10 Things About Living Longer in Retirement

Click the graphic for a better look…

4 Weeks Until an Important Deadline

Here’s an important reminder if you have an individual retirement account (IRA) or are considering opening an IRA. 2014 contributions to IRAs can still be made up through April 15, 2015.

Here’s an important reminder if you have an individual retirement account (IRA) or are considering opening an IRA. 2014 contributions to IRAs can still be made up through April 15, 2015.

Make it a double? If you really want to make the most of the growth potential that retirement accounts offer, you should consider making a double contribution this year: a last-minute one for the 2014 tax year and an additional one for 2015, which you’ll claim on the tax return you file next year. That strategy can add much more to your retirement nest egg than you’d think.

2014/2015 Annual IRA Contribution Limits*

- Traditional/IRA Rollover: $5,500 ($6,500 if you are 50 years old or older)

- Roth IRA: $5,500 ($6,500 if you are 50 years old or older)

- SIMPLE IRA: $12,000 (2014), $12,500 (2015) ($14,500/$15,500 if you are 50 years old or older)

- SEP IRA: $52,000 (2014), $53,000 (2015)

*Note: The maximum contribution limit is affected by your taxable compensation for the year. Refer to IRS Publication 590 for full details.

The savings, tax deferral, and earnings opportunities of an IRA make good financial sense. The sooner you make your contributions, the more your money can grow.

If you have any questions or would like to make an IRA contribution give us a call at (704) 350-5028 or email info@nstarcaptical.com.

Top 10 Mistakes Made with Beneficiary Designations

#1 — Not Naming a Beneficiary

#1 — Not Naming a Beneficiary

By not naming a beneficiary you have most likely guaranteed that the asset will go through probate upon your death.

#2 — Not Designating Contingent Beneficiaries

If your primary beneficiary predeceases or dies at the same time as you, you’re subject to the same consequences as #1

#3 — Failing to Keep Beneficiary Designations Up-to-Date

If you get divorced, it’s essential you immediately review and update all beneficiary designations.

#4 — Naming Minors as Direct Beneficiaries

Trusts are often established to delay the time a survivor receives an asset until they are old enough to make good money decisions. However, if you designate a minor child as an account’s beneficiary and there’s also a testamentary trust, the designation trumps the trust and the child will receive the assets immediately.

#5 — Naming Special Needs Individuals as Direct Beneficiaries

Naming a “special needs” individual as the direct beneficiary could unintentionally disqualify that individual from receiving his or her valuable governmental benefits.

#6 — Naming Financially Irresponsible Beneficiaries

Often it’s better to create a lifetime “spendthrift trust” to hold the inheritance for the benefit of the individual for his or her lifetime while protecting the assets from creditors.

#7 — Naming Direct Beneficiaries on All Assets Other than Real Estate

Very often real estate will need to go through probate even if there’s a will in place. This process can take a year or longer during which the estate is responsible for paying for maintenance, taxes, etc. It’s generally advisable to allow your cash accounts and/or life insurance proceeds to go through probate so the estate will have sufficient funds to support the real estate during probate.

#8 — Naming Multiple Beneficiaries on a Transfer on Death Deed

Avoid doing because all beneficiaries must agree on the realtor, sale price, and maintenance costs until the property is sold. Getting that type of agreement is very difficult.

#9 — Naming a Child as Co-Owner of a Deposit or Investment Account

Aging parents will sometimes add a trusted adult child as the co-owner of his or her bank account. Avoid this because it can create complicated issues around gifting, creditor issues, and final expenses.

#10 — Naming One Child as the Sole Beneficiary of a Life Insurance Policy or Deposit Account

A parent with multiple adult children should avoid doing this because it can create a situation very similar to #9.

Source: AAII

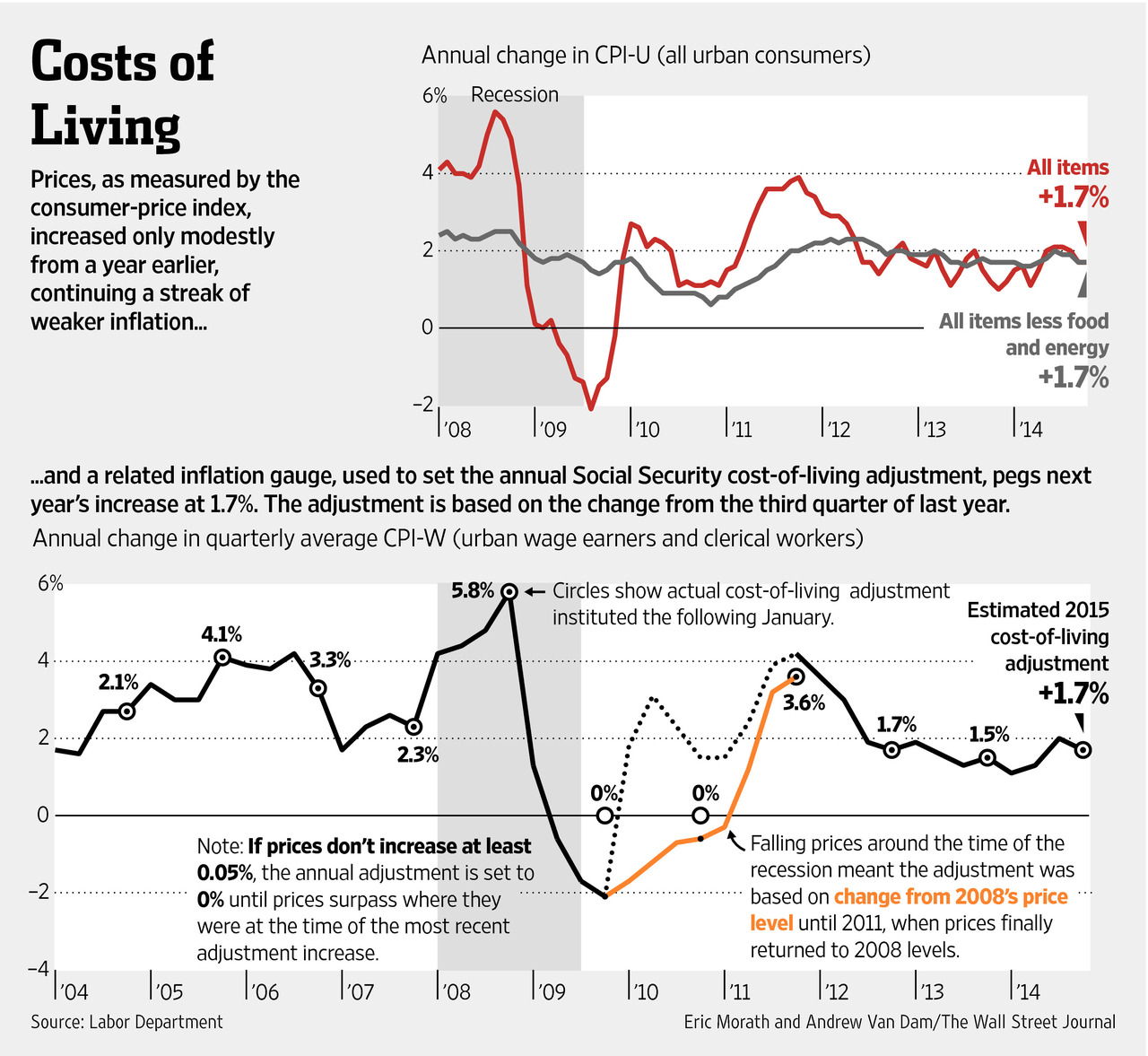

Low Inflation, Flatter COLA

The Social Security Administration on Wednesday announced a 1.7% annual cost-of-living adjustment, or COLA, for the nearly 64 million Americans who receive federal retirement or disability benefits. The increase would result in about a $22-a-month increase for the average retiree. Increases have been between 1.5% and 1.7% for three straight years.

The benefit increase in 2015 matches the 1.7% gain in consumer prices in September, compared to a year earlier, according to Labor Department data also released Wednesday.

source: WSJ

7 Fatal Flaws in 401(k) Plans

Paul Merriman writes about seven fatal flaws in America’s 401(k) plans:

Paul Merriman writes about seven fatal flaws in America’s 401(k) plans:

#1 Restricted Access

The first and biggest flaw in 401(k) plans is restricted access to the best investment choices

#2 Participation not required

I believe that many American households, with nothing saved for retirement, are headed by employed breadwinners who could participate in a 401(k) retirement plan

#3 Insufficient employer match

I also think employers should be required to match at least a quarter of what each employee contributes — after the waiting period, of course.

#4 Employees bear the costs

Many employers make their workers pay the costs of administering a 401(k) plan, which should be treated as an employee benefit that’s paid for by the company. In far too many cases, the costs paid by employees are hidden in the form of higher fees for investment funds.

#5 No Rollover IRA option

Federal law allows — but doesn’t require — employers to let employees move part or all of their 401(k) balances into a Rollover IRA while continuing to contribute to the company plan. All workers should have this option, which gives them access to virtually unlimited investment choices.

#6 Too much company stock

Corporate 401(K) plans often encourage participants to load up on company stock. There’s probably no way to stop this short of a federal law, because employers with publicly-traded stock love the steady market that’s created for their shares every payday.

#7 Default options are too safe

Too many plans steer contributions to low-performance investments. It’s bad enough that the employee’s default option in many plans is simply not to participate. But for those who do sign up, it’s equally wrong to have a default option of a stable value fund that virtually guarantees the employee will gradually lose some of the purchasing power of their savings.

Supreme Court: No Bankruptcy Protection for Inherited IRAs

In June the U.S. Supreme Court issued a unanimous ruling stating that inherited IRAs are not protected from creditors under the bankruptcy code. This decision does not apply to any other type of individual retirement accounts.

In June the U.S. Supreme Court issued a unanimous ruling stating that inherited IRAs are not protected from creditors under the bankruptcy code. This decision does not apply to any other type of individual retirement accounts.

The Supreme Court case centered on an inherited, non-spousal IRA. Heidi Heffron-Clark inherited her mother’s traditional IRA in 2001. Heffron-Clark subsequently declared bankruptcy in 2010.

The Court acknowledged there is an exemption in the bankruptcy code for retirement accounts. More specifically, the code gives protection to “retirement funds” that are “sums of money set aside for the day an individual stops working”.

The funds set aside in an inherited IRAs are not considered retirement savings because of three legal properties:

- Additional funds can never be contributed to an inherited IRA

- Beneficiaries of inherited IRAs are required to either withdraw the entire balance within 5 years after the owner’s death or take minimum withdrawals every year

- The owner of the an inherited IRA can make withdrawals at any time, whereas traditional and Roth IRA owners incur a penalty for withdrawing before age 59 1/2

Justice Sonia Sotomayor, writing for the court, highlighted that the bankruptcy protections given to traditional and Roth IRAs are intended to protect the debtor’s needs in retirement. Affording the same protection to inherited IRAs would give debtors essentially a “free pass” as the funds could be used to purchase “a vacation home or sports car immediately after her bankruptcy proceedings are complete.”

Source:

“Clark et ux v. Rameker, Trustee, et al,” U.S. Surpeme Court, No. 13-299 (June 12, 2014)

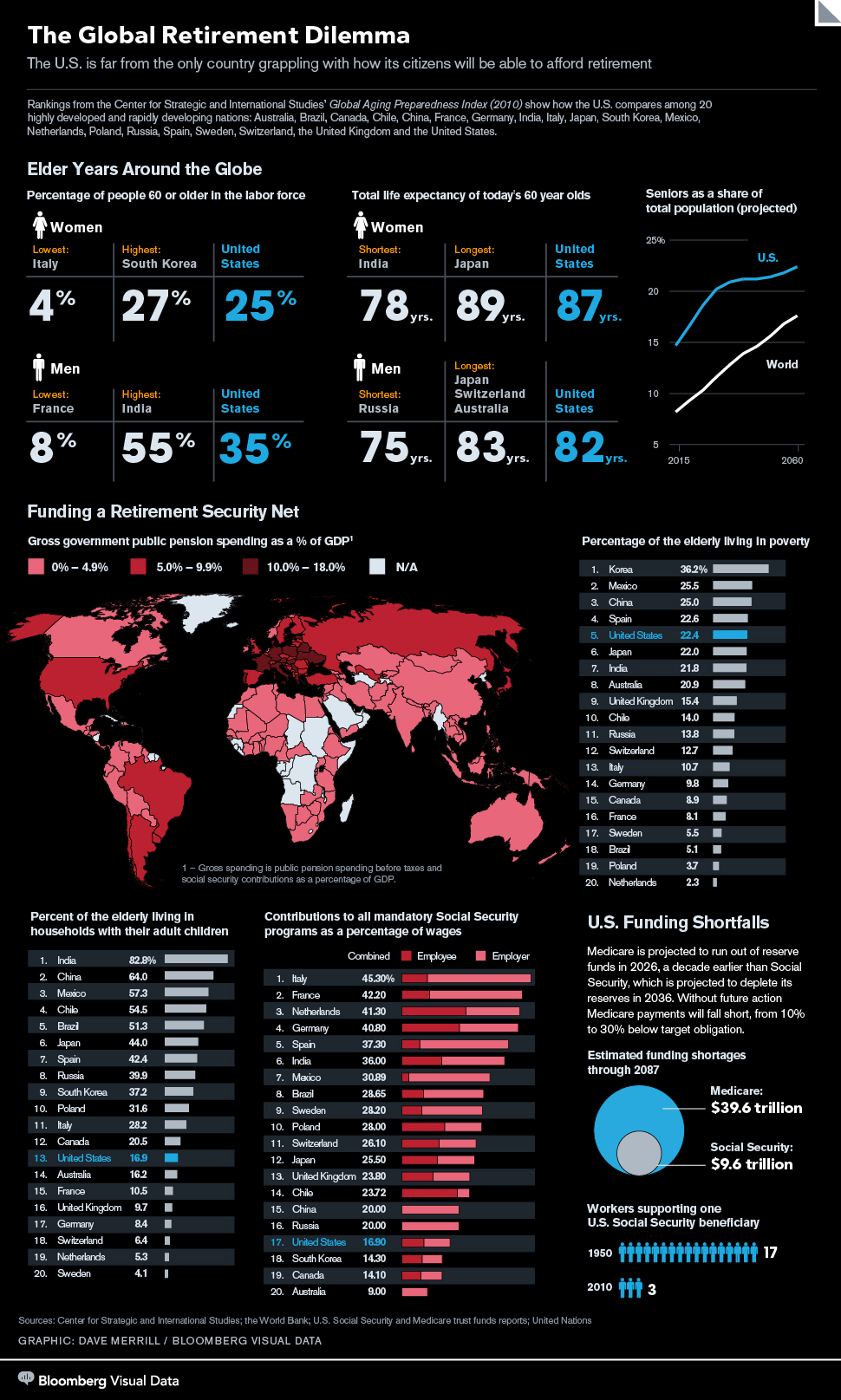

Global Retirement Dilemma

Source: Bloomberg

Inherited IRAs

Inheritances received via an IRA can be advantageous since you can choose to stretch the required distributions across your life expectancy, giving the assets more time to grow (plus taxes aren’t due until withdrawals are made). Here are key best practices to keep in mind:

Inheritances received via an IRA can be advantageous since you can choose to stretch the required distributions across your life expectancy, giving the assets more time to grow (plus taxes aren’t due until withdrawals are made). Here are key best practices to keep in mind:

- When you inherit an IRA from anyone other than your spouse, you can’t roll it over into your own IRA

- Instead, you have to retitle the IRA so it is clear the owner died and you are the beneficiary

- If you move the account to a new custodian, make sure it is a “trustee to trustee” transfer”

- If the check is mistakenly made out to you, the IRS will consider it a “total distribution” subject to tax and if you are anyone other than the surviving spouse, it would effectively end the IRA

- Be aware there are deadlines for all of these actions

- If the IRA owner dies after age 70 1/2 (when required withdrawals start) and didn’t yet take a withdrawal for the year, the heir has to do so by December 31

(if you miss the deadline, you are subject to a 50% penalty on the amount you should have withdrawn!) - If you are a nonspouse beneficiary, determine the required distribution by looking up your life expectancy on the single-life table in IRS publication 590

(most IRA custodians will calculate the required withdrawal amount for you but you need to make sure they are using the inherited IRA calculation) - Once you receive a 1099 form, confirm that the custodian properly indicated the distribution as a code “4”

Know More, Make More

A new academic study finds that more financially knowledgeable people earn a higher return on their 401(k) retirement savings.

A new academic study finds that more financially knowledgeable people earn a higher return on their 401(k) retirement savings.

Dr Robert Clark (NC State University), Dr. Annamaria Lusardi (George Washington University), and Dr. Olivia Mitchell (University of Pennsylvania) analyzed a unique dataset that combined 401(k) performance data for 20,000 employees plus financial literacy data for the same workers.

Investors deemed to be more financially knowledgeable than peers enjoyed an estimated 1.3% higher annual return in their 401(k)s or other defined contribution plans than those with less knowledge.

According to the study’s authors:

“We show that more financially knowledgeable employees are also significantly more likely to hold stocks in their 401(k) plan portfolios. They can also anticipate significantly higher expected excess returns, which over a 30-year working career could build a retirement fund 25% larger than that of their less-knowledgeable peers.”

Financially savvy people tend to save more and are more likely to invest those savings in the stock market. But past studies haven’t clearly demonstrated that these people necessarily make better investment decisions. The authors look at patterns in 401(k) retirement accounts and find that more sophisticated investors do indeed get better returns on their savings.

Source: “Financial Knowledge and 401(k) Investment Performance”

Recent Posts

-

-

Four Things That Can Sabotage Retirement July 9,2026

Four Things That Can Sabotage Retirement July 9,2026 -

Is 2032 the End of Social Security? June 25,2026

Is 2032 the End of Social Security? June 25,2026 -

-