time as a student. These nine individuals provided great leadership & passion over many decades and impacted thousands of students’ lives, including my own. The level of professional and personal adoration expressed by the school community for this exceptional group of educators was incredibly moving. One presenter captured the moment perfectly saying to effect, these retiring teachers are Mount Rushmore figures in the field of master educators! Inspired by their greatness and to honor the start of their next great adventures, we share the following advice for new retirees. Congratulations and thank you to the newest members of the “Golden Chargers” at Providence Day School. — Chris Mullis

Some years ago the consulting firm PricewaterhouseCoopers conducted a survey to reveal what new retirees need to understand to make their retirement more meaningful and to ease this major life transition. The following are excerpts from the survey results.

Initial Thoughts

Most of the new retirees strongly recommended keeping active, whether in volunteer work, hobbies, travel, reading, or new business ventures. Words of wisdom included:

- Use your talents and realize this is a “new beginning” and not an end.

- Set goals two to three years in advance. Good planning is helpful … focus on financial and emotional issues.

- You should develop a routine (daily) and not just allow things to happen or not happen—you really are on your own—work, family, etc.

- Learn to relax without feeling guilty about it! Stay busy, mentally and physically. Remember, it’s never too late to learn new things and improve old things.

- Make a priority list of the things you’ve always wanted to do but didn’t have the time to do. Start doing the highest-priority items immediately.

- Consider retirement a process rather than an event.

- Don’t worry about how you will fill your day. If you are reasonably active physically, have outside interests and are willing to be involved in your community affairs … you will wonder where the time flies. But nail down the finances.

Your Significant Other

A frequently overlooked but important aspect of retirement is the new or different relationship with one’s spouse. A new retiree may need to be careful not to intrude or tread on a spouse’s independent lifestyle. Spouses offered the following comments:

- Retirement is great but not for lunch.

- Remember we have lives that are already full, and don’t expect to be waited on all the time.

- Spouses have their own life in community activities. Make sure you don’t make them feel guilty when they continue their own lives.

- Be prepared for a lot of togetherness. [One wife described it as half the money, twice the husband.]

- Continue to pursue and respect other interests; take care of your health.

- Sit down and review life’s priorities. Develop a jointly agreed-upon plan, together with benchmarks concerning the high-priority items. Allow plenty of time to relax together.

Expectations

Most retirees were surprised at how easy it was to fall into a new routine. Common sentiments included:

- Instead of being bored and frustrated I found a new sense of freedom. For the first time in years I was my own boss and totally accountable for my state of mind.

- The first six months [were] lonely and depressing that your successors never ask for your advice … followed by bliss!

- How hard I thought it would be and how easy it really is.

- [I was surprised that] my handicap did not drop by 10 strokes.

- [You will be surprised by] how much you will miss the relationships and connections that you leave behind at work.

What They Would Do Differently

Lastly, new retirees were asked what they would have done differently before retiring. Most respondents said they would begin retirement planning, including financial and tax planning, at an earlier stage. Here are some insightful comments on this topic:

- Put as much of the financial/administrative side of life on automatic pilot as soon as possible. Simplify and try to get out of the middle of all the minutiae.

- We traveled extensively the first year. I would spread it out, but highly recommend travel.

- Develop a greater understanding of the income tax considerations in the year of retirement.

- I would have said appropriate farewells (good-byes) to all colleagues.

- Would have done advance planning (for post-retirement activities) one to two years before actually retiring.

Source: PwC

Remove Hidden Risks from Your 401(k)

Have you heard of Valeant Phramaceuticals? Or how about the Sequoia Fund? Valeant is a drugmaker whose stock price has tumbled 70% this year on a potential accounting scandal. Sequoia is a mutual fund who took an out-sized stake in Valeant. Sequoia has fallen sharply, trails 98% of its peers, and their CEO just resigned.

Have you heard of Valeant Phramaceuticals? Or how about the Sequoia Fund? Valeant is a drugmaker whose stock price has tumbled 70% this year on a potential accounting scandal. Sequoia is a mutual fund who took an out-sized stake in Valeant. Sequoia has fallen sharply, trails 98% of its peers, and their CEO just resigned.

Why should all this matter to you? First, if you’re employed at one of the 50+ American companies that offers the Sequoia Fund as a retirement plan investment option, you may be unwittingly part of this debacle. Second, if you’re lucky enough not to be directly impacted, you should take this as a lesson and an opportunity remove similar risks from your retirement portfolio.

Incredibly, the Sequoia Fund is one of the most widely held investment options for Walt Disney employees. It’s relatively rare for major employers to offer risky mutual funds like Sequoia that make concentrated bets. Such “high-octane” funds have no business being present in 401(k)’s and similar retirement plans. Plan sponsors could even face class-action lawsuits from investors caught up in this avoidable mess.

How can you protect yourself?

- Step #1: Educate yourself about what’s in your retirement portfolio.

- Step #2: Pivot toward a massively diversified portfolio that favors low-cost, tax efficient index funds versus expensive, actively managed funds like Sequoia.

- Step #3: Visit 401k.nstarcapital.com to access portfolio recommendations for +120 company retirement plans. Don’t see your company in the list? Shoot us an email (info@nstarcapital.com) and we’ll add your plan!

4 Weeks Until an Important Deadline

Here’s an important reminder if you have an individual retirement account (IRA) or are considering opening an IRA. 2015 contributions to IRAs can still be made up through April 15, 2016.

Make it a double? If you really want to make the most of the growth potential that retirement accounts offer, you should consider making a double contribution this year: a last-minute one for the 2015 tax year and an additional one for 2016, which you’ll claim on the tax return you file next year. That strategy can add much more to your retirement nest egg than you’d think.

2015/2016 Annual IRA Contribution Limits*

- Traditional/IRA Rollover: $5,500 ($6,500 if you are 50 years old or older)

- Roth IRA: $5,500 ($6,500 if you are 50 years old or older)

- SIMPLE IRA: $12,500 ($15,500 if you are 50 years old or older)

- SEP IRA: $53,000

*Note: The maximum contribution limit is affected by your taxable compensation for the year. Refer to IRS Publication 590 for full details.

The savings, tax deferral, and earnings opportunities of an IRA make good financial sense. The sooner you make your contributions, the more your money can grow.

If you have any questions or would like to make an IRA contribution give us a call at (704) 350-5028 or email info@nstarcaptical.com.

Retiring in a Bear Market

AARP recently reached out to our firm to get advice on what people should do if they are going to end up retiring in a bear market. Here are our leading thoughts that we shared:

AARP recently reached out to our firm to get advice on what people should do if they are going to end up retiring in a bear market. Here are our leading thoughts that we shared:

- First, let’s address the premise that you’re retiring into a bear market because you may in fact be jumping the gun! There are always talking heads in the financial media warning of an imminent bear attack. Pessimism sells and being a pessimist makes you look smart. Just look to the recent past. Every single year for the past five plus years “pundits” have threatened that a bear market is just around the corner. Meanwhile, the market has pushed onward, just like it does a majority of the time, and delivered a fantastic run up in value.

- Don’t start planning for a bear market after it occurs. Since timing the market is essentially impossible, you want to structure your investments to be a stable ride whether it’s an up or down market. In fact, if you have a properly diversified portfolio with a robust mixture of stocks and bonds, you’ve got the all-weather portfolio that you need. Technical note — high quality intermediate-term bonds are your best option for preserving capital during an economic disaster.

- What about your attitude and, more importantly, your behavior? Prepare yourself psychologically to keep calm and carry on regardless of the investment environment. Getting your attitude and expectations in check will decrease the chances of making an unforced error and blowing up your portfolio. Have a plan and stick with it. If you need help, don’t hesitate for a moment to hire a financial coach because this is the most important game of your life.

- When you’re actually in a bear market, you’ll know it. By convention, market values will be off more than 20% and everyone’s attitude will be gloomy. While the market is down there are concrete steps that you can take to avoid straining your retirement nest egg and denting its future potential.

- What you want to do is avoid withdrawing from your investments as much as possible.

- delay major expenditures

- temporarily cut back on your travel and other discretionary spending

- draw down on your cash reserves to provide temporary retirement income

- if you have to draw from you portfolio, preferentially sell your bonds so stocks don’t get sold after a crash

- even consider a part-time job or consulting gig to supplement income

- The less you draw from your portfolio during the bear, the greater the spring back will be in its value when the market recovers. Historically, bears hit fast and then the market recovers quickly so you shouldn’t have to take these emergency countermeasures for too long.

- Another technical note — don’t forget to continue to annually rebalance your portfolio even in a bear market. Those intermediate-term bonds should be up in value which will provide you dry powder to buy stocks when stocks are on sale at temporarily diminished prices.

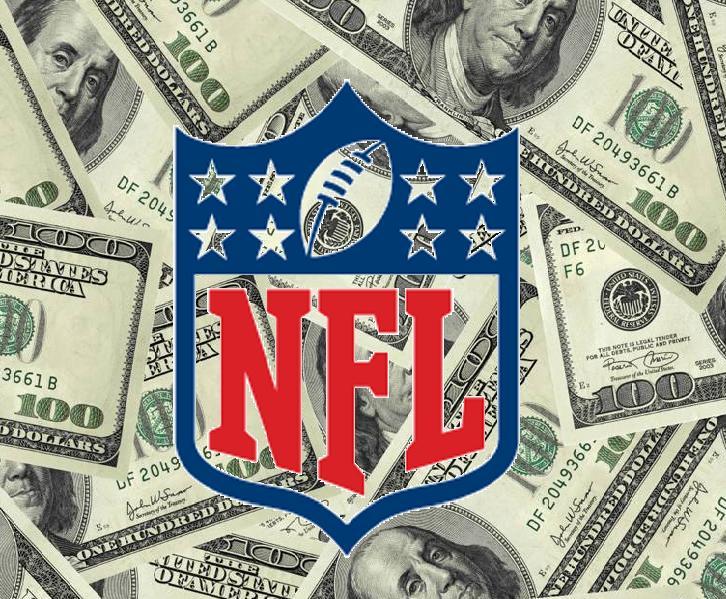

Retiring from the NFL

This Sunday’s Super Bowl 50 match-up between our hometown Carolina Panthers and the Denver Broncos is the talk of the town. But what happens after the Super Bowl? Potentially way after the game when a professional football player retires?

This Sunday’s Super Bowl 50 match-up between our hometown Carolina Panthers and the Denver Broncos is the talk of the town. But what happens after the Super Bowl? Potentially way after the game when a professional football player retires?

It turns out the National Football League has a rather generous pension plan. The NFL is one of the rare 7% of American companies that offers traditional pensions to new hires. That figure is way down from the 62% level seen in 1979.

Only a few years ago the NFL had the worst funded plan of the four major sport leagues, reaching a low 49% of assets on hand to fund future benefits. Their funding ratio has made a dramatic recovery since then to 72% and NFL owners have committed to 100% funding by 2021.

The NFL pension plan has $1.8 billion in assets with 4,200 retirees and 2,100 active players. Players qualify after 3 seasons and are eligible to draw benefits starting at age 55. An 18-year veteran like Peyton Manning would receive an estimated annual pension $107,040 compared to a 3-year, short-timer’s check of $21,360.

Although most corporations have done away with pensions and shifted the risk and responsibility of saving for retirement to their employees, the NFL’s program is strongly in place thanks to the community of active and retired sportsmen. NFL retirees do a great job of communicating the great benefit of the pension to the younger, active players which carries through to the players’ collective bargaining.

Source: WSJ

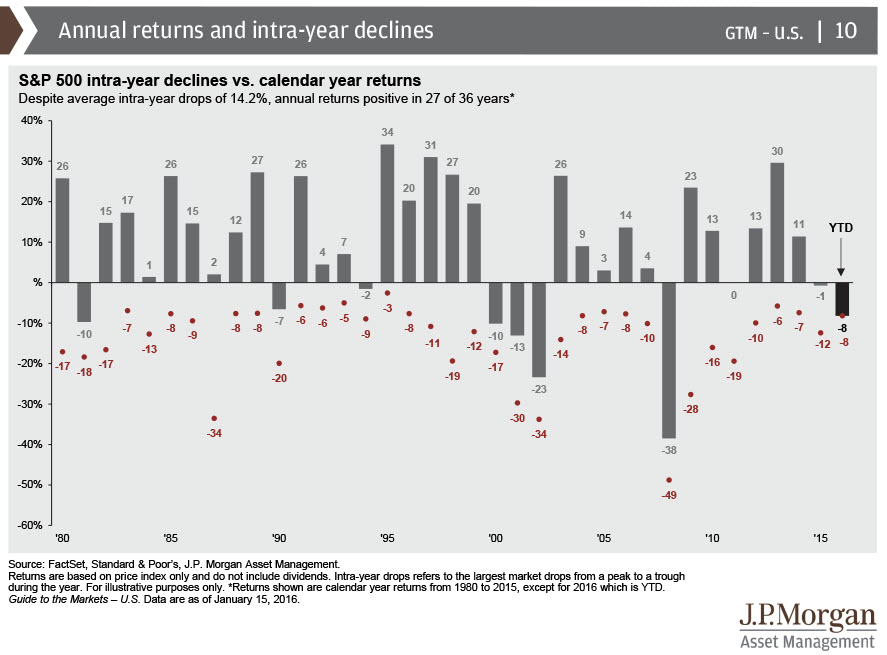

Happens All The Time

The New Year selloff in stocks has captured a lot of attention because,

- We’re not used to this since the market has been unusually quiescent the past few years

- The decline is global

- The speed of descent is significant

But despite perception, double-digit declines from prior highs are the norm, not an anomaly. It happens two out of every three years.

Here are great points of reference to put this market event into context:

-

The average intra-year decline is 16.4%. This current decline might feels worse due to the speed at which it’s happening, and because it’s occurring right out of the gate.

-

Double digit declines are to be expected, 64% of all years experienced them.

-

It’s not unusual for those double digit declines to be of little importance. 57% of the years with 10% drawdowns finished positive.

-

Stated differently, 36% of all years saw a double digit decline and still finished positive.

-

Drawdowns of 20% or more have happened 23 times, or 26% of all years. On five of those 23 occasions, stocks still ended up positive on the year.

The following chart provides a great visual on how intra-year drawdowns are normal.

Source: TII

No COLA in 2016

Not so great news for the 65 million retirees and others that receive Social Security benefits. For the first time in 5 years, there will be no annual raise in Social Security benefits. There’s no cost of living adjustment or COLA going into 2016 because falling gas prices have kept inflation low. According to the Social Security Administration’s calculations, inflation is down 0.6% for the past 12-month period that ended in September. This decline is largely driven by the 30% drop in gas prices.

Not so great news for the 65 million retirees and others that receive Social Security benefits. For the first time in 5 years, there will be no annual raise in Social Security benefits. There’s no cost of living adjustment or COLA going into 2016 because falling gas prices have kept inflation low. According to the Social Security Administration’s calculations, inflation is down 0.6% for the past 12-month period that ended in September. This decline is largely driven by the 30% drop in gas prices.

Automatic benefits increases, also known as cost-of-living adjustments or COLAs, have been in effect since 1975. In the current process. the COLA is computed at the close of September and goes into effect with January’s benefit checks. Here’s complete list of COLAs received 1975-12016:

- January 2016 — 0.0%

- January 2015 — 1.7%

- January 2014 — 1.5%

- January 2013 — 1.7%

- January 2012 — 3.6%

- January 2011 — 0.0%

- January 2010 — 0.0%

- January 2009 — 5.8%

- January 2008 — 2.3%

- January 2007 — 3.3%

- January 2006 — 4.1%

- January 2005 — 2.7%

- January 2004 — 2.1%

- January 2003 — 1.4%

- January 2002 — 2.6%

- January 2001 — 3.5%

- January 2000 — 2.5%

- January 1999 — 1.3%

- January 1998 — 2.1%

- January 1997 — 2.9%

- January 1996 — 2.6%

- January 1995 — 2.8%

- January 1994 — 2.6%

- January 1993 — 3.0%

- January 1992 — 3.7%

- January 1991 — 5.4%

- January 1990 — 4.7%

- January 1989 — 4.0%

- January 1988 — 4.2%

- January 1987 — 1.3%

- January 1986 — 3.1%

- January 1985 — 3.5%

- January 1984 — 3.5%

- July 1982 — 7.4%

- July 1981 — 11.2%

- July 1980 — 14.3%

- July 1979 — 9.9%

- July 1978 — 6.5%

- July 1977 — 5.9%

- July 1976 — 6.4%

- July 1975 — 8.0%

Clinton’s Capital Gains Tax and Your Investments

Presidential candidate Hillary Clinton has put forward a major change to current capital-gains tax rates in an effort to get corporate managers to focus on long-term growth. Under Clinton’s proposal, investors would have to hold an investment for 6 years instead of the current 1-year requirement to qualify for the lowest rate on capital gains.

Presidential candidate Hillary Clinton has put forward a major change to current capital-gains tax rates in an effort to get corporate managers to focus on long-term growth. Under Clinton’s proposal, investors would have to hold an investment for 6 years instead of the current 1-year requirement to qualify for the lowest rate on capital gains.

But what’s the impact on individual investors like yourself?

Tax experts say most investors will feel no impact from this proposal for two reasons:

#1 Clinton’s proposed changes would affect only people in the top income-tax bracket

That bracket begins at $464,850 for married couples filing jointly and $411,500 for single filers in 2015.

#2 Many investors hold most of their investments within tax-sheltered retirement accounts such as IRAs and 401(k) plans.

These assets grow tax-free until withdrawal at which point proceeds are usually taxed as ordinary income and not eligible for the more favorable capital-gains tax rates.

Recent Posts

-

-

Four Things That Can Sabotage Retirement July 9,2026

Four Things That Can Sabotage Retirement July 9,2026 -

Is 2032 the End of Social Security? June 25,2026

Is 2032 the End of Social Security? June 25,2026 -

-